KPMG's 2023 Global Construction Survey found that 37% of respondents missed budget or schedule targets by 20% or more due to insufficient risk management. For heavy construction contractors, CFMA's Financial Benchmarker puts average net income before taxes at just 8.3% — meaning a modest cost overrun on a single large project can wipe out months of enterprise profit.

Cost reporting is the financial nervous system that prevents this. The difference between firms that protect margins and those that absorb overruns usually comes down to one thing: the quality, frequency, and speed of their cost reporting process.

Key Takeaways

- Cost reporting tracks all project financial activity — actuals, committed costs, forecasts, and variances — against the original budget

- The five core components are: budget baseline, actual/committed costs, ETC and EAC, change order management, and cash flow projections

- Effective cost reporting is an ongoing process, not a month-end task — it runs parallel to the project itself

- Common failure points: data lag, cost coding errors, and siloed field-office communication

- Automating cost reporting workflows helps firms catch margin fade earlier and free up finance teams for higher-value work

What Is Cost Reporting in Construction and Why Does It Matter?

Cost reporting is the systematic process of documenting, categorizing, and analyzing all financial activity on a construction project. It covers:

- Actual costs already incurred (labor paid, invoices processed, materials delivered)

- Committed costs (purchase orders placed, subcontracts executed but not yet invoiced)

- Forecasted costs to complete the remaining scope

- Variance against the original and revised budget

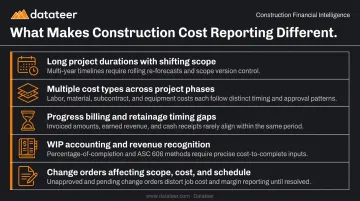

Why Construction Cost Reporting Is Different

Construction cost reporting isn't standard business accounting. Several factors set it apart:

- Long project durations with shifting scope and conditions

- Multiple cost types — direct, indirect, fixed, and variable — that interact differently across project phases

- Progress-based billing and retainage (typically 5–10%) that create timing gaps between work performed and cash received

- WIP accounting requirements where revenue is recognized as costs are incurred, not when billed or collected

- Change orders that alter scope, cost, and schedule simultaneously

What's at Stake Without It

Without accurate, timely cost reports, financial problems compound in silence. By the time the numbers surface in a monthly close, the damage is already done. Specifically:

- Project managers miss early overrun signals before costs escalate

- Finance teams can't produce defensible WIP schedules for sureties or lenders

- Executives lack the data to make sound decisions on resource allocation or new work pursuit

Key Components of a Construction Cost Report

A well-structured cost report brings together multiple interconnected elements — each tracking a different dimension of project finances — to give leadership a complete picture of where a project stands and where it's heading.

Budget Baseline and Revised Budget

The original budget (derived from the detailed cost estimate) is the financial benchmark for everything downstream. As approved change orders are executed, they update the revised budget. Every gap between original and revised budget must be formally documented, or variance analysis becomes unreliable and scope creep goes undetected.

Actual Costs and Committed Costs

These are not the same thing, and both must appear in the report:

- Actual costs: labor already paid, materials delivered, invoices processed

- Committed costs: purchase orders placed, subcontracts executed — financial obligations that haven't hit the books yet

Ignoring committed costs causes understated project exposure. A $200,000 subcontract executed last week is real financial liability even before the invoice arrives.

Estimated Cost to Complete (ETC) and Cost at Completion (EAC)

- ETC: the forward-looking projection of remaining spend needed to finish the project

- EAC: total projected final cost — costs to date plus ETC

When EAC is compared against the revised budget, it produces the projected over/under variance — the number that tells you whether the project is trending toward profit or loss.

Change Orders and Pending Cost Adjustments

Unapproved or pending change orders represent financial risk that must be tracked separately. Failing to document the cost impact of scope changes — even when approval is pending — is one of the most consistent drivers of undetected budget overruns. Per a 2025 US DOT Volpe report, change orders become necessary when proper cost controls aren't executed from the start.

Cash Flow Projections and Contingency Reserves

The cost report should include a cash flow forecast showing expected inflows and outflows by project phase. Construction cash flow is notoriously uneven: retainage withholds 5–10% of each draw, and progress billing cycles create gaps between work performed and payment received.

A cost report that omits cash flow timing gives an incomplete picture of project financial health, regardless of how accurately it tracks the cost side.

How Construction Cost Reporting Works: Step by Step

Effective cost reporting isn't a monthly task — it's an ongoing process that runs parallel to the project, requiring consistent inputs from both field and office.

Step 1 – Establish the Budget Baseline

Convert the final cost estimate into a project budget aligned to the firm's cost account structure and cost codes. The rigor applied here — including contingency allocation and cost code standardization — determines the accuracy of every report generated downstream. A weak baseline creates compounding errors across the entire project lifecycle.

Step 2 – Capture and Record Costs in Real Time

Document all expenditures as they occur:

- Labor hours and wages

- Material deliveries and invoices

- Equipment use and rental charges

- Subcontractor invoices and progress payments

Delayed data entry and batch-processing are where this step breaks down. Finance teams end up working with numbers that are 10–20 days out of date — and by the time the report is reviewed, the overrun has already deepened.

Step 3 – Forecast the Cost to Complete

Apply cost-to-complete (CTC) forecasting by analyzing current productivity rates, remaining work scope, and known risk factors to project ETC for each cost category. Linear extrapolation of current unit costs is the standard method. Adjust it when:

- Productivity is trending meaningfully up or down

- Scope has changed materially since the last forecast

- Known risk factors have shifted cost exposure

Step 4 – Manage and Integrate Change Orders

Establish a structured review and approval process for each change order, then immediately reflect:

- Approved changes in the revised budget

- Pending changes in the projected budget as tracked exposure

The cost report must always reconcile with the current contract value — not just the original estimate.

Step 5 – Produce and Distribute the Cost Report

Compile the full report — budget baseline, actuals, committed costs, ETC, EAC, change orders, cash flow projections, and projected over/under — and distribute at a cadence appropriate to the project's pace. Weekly or bi-weekly is standard for active projects.

Different audiences need different views:

- Field PMs need line-item visibility by cost code and phase

- Executives need portfolio-level summaries with red/yellow/green status indicators

Step 6 – Review, Adjust, and Act

Use the cost report as a decision-making tool, not a filing exercise. Identify variance items requiring investigation, update forecasts based on current field conditions, and carry lessons forward into future estimates. The firms that actually protect margins are the ones that act on findings before the job closes — not after:

- Reallocating resources when labor productivity slips below target

- Renegotiating change orders before they age into disputes

- Adjusting ETC forecasts when field conditions diverge from plan

A Real-World Cost Reporting Scenario

Consider a mid-size commercial construction firm three months into a 12-month project. Early cost reports show labor running 15% over budget on a specific phase due to productivity losses. Material costs are tracking on budget. On the surface, the project looks fine to anyone not reading the cost report carefully.

Without timely reporting, this labor slippage goes unnoticed. It compounds across the next phase and the one after that — each phase inheriting the same productivity problem. By month seven, the overrun is structural.

With a functioning cost report process, the sequence looks different:

- Finance isolates the variance — labor 15% over in Phase 2, all other categories on track

- ETC is updated for affected activities, adjusting the EAC upward

- The overage is flagged to the project manager with the specific cost codes driving it

- A mitigation path is executed — resource reallocation or a revised work plan — before the overrun becomes unrecoverable

The difference is timing. Forensic accounting finds the problem after it's baked in. Proactive cost management catches it while corrective action is still on the table. FMI's 2023 Labor Productivity Study estimated $30–40 billion lost annually to poor labor productivity — losses that accumulate precisely when cost reporting lags behind field reality.

Common Challenges in Construction Cost Reporting

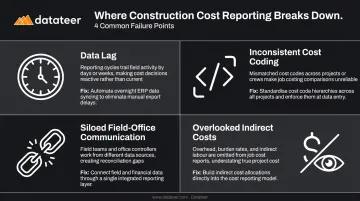

Even firms with structured processes struggle with consistency as project complexity and team size grow. The same four failure points surface repeatedly — and each one compounds the others.

Data Lag and Stale Reporting

When cost reports rely on manually compiled spreadsheets or batch-synced accounting data, finance teams may be working with numbers that are 10–20 days old by the time the report is reviewed. That's a wide window for margin fade, labor slippage, and underbilling to go undetected.

The fix: implement real-time or near-real-time data capture that syncs directly from the ERP, eliminating the lag between when costs occur and when they appear in the report.

Inconsistent Cost Coding

When field teams code expenses on the fly — misclassification follows. The result: distorted job cost reports and benchmarks too unreliable to use in future estimates.

The fix: standardize cost codes across all projects, enforce coding discipline at point of entry, and build review checkpoints into AP and payroll processes. Automated data standardization tools that remap inconsistent field entries before they reach the report layer can catch most of these errors automatically.

Siloed Field-Office Communication

When field teams and office finance teams operate in separate systems with no shared record, cost reports reflect the office's understanding of project financials — not ground truth. That gap creates real financial exposure: unlogged change orders, unrecorded labor, and cost overruns that don't surface until month-end.

One solution: establish a single source of truth where project managers, site supervisors, and finance staff all access and input into the same financial system.

Overlooking Indirect Costs and Contingencies

Many construction cost reports track direct costs (labor, materials, equipment) while underrepresenting indirect costs (administration, insurance, overhead allocation) and failing to document contingency drawdowns. This understates true project cost and distorts profitability projections.

The fix: build indirect cost allocation into the project budget from the start and create a clear process for documenting when and why contingency funds are accessed.

How Datateer Can Help

Datateer is a financial analytics platform built specifically for construction, not a generic BI tool retrofitted to it. The platform integrates directly with 12+ construction ERPs — Procore, Sage 100/300/Intacct, Viewpoint Vista, Viewpoint Spectrum, Acumatica, Foundation Software, CMiC, Jonas Construction, and others — automatically extracting, cleaning, and standardizing financial data into construction-specific dashboards.

Specific Impact on Cost Reporting

For construction finance managers dealing with the challenges described above, Datateer addresses them directly:

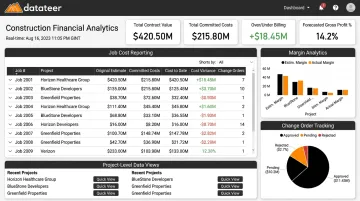

- Job Costing & Cost-to-Complete Analytics — real-time visibility into actual costs, committed costs (POs and subcontracts), pending change orders, projected final cost, and variance to budget at job, phase, and cost-code level

- Cost Variance Reporting (Budget vs. Actual) — continuous in-month variance tracking with trend analysis showing whether a job is converging or diverging from target, including drill-down to source transactions in the ERP

- Margin Protection & Margin Fade Prevention — monitors original estimated margin versus current projected margin per job, flagging the specific cost codes and phases driving deterioration

- Change Order Impact & Aging Analytics — tracks pending, approved, and denied change orders with aging by days since submission, surfacing stalled change orders before their cost impact locks in

- 13-Week Cash Flow Forecasting — automated projection based on real-time project burn rates and retainage schedules

The data updates overnight, replacing the 10–20 day manual reporting lag with current numbers. Double L Management's team put it directly: "That one click replaced two weeks worth of prior work."

What Changes for the Finance Team

With data extraction and report generation handled automatically, construction finance managers stop spending their week reformatting spreadsheets. Instead, they act as strategic partners — using clean, current cost data to advise project teams, protect margins, and inform resource decisions.

That shift is accessible regardless of firm size. Datateer serves construction firms from $10M to over $1B in annual revenue, with:

- Flat annual pricing starting at $10,000/year per data source

- Unlimited users across the full dashboard suite

- 2–4 week implementation timeline

Firms like Acme Constructors, Morris-Shea Bridge Company, and Double L Management use the platform to replace manual cost reporting workflows with automated, always-current financial intelligence.

Frequently Asked Questions

How do you keep track of construction expenses?

Three practices matter most:

- Assign every cost to a specific job cost code in your ERP or accounting system

- Capture actuals as they occur, not in batches

- Reconcile tracked expenses against budget in regular cost report reviews

Real-time entry is the linchpin — delayed logging creates data lag that makes overruns invisible until they compound.

What are the five basic financial reports in construction?

The five most commonly referenced are the WIP report, job cost report, balance sheet, income statement, and cash flow statement. The WIP and job cost reports are the most operationally critical for day-to-day project financial management, since they directly track earned revenue, cost performance, and billing status.

What programs do construction companies use to track budgets and projects?

Most construction firms rely on ERPs like Procore, Sage 300, Vista by Viewpoint, Acumatica, Foundation Software, or CMiC for core financial tracking. These are often supplemented by financial reporting platforms like Datateer, which pull data from those ERPs into real-time dashboards without requiring manual exports or spreadsheet work.

What is included in a construction cost report?

A complete cost report covers:

- Original budget, approved change orders, and revised budget

- Committed costs and actual costs to date

- Estimated cost to complete (ETC) and estimated cost at completion (EAC)

- Cash flow projections and projected over/under variance

Track pending change orders separately — they represent additional exposure not yet in the baseline.

What is cost-to-complete forecasting in construction?

Cost-to-complete (CTC) forecasting estimates how much additional spend is needed to finish remaining scope, using current productivity rates, remaining quantities, and known cost variables. It feeds directly into the EAC calculation and is the primary input for projecting final project profitability.

How often should construction cost reports be updated?

Best practice is weekly or bi-weekly for active projects, with frequency increasing as a project approaches completion or enters a high-risk phase. Firms using ERP-connected dashboards can maintain a continuously updated cost picture rather than depending on periodic manual compilations.