For construction finance managers, CFOs, and CPAs advising contractors, this distinction matters enormously. Projects spanning multiple fiscal years make end-of-project recognition misleading to lenders, bonding companies, and internal decision-makers. PCM solves that problem by matching revenue to reality.

The catch: PCM is frequently misapplied. Many contractors run the formula once a quarter, rely on spreadsheets assembled days after period-end, and then wonder why margin surprises keep appearing. This guide walks through exactly how PCM works, how to calculate it step by step, and where it most commonly breaks down.

Key Takeaways

- PCM recognizes revenue based on work performed, not billing amounts. The formula: % Complete = Costs Incurred ÷ Total Estimated Costs

- Revenue Earned = % Complete × Contract Price** — this drives your income statement, not your invoices

- The WIP schedule consolidates PCM across all active jobs and must be updated monthly to be useful

- Overbillings are a liability; underbillings are an asset, and both signal cash flow and margin risk

- The IRS requires PCM for most long-term contracts; the small contractor exception covers firms under $32M gross receipts (2026) with contracts completing within two years

What Is the Percentage of Completion Method?

The percentage of completion method (PCM) is a revenue recognition approach built for long-term contracts—typically those spanning more than one fiscal year. Rather than waiting until project completion to record income, PCM aligns recognized revenue with the actual proportion of work performed each period.

The goal is to produce financial statements that reflect a contractor's true position at any point in time. That accuracy matters for cash flow forecasting, evaluating bonding capacity, and giving stakeholders a picture that isn't distorted by billing timing.

How PCM Differs from the Completed Contract Method

The completed contract method (CCM) defers all revenue and expense recognition until the contract is substantially finished. That simplicity comes at a cost: a three-year project shows zero revenue for two years, then records everything in year three.

For lenders and surety companies reviewing financials, those swings are artificial and make trend analysis meaningless. PCM eliminates that volatility by distributing recognition across the project's life.

CCM does have legitimate uses, including:

- Short-duration projects completing within the same tax year

- Home construction contracts

- Situations where reliable cost estimation isn't feasible

Outside those scenarios, the revenue swings CCM creates are a liability — not a feature. For commercial contractors running multi-period projects, PCM gives lenders, sureties, and internal leadership a financial picture that actually tracks with project reality.

How the Percentage of Completion Method Works

PCM requires four inputs:

| Input | Description |

|---|---|

| Contract Price | Total agreed amount, including approved change orders |

| Total Estimated Cost | All projected direct and indirect costs to complete |

| Costs Incurred to Date | Actual cumulative costs as of the reporting period end |

| Progress Billings | Total invoiced to the client to date |

The most widely used approach for measuring completion is the cost-to-cost method: costs incurred are a reliable proxy for work performed. Treasury Regulation Section 1.460-4 defines completion percentage as cumulative allocable contract costs incurred divided by estimated total allocable contract costs.

Alternative measures exist under ASC 606—output methods like milestones or units delivered, and input methods like labor hours—but cost-to-cost remains standard for general contracting.

Whichever method you use, every downstream PCM calculation is only as good as your estimate at completion (EAC). A stale EAC contaminates percent complete, earned revenue, and the WIP schedule at once — all three go wrong together.

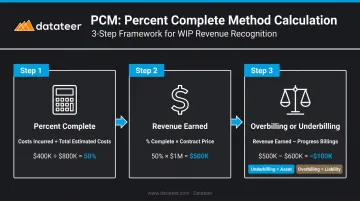

Step 1: Calculate Percent Complete

Formula: Percent Complete = Costs Incurred to Date ÷ Total Estimated Costs

Example: $400,000 incurred ÷ $800,000 estimated = 50% complete

Step 2: Calculate Revenue Earned to Date

Formula: Revenue Earned = % Complete × Contract Price

Example: 50% × $1,000,000 contract = $500,000 earned revenue

This $500,000 appears on the income statement regardless of how much has been billed. Revenue follows performance, not invoicing.

Step 3: Determine Overbilling or Underbilling

Formula: Underbilling (or Overbilling) = Revenue Earned − Progress Billings

- Positive result = Underbilling → asset on the balance sheet (earned more than billed)

- Negative result = Overbilling → liability on the balance sheet (billed ahead of work performed)

Using the example: if progress billings are $600,000 against $500,000 earned, the contractor has an overbilling of $100,000—a liability representing revenue not yet supported by completed work.

Overbillings, Underbillings, and the WIP Schedule

The WIP (Work-in-Progress) schedule is the operational report that consolidates PCM calculations across all active contracts. Per AICPA-CIMA guidance, it's the blueprint for construction accounting—tracking contract value, estimated cost, costs to date, percent complete, earned revenue, billed amount, and the resulting over/underbilling position for every job.

Why Monthly Updates Are Non-Negotiable

Contractors who produce WIP reports only at quarter-end or for year-end audits are making bonding, backlog, and cash flow decisions on outdated information. By the time a quarterly WIP reveals a problem, the margin damage is often done.

What each position signals:

- Persistent underbilling: The contractor is funding work it hasn't invoiced yet—a cash flow crisis quietly building

- Persistent overbilling: Billings have outpaced completed work, leaving insufficient revenue to cover remaining costs—and a margin shortfall that compounds the longer it goes unaddressed

Surety companies and lenders scrutinize these ratios closely. An overbilling-heavy WIP schedule raises immediate questions about whether future revenue can cover remaining costs.

From Manual Assembly to Live Visibility

The traditional WIP assembly process—CSV exports, VLOOKUP reconciliation between Procore and Sage, manual consolidation across job spreadsheets—routinely consumes 10 to 20 days of finance team time each month. By the time the WIP report is ready, it's already describing the past.

Datateer's WIP Reporting module replaces that process with automated schedules pulled directly from the ERP overnight. According to Double L Management's business analyst: "That one click replaced two weeks worth of prior work."

The platform syncs with Procore, Sage, Viewpoint Vista, Acumatica Construction, Foundation Software, and a dozen other construction ERPs—calculating percent complete, earned revenue, and overbilling/underbilling positions per job automatically. Real-time margin fade detection flags deterioration before month-end is locked in.

Common Errors and Risks with PCM

Most PCM failures trace back to data quality, not formula complexity. Here are the four most common breakdowns:

Stale Cost Estimates

When project managers don't revise their cost-to-complete forecasts as field conditions change, every downstream number is wrong. The AICPA Practice Alert 2000-3 notes that the longer the contract period, the greater the risk that an estimate will be incorrect.

Here's how a single $50,000 underestimate compounds: on a $1,000,000 contract with $800,000 in estimated costs, that error inflates percent complete from 50% to roughly 52.6%, overstating earned revenue by $26,000 — and simultaneously misstates the overbilling/underbilling position. All from one stale input.

Change Orders Entered Late

PCM requires contract price and estimated costs to be updated the moment a change order is approved. Contractors who batch change orders at month-end run their WIP calculations on outdated contract values, producing sudden unexplained jumps in recognized revenue when the entries finally post. Datateer's Change Order Impact & Aging module tracks change orders through their full lifecycle (pending, approved, denied, executed) and flags stalled approvals that are creating margin exposure before they hit the WIP schedule.

Stored Materials Inflating Percent Complete

Materials delivered to the job site but not yet installed represent costs incurred without completed work. Including them in the cost-to-cost calculation overstates percent complete and inflates earned revenue. Under ASC 606, revenue on uninstalled materials may only be recognized to the extent of cost, with no profit margin. This is a common audit finding and a genuine misrepresentation of project progress.

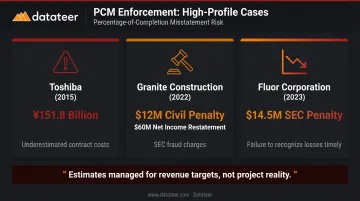

Front-Loading and Deliberate Misuse

When early-stage costs are low but initial billings are high, overbilling positions can mask losses building beneath the surface. Regulators have pursued this aggressively — three enforcement actions in the past decade illustrate the financial and legal exposure:

- Toshiba (2015): ¥151.8 billion in pre-tax income adjustments traced to PCM misuse — underestimated total contract costs and delayed loss recognition

- Granite Construction (2022): SEC fraud charges resulting in a $12 million civil penalty after the company restated net income by $60 million for 2017

- Fluor Corporation (2023): $14.5 million SEC penalty for overly optimistic cost estimates and failure to recognize losses on time

In each case, the root cause was the same: estimates managed for revenue targets rather than updated to reflect actual project conditions. The antidote is a systematic review cycle that catches stale inputs before they compound.

GAAP, IRS Requirements, and When PCM Isn't Mandatory

IRS Rules Under IRC Section 460

IRC Section 460 defines a long-term contract as any building, installation, or construction contract not completed within the taxable year it's entered. For these contracts, taxable income must generally be determined under PCM.

The small contractor exception has two required conditions:

- The contract must be expected to complete within two years of commencement

- The contractor's average annual gross receipts for the prior three years must not exceed the Section 448(c) threshold—set at $32,000,000 for taxable years beginning in 2026 per IRS Rev. Proc. 2025-32

Both conditions must be satisfied. Tax shelters are excluded from the exception regardless of size.

Home construction contracts are separately exempt when 80% or more of estimated total contract costs relate to dwelling units in buildings with four or fewer units and directly related site improvements.

GAAP Under ASC 606

PCM by name was superseded when ASC 606 took effect—for public companies, annual periods beginning after December 15, 2017; for private companies, annual periods beginning after December 15, 2018.

ASC 606 uses a five-step revenue recognition model, with revenue recognized over time when one of three criteria is met:

- The customer simultaneously receives and consumes the benefits of performance

- The contractor creates or enhances an asset the customer controls as it's created

- Performance doesn't create an asset with an alternative use and the contractor has an enforceable right to payment for work completed to date

Most commercial construction contracts satisfy at least one criterion, so ASC 606's over-time recognition typically produces the same result as traditional cost-to-cost PCM. The cost-to-cost percentage calculation stays the same; what changes is the five-step framework contractors must document to support it.

For firms managing multiple concurrent contracts, automating that documentation—per job, per period, per performance obligation—is where platforms like Datateer's ASC 606 Revenue Recognition module add the most operational value.

Conclusion

PCM does one thing: it makes sure revenue reported in any period reflects actual work completed—not billing timing, not project completion, not cash received. That accuracy is what makes financial statements meaningful to lenders, surety companies, and the people running the business.

The formula itself is simple enough. What breaks down is the data behind it:

- Cost estimates that go stale mid-project

- Change orders entered weeks after the fact

- Stored materials coded as installed work

Contractors who treat PCM as an annual audit exercise rather than a live management discipline are building margin surprises into every project.

Monthly WIP updates, timely change order entry, and honest cost-to-complete forecasting are the actual work of financial management in construction. Everything else is cleanup.

If your team is still assembling WIP from spreadsheets and ERP exports, Datateer's 15-Minute Workflow Audit is a no-pitch starting point to see what automated WIP and cost-to-complete analytics look like with your own data.

Frequently Asked Questions

What is the formula for the percentage of completion method?

Percent Complete = Costs Incurred to Date ÷ Total Estimated Costs. That percentage is then multiplied by the total contract price to calculate Revenue Earned to Date. Progress billings are compared to earned revenue to determine overbilling or underbilling.

What is the POC method?

POC (percentage of completion) and PCM refer to the same approach: an accounting method used in construction and other long-term contract industries that recognizes revenue incrementally as work progresses, rather than deferring everything to project completion.

Is the percentage of completion method GAAP?

ASC 606 replaced the PCM label, but the underlying principle survives. For long-term construction contracts where control transfers over time and progress can be reliably measured, ASC 606's over-time recognition produces the same result as traditional cost-to-cost PCM and is fully GAAP-compliant.

What is the difference between overbilling and underbilling?

Underbilling means a contractor has earned more revenue than it has billed, recorded as an asset. Overbilling means billings exceed earned revenue, recorded as a liability. Both are calculated from the WIP schedule by comparing earned revenue to progress billings.

How often should contractors update their WIP schedule?

Monthly at minimum. Bonding, cash flow, and backlog decisions all depend on current data. Contractors relying on quarterly or year-end updates are making strategic decisions on information that no longer reflects where jobs actually stand.