This guide covers the four formal estimation methods used across the industry, the mistakes that most reliably blow budgets, six proven prevention strategies, and the warning signs that should trigger immediate investigation on any active project.

TL;DR — Key Takeaways

- Most overruns originate in the estimate, not the field — bad inputs produce bad budget baselines

- Four estimation methods exist (analogous, parametric, bottom-up, three-point); using the wrong one for your project phase creates structural risk

- Scope creep, stale labor rates, and omitted indirect costs are the top budget killers

- Prevention requires both pre-project rigor and mid-project monitoring — neither alone is sufficient

- Real-time budget-vs-actual visibility catches overruns while correction is still possible — monthly reports rarely do

Why Construction Cost Overruns Are a Finance Problem, Not Just a Field Problem

The default explanation for overruns points to the field: weather delays, crew productivity issues, material delivery problems. Those factors are real — but for construction finance teams, they're secondary to a more dangerous problem: a data visibility gap that lets overruns compound for weeks before anyone in finance sees them.

McKinsey's analysis of large capital projects found that cost overruns averaged at least 79% relative to initial budget estimates, while schedule delays averaged 52% relative to initial timelines. Even in less extreme contexts, KPMG's 2023 Global Construction Survey found 37% of respondents missed budget and/or schedule targets — meaning overruns are not edge cases.

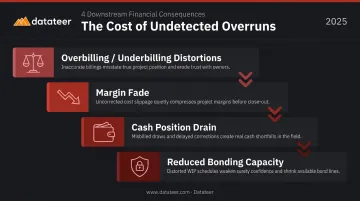

The Downstream Financial Consequences

When overruns go undetected through traditional monthly reporting cycles, the damage isn't just to job margin. The cascade hits multiple dimensions:

- Overbilling/underbilling distortions — CFMA notes that high underbillings relative to equity cause sureties and banks to question actual profitability and management effectiveness

- Margin fade — projected profit on in-progress work deteriorates while the WIP report sits unassembled

- Cash position — labor and material costs continue while billing lags, draining working capital

- Bonding capacity — surety underwriters evaluate financial strength, contract schedules, and cash flow; deteriorating numbers on any of these dimensions can reduce bonding availability

By the time a manual WIP report is assembled (pulling ERP data, reconciling cost codes, formatting in Excel), the data is already 10–20 days stale. Finance teams are making decisions against project numbers that no longer reflect what's happening on the ground today.

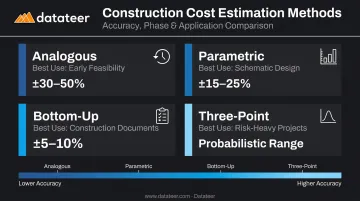

The Four Methods Used to Estimate Construction Costs

Experienced estimators match their method to how much design information is available and how much accuracy the situation demands. Getting this wrong (using a rough analogous estimate where a bottom-up is required, or skipping probabilistic analysis when risk is high) is itself a source of overruns.

Analogous Estimating (Top-Down)

Analogous estimating draws on cost data from similar completed projects to produce a fast, high-level estimate. It's the basis for cost-per-square-foot benchmarks and thumb-rule approaches.

Useful for early feasibility assessments and pre-bid screening. The AACE estimate classification framework puts early-phase estimates (Class 4–5) at accuracy ranges of -15% to -30% on the low side and +20% to +50% on the high side — far wider than the commonly cited ±20–30%.

Using outdated benchmarks, or benchmarks from structurally different project types, can push you well outside even those ranges before a single shovel hits the ground.

Parametric Estimating

Parametric estimating builds cost using statistical relationships between project variables: cost per linear foot of pipe, cost per ton of steel, cost per installed unit. It scales these parameters to the current project scope.

More accurate than analogous when the underlying data is solid. Parameters sourced from projects completed 18–24 months ago, or from different regional markets, carry systematic errors. When those errors multiply across thousands of units, the cumulative variance can erase your contingency before construction starts.

Bottom-Up Estimating

Bottom-up is the most granular and most defensible method. It builds total project cost from individual work packages, tasks, materials, and labor hours — aggregating up to a project total.

This is the standard for competitive bidding. It requires near-complete design documents and is the most time-intensive approach.

The compounding risk is easy to miss: when dozens or hundreds of line items are each underestimated by modest amounts, those variances stack. A 3% underestimate across 400 line items isn't a 3% problem — it's a 3% error repeated 400 times.

Datateer's Job Costing & Cost-to-Complete Analytics module tracks actuals at this same cost-code level. Variance between the bottom-up estimate and field performance becomes visible in real time rather than at closeout.

Three-Point Estimating

Three-point estimating generates an optimistic estimate, a most-likely estimate, and a pessimistic estimate — then produces a weighted expected cost with a built-in risk range.

This method is particularly useful for construction finance teams because it replaces false precision with a probabilistic range that directly informs contingency planning. Knowing your cost range spans $4.2M to $5.8M rather than a single-point $4.9M changes how you set contingency — and how you communicate risk to owners and leadership.

The Most Common Estimation Mistakes That Lead to Overruns

Using Stale Cost Data

Material prices don't move gradually — they spike and crash. BLS Producer Price Index data shows softwood lumber prices rose approximately 174% between April 2020 and May 2021, then fell roughly 53% by September 2021. Steel mill products followed a similar trajectory, rising about 153% between mid-2020 and late 2021.

An estimate built on pricing data from 12–18 months prior can be structurally mispriced before mobilization. For firms bidding competitive work over multi-month procurement cycles, that pricing gap becomes a margin problem baked into the baseline before the first shovel hits ground.

Omitting Indirect and Soft Costs

Estimators focused on hard costs routinely undercount or miss entirely:

- Permit and inspection fees

- Equipment mobilization and demobilization

- Temporary utilities and site facilities

- Project management and superintendent overhead

- Insurance and bonding costs

- Design and engineering fees (on design-build work)

AACE defines field indirects as costs that don't become part of the final installation but are required for project completion. Firms that don't maintain a standard indirect cost checklist by project type leave consistent gaps in their estimates.

Underestimating Labor Using Best-Case Productivity

FMI's 2023 Labor Productivity Study of more than 250 senior leaders from self-performing contractors found $30–$40 billion lost annually to poor productivity, with roughly 60% of respondents believing 11% or more of field labor costs are wasted. When labor is the largest line item and actual productivity runs below estimate, the overrun compounds fast.

Using theoretical productivity rates instead of actual historical averages from your own crews and trade partners sets an unrealistic baseline from day one.

Bidding to Win Rather Than to Be Profitable

Shaving labor hours and using lowest-possible material prices to sharpen a bid sets a margin ceiling before first mobilization. The finance team often has no visibility into these assumptions until the WIP surfaces an under-margin job. Two warning signs to catch early:

- Compressed labor hours relative to crew historical averages

- Material pricing below recent actuals without a documented procurement rationale

Ignoring Change Order Probability

On renovations, ground-up commercial work, and design-build projects, change orders are near-certain, not exceptions. Estimators who don't build a realistic expectation of change order volume into their risk-adjusted budget are assuming perfect scope stability. Building even a modest change order contingency into the baseline — informed by historical data from similar project types — is a more defensible starting point than assuming clean scope through closeout.

How to Prevent Construction Cost Overruns: 6 Proven Strategies

Strategy 1: Build Estimates from Your Own Historical Job Cost Data

Industry averages are a starting point. The most reliable estimates come from budget-to-actual comparisons across your own completed projects, tracked by trade, cost code, and project type. Firms that close out job costs rigorously build a benchmark database that makes each successive estimate structurally more accurate.

Strategy 2: Lock In Scope Before Locking In Price

A detailed, contract-level scope of work should define inclusions, exclusions, and assumptions explicitly. Every assumption left unwritten in the estimate is a potential change order — and a potential overrun — waiting to materialize.

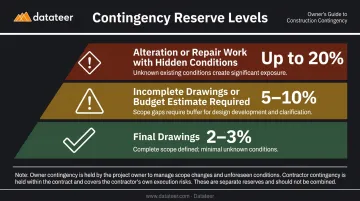

Strategy 3: Build Contingency Correctly — and Protect It

Contingency is a risk reserve for legitimate unknowns, not a buffer for imprecise estimating. RSMeans guidance suggests 2–3% when drawings are final and only field contingencies remain; 5–10% when drawings are incomplete or a budget estimate is required; and up to 20% on alteration or repair work.

Renovation and remodel projects warrant higher contingency due to hidden conditions. Owner contingency and contractor contingency should be documented separately, with clear rules governing each.

Strategy 4: Enforce a Mandatory Change Order Process — Zero Exceptions

Every scope addition must be documented, priced, and approved in writing before work begins. Verbal approvals and "we'll figure it out later" agreements are where significant margin disappears on otherwise well-managed projects.

Strategy 5: Track Committed Costs, Not Just Invoiced Costs

A project that looks on-budget based on invoices can already be structurally over-budget based on commitments. Purchase orders placed and subcontracts signed are financial obligations that must be tracked alongside invoiced amounts — not discovered at month-end.

Datateer's Job Costing & Cost-to-Complete module pulls both actual costs and committed costs directly from ERP integrations, so your projected final cost reflects the full picture rather than just what's been billed.

Strategy 6: Conduct Weekly Budget-vs.-Actual Reviews, Not Monthly

Monthly reviews are too slow. A weekly 30–45 minute cost review — covering labor hours burned, material invoices, subcontractor billings, and committed costs by cost code — creates the feedback loop that keeps small variances from becoming unrecoverable overruns. This requires current cost data, which is exactly where Excel-based processes break down.

Warning Signs Your Project Is Already Going Over Budget

These signals should trigger immediate investigation, not a footnote in next month's review.

Committed costs are outpacing percent-complete. If a project has consumed 60% of its budget but only 40% of the work scope is complete, the final cost trajectory is already showing an overrun. This is a basic earned value signal: cost performance index below 1.0 demands a cost-to-complete reset.

Datateer's Job Costing module surfaces CPI and Schedule Performance Index as standard earned value metrics, so this signal is visible continuously rather than at month-end.

Labor hours are trending above estimate at the task level. Aggregate labor tracking masks problems. If concrete work was estimated at 200 hours and has consumed 160 hours with only 50% of that scope complete, the math is already wrong.

Datateer's Labor & Materials Productivity dashboards surface this type of cost-code-level labor variance. The goal is catching the blowout on Tuesday, not three weeks after payroll is cut.

Approved change orders haven't been reflected in the revised budget. When change order work is underway but the project budget hasn't been updated, the finance team is comparing actuals against the wrong baseline. Every approved change order must immediately update the revised project budget. A budget that still reflects original contract value on a project with $400K in approved changes is producing misleading variance data.

How Real-Time Financial Visibility Keeps Construction Overruns in Check

Traditional reporting creates a structural lag problem. Assembling a monthly WIP report — pulling ERP exports, reconciling cost codes, building the Excel model, distributing for review — puts 10–20 days between when data is current and when it reaches decision-makers. By then, the project has moved on. The report describes what happened, not what's happening.

What changes with real-time budget-vs-actual dashboards that sync directly from the ERP:

- Labor slippage is visible the next morning, not at month-end

- Committed costs appear as soon as POs are entered, not when invoices arrive

- Margin fade shows up while corrective action is still possible

- The CFM's role shifts from forensic accounting to proactive financial management

Datateer automates the full data flow from ERP to executive dashboards for construction firms ranging from $10M to $1B+ in annual revenue. The platform integrates with Procore, Sage 100/300/Intacct, Viewpoint Vista, Viewpoint Spectrum, Acumatica Construction, Foundation Software, CMiC, Jonas, QuickBooks, NetSuite, and others, with overnight sync as standard and configurable higher frequency when needed.

A business analyst at Double L Management noted that the first time they accessed their data through Datateer's dashboards, "that one click replaced two weeks worth of prior work."

That same real-time monitoring compounds over time. When your actual cost-per-unit and labor productivity rates come from a continuously updated database rather than a three-year-old spreadsheet, each successive estimate starts from a more accurate baseline.

Frequently Asked Questions

How to prevent cost overruns in construction projects?

Prevention requires accurate estimates built from your own historical data, explicit scope documentation before pricing, mandatory written change orders, appropriate contingency reserves, and weekly cost-code-level budget reviews during execution. Each element reinforces the others — gaps in any one area tend to surface as budget problems downstream.

What four methods are used to estimate construction costs?

The four standard methods are:

- Analogous: Historical benchmarking from comparable past projects

- Parametric: Statistical scaling by unit (cost per SF, cost per unit)

- Bottom-up: Task-level rollup to a total project cost

- Three-point: Risk-range weighting across optimistic, likely, and pessimistic scenarios

Method selection depends on available design documentation and the accuracy level the project phase requires.

What is the thumb rule for construction cost?

Thumb rules are shortcut estimates based on cost per square foot, cost per unit, or percentage-based benchmarks for specific project types. They're useful for early feasibility screening but carry accuracy ranges of -15% to -30% or wider — not a substitute for a detailed bottom-up estimate before competitive bidding.

What is the most common cause of construction cost overruns?

Two drivers account for the majority: inaccurate estimation (stale data, underestimated labor, omitted indirect costs) and unmanaged scope creep (changes executed without documented and approved change orders). When both are present simultaneously, overruns compound quickly and become harder to recover from mid-project than either factor alone.

What percentage should I budget for construction contingency?

RSMeans recommends 2–3% when drawings are final, 5–10% when drawings are incomplete, and up to 20% for alteration and repair work. Renovation projects with potential hidden conditions warrant higher reserves. Contingency should be documented for legitimate unknowns — not structured to compensate for weak estimating.

How does real-time financial reporting help prevent construction cost overruns?

Real-time budget-vs-actual visibility surfaces labor slippage, cost code variances, committed cost overruns, and margin fade as they develop — not at job closeout. This gives finance teams and project managers the lead time needed to intervene, adjust resources, or accelerate change order processing before the overrun becomes unrecoverable.