This happens more than most firms want to admit. According to FMI, contractors lost an estimated $30–$40 billion to labor inefficiencies in 2022 alone — and inaccurate burden rate assumptions are a direct contributor to that number.

This guide covers everything a construction finance team needs to get burden rates right: what the fully burdened labor rate actually includes, how to calculate it with a worked example, construction-specific benchmarks, Davis-Bacon compliance requirements, and the mistakes that quietly destroy margins on otherwise healthy jobs.

Key Takeaways

- The fully burdened labor rate = base wages + all indirect employer costs (taxes, insurance, benefits, PTO), and typically runs 30–50% above base wages

- Estimates built on unburdened wages systematically underprice jobs — a pattern that keeps firms busy but unprofitable

- Burden rates vary by trade, union status, and state; using one blended company-wide rate introduces error into every bid

- Davis-Bacon projects impose mandatory fringe benefit floors that make burden rate accuracy a compliance issue, not just a financial one

- Firms tracking burdened costs in real time catch margin fade early enough to protect the job

What Is a Fully Burdened Labor Rate?

The fully burdened labor rate is the total hourly cost to employ a worker — their gross wage plus every indirect employer-paid cost attached to that employment relationship. The number on their paycheck is only part of the story.

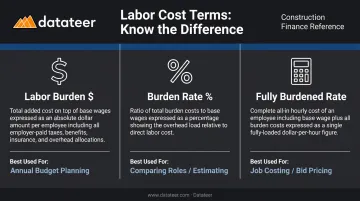

Three related figures get conflated regularly, and each serves a different purpose:

| Term | Definition | Best Used For |

|---|---|---|

| Labor Burden $ | Total dollar amount of all indirect costs | Annual budget planning |

| Burden Rate % | Indirect costs ÷ base wages × 100 | Comparing across roles; estimating |

| Fully Burdened Rate | Base wage + labor burden, per hour or per year | Job costing; bid pricing |

The Sticker Price Problem

A worker earning $30/hour typically costs $39–$45/hour fully burdened. Every estimate built on $30 systematically underestimates true labor cost — a structural gap that compounds across every bid and every project.

Two scope boundaries matter here:

- The fully burdened rate excludes markup, profit margin, and overhead costs unrelated to a specific employee

- Pulling those items into this calculation — and then into overhead markup — creates double-counting, a common estimating error covered later in this guide

What Does a Fully Burdened Labor Rate Include?

Mandatory Payroll Taxes

These apply to virtually every W-2 employee and are non-negotiable:

- Employer FICA: 6.2% Social Security (up to the $184,500 wage base) + 1.45% Medicare = 7.65% standard employer FICA per IRS Publication 15

- FUTA: 6.0% on the first $7,000 of wages; drops to an effective 0.6% when the full 5.4% state unemployment credit applies

- SUTA: State unemployment tax — experience-rated and varies widely by state. California's Schedule F+ runs 1.5% to 6.2% on a $7,000 wage base

- State-specific programs: Washington's 2026 Paid Family and Medical Leave premium is 1.13% of wages, with employers covering 28.57% of that total

Workers' Compensation Insurance

Workers' comp is the most variable burden item in construction. Rates depend on trade classification code, state, and the firm's claims history, and they change at every policy renewal.

One documented example: Texas TDI sets the July 1, 2026 loss cost for Code 5551 (Roofing) at 1.946 per $100 of payroll before the carrier's multiplier. A roofer carries higher comp costs than a carpenter or office administrator. California's workers' comp advisory pure premium rates were proposed to increase an average of 10.4% for September 2026, while Oregon's dropped for the 13th consecutive year. These rates must be verified at each renewal, not carried forward from last year.

Employee Benefits

- Employer-paid health, dental, and vision premiums

- 401(k) match or pension contributions

- Life and disability insurance

- Union multiemployer benefit plan contributions, where applicable (these can be substantial)

Paid Time Off and Non-Productive Time

PTO is paid but generates no billable output. Those hours have to be spread across productive hours, which raises the effective hourly cost.

According to BLS 2025 benefits data, construction and extraction occupations have access rates of 76% for paid vacation and 80% for paid holidays.

If an employee works 1,880 productive hours out of 2,080 paid hours, burden calculations must reflect that gap: the base wage is being paid for all 2,080 hours, but only 1,880 are billable.

Role-Specific Costs

The following belong in the burden rate for roles where they apply:

- Safety training and certifications

- Personal protective equipment (PPE)

- Per diem and travel allowances

- Tool allowances and uniforms

- Cell phone stipends

Company vehicles are typically categorized as equipment overhead. Those costs persist after an employee leaves, so they don't belong in the labor burden calculation.

How to Calculate the Fully Burdened Labor Rate

The Core Formulas

Fully Burdened Labor Rate = (Total Base Wages + Total Indirect Labor Costs) ÷ Total Productive Hours

Burden Rate (%) = Total Indirect Labor Costs ÷ Total Base Wages × 100

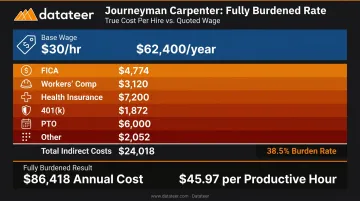

Worked Example: Journeyman Carpenter

Assumptions: $30/hour base wage, 2,080 paid hours, 1,880 productive hours

| Cost Category | Annual Amount |

|---|---|

| Base wages (2,080 hrs × $30) | $62,400 |

| Employer FICA (7.65%) | $4,774 |

| FUTA (effective 0.6% on $7,000) | $42 |

| SUTA (estimated 3.0% on $7,000) | $210 |

| Workers' comp (varies by code/state) | $3,120 |

| Health insurance (employer share) | $7,200 |

| 401(k) match (3%) | $1,872 |

| PTO (200 non-productive hrs × $30) | $6,000 |

| Safety training / PPE | $800 |

| Total Indirect Costs | $24,018 |

| Total Burdened Annual Cost | $86,418 |

Burden Rate = $24,018 ÷ $62,400 = 38.5%

Fully Burdened Hourly Rate = $86,418 ÷ 1,880 productive hours = $45.97/hour

That $30 base wage costs nearly $46 per productive hour — and if your bids are priced at anything close to $30, you're absorbing that gap directly out of margin.

Scaling Across a Workforce

Don't run individual calculations for every employee. Group workers by trade classification — roofers, laborers, carpenters, electricians — and calculate a burden rate per classification. Workers' comp codes and benefit tiers differ enough across trades that blending everything into one company-wide rate will introduce real error into bids.

How Often to Recalculate

At minimum, twice per year. Recalculate immediately when any of these occur:

- Insurance renewal (WC premiums can shift 10%+ in a single filing)

- New or amended union agreement

- Benefit plan changes

- State payroll tax rate adjustments

Using last year's rates builds error into every bid before work starts. Manual recalculation catches the big events, but it misses the slow drift between them. Datateer's Overhead & Burden Rate Analytics module addresses this by syncing directly from 12+ construction ERPs — including Sage, Viewpoint, and Acumatica — so finance teams can compare budgeted burden rates to actuals at the project level on a continuous basis, not just at renewal time.

Benchmark Reality Check

BLS Employer Costs for Employee Compensation data (December 2025) shows private industry benefits averaging $13.79/hour against wages of $32.36/hour — a 42.6% burden-to-wage ratio across all private industry. If your calculated burden rate is significantly below that benchmark, you're likely missing cost categories. Construction tends to run toward the higher end of the 30–50% range, primarily because of workers' comp premium costs that other industries don't carry.

Why Fully Burdened Labor Rates Matter in Construction

Accurate Bidding and Job Costing

Labor is one of the largest variable costs on any project. Estimates built on unburdened wages create systematic underpricing — not a one-time miscalculation, but a structural flaw that surfaces on every job. This produces the "busy and broke" problem: full schedules with margins that vanish by closeout.

The fix isn't complex. Use the actual fully burdened rate per trade classification at the estimating stage. The more precise the input, the more defensible the bid.

Real-Time Margin Protection

Knowing your burden rates is only half the equation. The value multiplies when burdened cost data is tracked at the project level continuously — not reconstructed during monthly close.

This is where purpose-built analytics earn their keep. Datateer's Overhead & Burden Rate module tracks burdened costs by craft, department, and division — comparing budgeted rates to actuals across all active jobs so finance teams catch variance while there's still time to act. Key capabilities include:

- Calculates actual fully burdened rates by trade classification

- Monitors overhead absorption at the project level

- Flags under-allocated overhead before it erodes margin

- Delivers budget-vs.-actual variance data during the project, not after close

Workforce Productivity and Capacity Planning

Comparing fully burdened cost to revenue generated per crew gives finance managers a genuine picture of labor efficiency. That ratio drives real decisions: whether to subcontract a trade, add headcount, or renegotiate rates. Using unburdened wages for that comparison overstates labor efficiency and produces bad capacity decisions.

Fully Burdened Labor Rates in Government Contracting

Davis-Bacon and Related Acts (DBRA) apply to federal construction contracts exceeding $2,000, covering alteration or repair of public buildings and public works. On these projects, burden rate accuracy is a compliance requirement, not just a financial best practice.

How Davis-Bacon Affects Burden Calculations

The Department of Labor publishes prevailing wage determinations for each trade and locality, including both base wage rates and fringe benefit rates. Those fringe rates set a minimum floor for the labor burden calculation on affected employees. Contractors can't estimate below them.

Wage determinations are published on the System for Award Management (SAM.gov) and incorporated directly into covered contracts.

Cash vs. Bona Fide Benefits

Contractors can satisfy fringe obligations two ways:

- Contribute to bona fide benefit plans (health insurance, pension, etc.) — contributions count dollar-for-dollar toward the fringe obligation

- Pay the fringe rate in cash, added to the worker's wage — this affects certified payroll line items differently

The choice has direct consequences for job cost accounting and certified payroll reporting. Getting it wrong on a federally funded project creates compliance exposure.

Audit and Enforcement Risk

Government contracts are subject to audit of all burden components. DOL enforcement carries real consequences. One 2023 enforcement action recovered $633,000 in back wages for 84 workers. Firms without a clear, well-documented labor cost structure face back-pay liability and potential disqualification from future bids.

Common Mistakes When Using Fully Burdened Labor Rates

Double-Counting Overhead

The most expensive estimating error: including labor-related costs in both the burden rate and the overhead markup. It produces bids that are uncompetitively high — and when the firm loses work, no one can easily trace why.

The reverse does just as much damage: removing items from overhead but estimating with unburdened wages prices those costs at zero.

The rule is simple: every cost lives in exactly one place. Decide before estimating which costs sit in the burden rate versus the overhead markup, document it, and apply it consistently.

Using Stale or Blended Rates

Two distinct problems, both common:

- Stale rates: Insurance renewals, benefit changes, and annual state tax adjustments can move burden costs 5–15% without anyone updating the estimating template. Workers' comp alone can shift 10%+ in a single filing year.

- Blended rates: Averaging a roofer, a laborer, and a superintendent into one company-wide rate ignores meaningful differences in workers' comp codes and benefit structures across those roles.

Both problems trace back to the same root cause: manually maintained rate tables that no one updates between projects. Pulling actual payroll and cost data directly from the ERP eliminates that dependency. Datateer's overnight sync from systems like Foundation, CMiC, and Procore automatically refreshes burden rate data without requiring anyone to update the estimating template by hand.

Omitting Irregular Costs

Infrequent costs get dropped from burden calculations because they don't appear in the standard monthly expense view:

- Annual safety certifications and recertifications

- One-time PPE purchases after a project-specific safety requirement

- Mid-year insurance adjustments outside the renewal cycle

- Discretionary bonuses

Maintain a running log of all employment-related costs and reconcile it against burden rate assumptions at least quarterly. If a cost is real and recurring — even annually — it belongs in the rate.

Frequently Asked Questions

What does a fully burdened labor rate include?

Base wages plus all indirect employer costs: payroll taxes (FICA, FUTA, SUTA), workers' compensation insurance, health and retirement benefits, employer-paid PTO, and role-specific costs like safety training and PPE. It does not include markup or general business overhead.

How do you calculate the fully burdened labor rate?

Sum all indirect labor costs for a period and divide by base wages to get the burden rate percentage. Multiply base wages by that rate and add back to wages for the fully burdened annual cost. Divide by productive hours (not total paid hours) to get the hourly rate.

What is the average fully burdened labor rate?

BLS ECEC data shows private industry benefits average 42.6% of wages across all industries. Construction typically runs toward the higher end of the 30–50% range due to workers' compensation costs. The right benchmark for any firm is their own calculated rate — not an industry average.

What is the fully burdened labor rate in government contracting?

On Davis-Bacon-covered projects, the Department of Labor publishes prevailing wage determinations with a mandatory fringe benefit component that sets a minimum burden floor. Contractors must include those fringe rates in burden calculations and report them line-by-line on certified payroll submissions under WH-347 requirements.

What is the difference between labor burden and overhead?

Labor burden covers indirect costs tied to a specific employee — taxes, insurance, benefits — that end when that employee leaves. Overhead covers general business costs — rent, software, administrative salaries — not tied to any single employee or project.

How often should construction firms recalculate burden rates?

At minimum twice per year, and immediately after any material change: insurance renewal, benefit plan adjustment, new union agreement, or state payroll tax rate change. Using outdated rates compounds errors across every bid you submit that year.