Introduction

In commercial construction, the monthly pay application is where completed work becomes collected cash. Get it wrong — miscalculate a line item, miss a change order, or let retainage sit uncollected — and the cash flow consequences compound fast.

AIA billing, built around two standardized forms (G702 and G703), governs how contractors document progress, apply for payment, and track what owners withhold. It's the payment infrastructure for most commercial contracts.

The forms themselves are straightforward. Maintaining accuracy across dozens of billing periods, dozens of projects, and the constant movement of change orders, stored materials, and subcontractor invoices — that's where the process breaks down.

If you're a construction finance manager, CFO, or CPA advising construction clients, this guide covers how the forms work, why retainage creates financial pressure at the portfolio level, and where the process breaks down in practice.

Key Takeaways

- G702 is the payment application summary; G703 is the itemized schedule of values breakdown — you need both for a complete AIA pay application.

- Retainage (typically 5–10% of each progress payment) accumulates as a separate receivable and must be tracked independently from earned revenue.

- Each billing cycle: update percent complete by line item, roll up to the G702, and submit with supporting docs for architect certification.

- The most common failures: missing change orders on the G703, front-loaded schedules of values, and retainage that never gets proactively invoiced at closeout.

- Finance teams managing 10+ active jobs need portfolio-level retainage visibility to protect working capital and bonding capacity, not just per-project accuracy.

What Is AIA Billing and How Do G702 and G703 Work?

AIA billing is a standardized progress-payment framework — developed by the American Institute of Architects — that uses two linked forms to document what has been built, what has been paid, and what is being withheld on a commercial construction contract.

The G702: Application and Certificate for Payment

The G702 is the cover sheet. It summarizes:

- Original contract sum

- Net adjustments from approved change orders

- Total completed and stored to date

- Total retainage withheld (cumulative)

- Total previously certified

- Current payment due

The contractor signs it; the architect certifies it. If the architect's assessed value differs from what the contractor claimed, the certificate reflects the architect's number — not the contractor's.

The G703: Continuation Sheet

The G703 does the detailed accounting. It breaks down the contract into individual schedule of values line items, with columns for:

- Scheduled value

- Work completed in previous periods

- Work completed this period

- Materials presently stored

- Running total and percentage complete

- Balance to finish

- Retainage withheld per line

Arithmetic errors, disputed percentages, and billing disputes almost always originate here.

The Schedule of Values: The Foundation Everything Else Depends On

Per AIA A201-2017, before the first pay application is submitted, the contractor must provide a Schedule of Values allocating the entire contract sum to defined portions of work. Every G703 for the project's life draws from that original SOV.

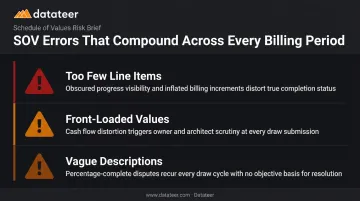

Errors made at SOV setup compound across every billing period. A poorly structured SOV creates problems that are hard to unwind once the project is underway:

- Too few line items obscure actual progress and inflate individual billing increments

- Front-loaded values on early work distort cash flow and draw scrutiny from owners and architects

- Vague descriptions invite disputes over percentage-complete assessments at every draw

How Retainage Appears Mechanically on the Forms

Retainage is calculated as a percentage — commonly 5% or 10% — of each line item's completed-and-stored amount. That deduction is applied on the G703 line by line, then carried to the G702 as a cumulative withholding balance.

The balance grows with every pay application. Release typically requires hitting a contractual trigger — most often substantial completion — which is why retainage exposure can build to significant sums before a single dollar comes back.

Why Retainage Tracking Is a Financial Pressure Point in Construction

Retainage exists as a performance guarantee. Owners withhold it so contractors have financial incentive to resolve punch list items and meet warranty obligations before receiving final payment. It's standard on commercial contracts and legally regulated in most U.S. states through prompt-payment statutes.

The Construction Financial Management Association confirms retainage is typically 5% or 10% of total project cost. At 10% across a portfolio of active commercial jobs, the withheld balance can represent a substantial portion of a firm's receivables — capital that is earned but inaccessible.

The Balance Sheet Problem

Under FASB Topic 606, retainage classification depends on whether the contractor's right to payment is unconditional. According to FASB's 2025 Staff Educational Paper, unconditional retainage — where only time passage is required before payment — is presented as a receivable. Conditional retainage still tied to performance milestones is generally a contract asset.

Mixing these up distorts the balance sheet and the WIP schedule that sureties, lenders, and CPA reviewers depend on.

Misclassified retainage has downstream consequences:

- Over- and under-billing positions shift on the WIP schedule when retainage is improperly categorized

- Inaccurate retainage presentation weakens the balance sheet picture sureties use to assess working capital and financial condition

- Retainage misclassified out of receivables directly reduces the 10–20x working capital multiplier that determines bonding capacity

The Cost of Passive Retainage Management

Contractors who don't actively track release milestones routinely wait 30–60 days beyond what their contracts require before submitting retainage invoices. The problem isn't contractual — it's operational. Finance teams focused on active billings often treat retainage as something that will take care of itself at project end. It doesn't.

How the AIA Billing Process Works

The monthly billing cycle runs on a fixed cadence. Most projects set a cutoff around the 25th, with three parallel tracks converging into a single pay application package.

Step 1: Build the Schedule of Values

The SOV is negotiated and approved at contract award. Each line item should align directly with the contractor's cost codes so billing data flows into job costing without manual re-entry.

Common SOV structuring errors to avoid:

- Front-loading mobilization or general conditions to accelerate early cash — this creates owner overpayment risk and can flag the SOV for rejection during architect review

- Too few line items that obscure real progress and make percentage disputes harder to resolve

- Line items that don't map to cost codes, which forces manual reconciliation every billing period

The architect reviews the SOV before work begins — getting their sign-off early eliminates the most common source of first-application disputes.

Step 2: Prepare the Monthly G702/G703 Pay Application

Each period, update the G703 with:

- Percentage complete per line item — verified with a field walkthrough, not estimated from the office

- Stored materials — documented with invoices and photos

- Approved change orders — added as new G703 line items, with the G702 contract sum updated to reflect the change

- Subcontractor billing rolls — confirmed before the application is finalized

Change orders that exist in the project management system but haven't been added to the G703 represent unbilled earned revenue. Per CFMA, unapproved or unincorporated change orders create recurring accounting risk — including potential removal from contract value if sureties or banks don't understand the supporting facts. That's a problem to solve before submission, not after.

Step 3: Submit for Architect Certification and Owner Payment

The architect typically has 7 days under AIA A201-2017 to review claimed percentages against observed field progress — and they can certify a different amount than requested. Certification can be withheld for:

- Defective work not remedied

- Failure to pay subcontractors or suppliers

- Unsupported completion percentages

- Missing lien waivers

Any rejection or short-certification restarts the payment clock. Verifying field percentages, lien waiver status, and change order inclusion before submission is what prevents a 30-day payment window from stretching to 60.

Step 4: Track and Invoice Retainage at Project Closeout

Once the project clears certification, most teams assume the hard work is done. It isn't — retainage release requires a separate, proactive process. The contractor must:

- Identify the contractual release trigger — typically substantial completion, defined under AIA A201-2017 as the point when the owner can occupy or use the facility for its intended purpose

- Submit a retainage-specific pay application at that milestone

- Collect conditional or unconditional lien waivers from all subcontractors before the owner will release withheld funds

Waiting for the owner to initiate this process is how retainage stays uncollected for months past its contractual due date.

Key Factors That Affect AIA Billing Accuracy and Timeliness

Schedule of Values Quality

The SOV determines billing accuracy for the project's entire life. A front-loaded SOV — where early-complete items carry inflated values — can cause owner overpayment early and create a cash shortfall late. Per AIA guidance, front-loading accelerates contractor cash flow at the owner's expense and raises default risk if the project doesn't complete.

What a well-structured SOV looks like:

- One line item per meaningful scope segment, not one catch-all per trade

- Dollar values that reflect realistic cost distribution across the project timeline

- Direct alignment between SOV line items and ERP cost codes (eliminates manual re-entry)

- Reviewed and accepted by the architect before the first billing period

Change Order Management

Every approved change order must be on the G703 before the pay application is submitted. Change orders processed in Procore or the project management system but never incorporated into the billing form represent earned revenue that isn't being invoiced.

This gap is one of the most consistent sources of revenue leakage on commercial projects — and it's preventable. Finance teams that reconcile change order logs against billing records each period catch these omissions before they age into material shortfalls.

Portfolio-Level Data Integrity

Finance teams managing 15–50+ active projects can't maintain accurate retainage receivable totals through spreadsheet aggregation. The lag and error risk are the same as on WIP — every manual touch is a potential discrepancy.

Datateer addresses this: the platform syncs automatically with 12+ construction ERPs (Procore, Sage, Viewpoint Vista/Spectrum, Acumatica, Foundation Software, CMiC, Jonas, QuickBooks, NetSuite) and surfaces retainage analytics across the full project portfolio. Tracked at the portfolio level:

- A/R retainage by project and owner

- A/P retainage held on subcontractors

- Retainage release schedules and aging

- Impact on 13-week cash flow forecasting

Overdue retainage releases that are tying up working capital get flagged automatically — not buried in a spreadsheet tab no one opens until month-end.

Common Issues and Misconceptions in AIA Billing

"Billing Percentage Equals Physical Completion"

The G703 percentage reflects value completed relative to scheduled value — not the share of physical work finished. A line item with expensive materials installed early can show 80% billed at 40% physical completion. That's legitimate billing, not an error.

The reverse — physical work done but not yet billed — creates underbilling that distorts WIP and understates revenue. Controllers who confuse the two metrics end up with WIP schedules that mislead on project health.

"Retainage Releases at Project Completion"

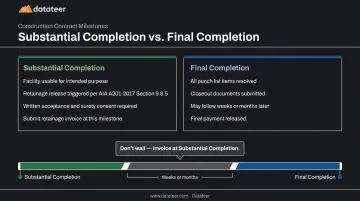

Most contractors assume retainage holds until the project is fully closed out. Many contracts don't work that way. Substantial completion — not final completion — is the typical release trigger.

AIA A201-2017 Section 9.8.5 requires the owner to release retainage on substantially complete work upon written acceptance and surety consent. These are two distinct milestones:

- Substantial completion: Work is usable for its intended purpose; retainage release is triggered

- Final completion: All punch list items resolved, closeout documents submitted — may follow weeks or months later

Submitting a retainage invoice at substantial completion recovers cash faster and is contractually correct. Waiting for final completion leaves money on the table unnecessarily.

The Overbilling Trap

Front-loading the SOV or claiming inflated completion percentages creates a billing deficit late in the project: actual costs accumulate while remaining billable value is exhausted. The consequences:

- WIP schedule shows a distorted over-billing position early, then flips

- Sureties and lenders flag inconsistency in billing-to-cost ratios

- Owners may demand credits on future applications or withhold payment pending reconciliation

By the time the overbilling position reverses, the project may already be flagged by a surety or lender — and recovering that trust takes longer than the cash benefit was worth.

Frequently Asked Questions

What is AIA G702 and G703?

G702 is the payment application cover sheet summarizing total contract value, retainage withheld, and the current payment due — signed by the contractor and certified by the architect. G703 is the itemized continuation sheet broken down by schedule of values line items. Both forms are required together to constitute a complete AIA pay application.

How do I bill for retainage on an AIA form?

Retainage isn't submitted as a separate line item during active billing. It's automatically calculated on each G703 line as a percentage of total completed and stored, then deducted from the G702 current payment due. A separate retainage invoice is submitted at substantial completion when the contract triggers release of withheld funds.

Is AIA billing hard to learn?

The forms are straightforward once the schedule of values is established. Maintaining accuracy across multiple billing periods is where errors creep in: tracking change orders, stored materials, and subcontractor roll-ups requires consistent discipline. Software that automates carryforward calculations and flags discrepancies significantly reduces that error rate.

What percentage is typically withheld as retainage?

Retainage is most commonly 5% or 10% of each progress payment, as set by the contract. Many contracts reduce retainage to 5% at 50% project completion. State laws also apply: Illinois requires reduction to 5% at 50% completion; Florida caps public project retainage at 5%; New York limits private project retainage to 5%.

When is retainage released on a construction project?

Release is typically triggered by substantial completion, when the owner can occupy the facility for its intended purpose. Some contracts release retainage in phases by subcontract or building area. Final release generally requires resolved punch list items, collected lien waivers, and submitted closeout documents.

How does retainage affect a construction company's cash flow and WIP reporting?

Retainage receivable accumulates as a separate balance sheet item distinct from standard AR and must be tracked accurately in WIP reporting. Large balances reduce working capital, affect bonding capacity calculations sureties rely on, and signal cash flow risk when misclassified or left uncollected past contractual release dates.

Conclusion

AIA billing and retainage tracking convert completed work into collected cash — but only when the schedule of values is sound, change orders are incorporated each period, and retainage milestones are actively managed rather than passively waited on.

The process rarely fails because someone doesn't understand the forms. It fails because field progress data, project management records, and financial reporting don't stay synchronized.

Firms that connect their billing data to real-time financial visibility — rather than reconciling spreadsheets after the fact — catch unbilled change orders before they age, identify retainage ready for release before the owner's payment clock runs out, and give sureties and lenders the clean WIP data they need to extend credit.

Datateer's retainage tracking and WIP dashboards plug directly into your existing ERP — Sage, Viewpoint, Acumatica, Procore, and others — so your billing data, change order status, and retainage balances stay current without the spreadsheet grind. If you're not sure where your firm stands, the free 15-Minute Workflow Audit is a quick way to find out.