For finance teams managing 15, 20, or 30 active jobs simultaneously, that erosion pattern is the real risk. A healthy company-level P&L can mask two or three deteriorating projects until the quarterly close forces the reckoning.

This article covers what a construction budget actually contains, how to build one that holds up, the failure modes that cause most overruns, and the practices — and tools — that keep margin intact from mobilization to closeout.

Key Takeaways

- Budget overruns are structural, not accidental — inaccurate estimates, untracked change orders, and optimistic cost-to-complete projections are the usual culprits

- Reliable budgets need a Work Breakdown Structure, fully burdened labor costs, and a contingency reserve scaled to actual project risk

- Finance and PMs should review budgets together weekly — accounting actuals alone miss what's happening in the field

- Real-time financial visibility closes the gap between field costs incurred and leadership decisions made

- A 10–20 day WIP reporting lag is where margin quietly disappears

What Makes Construction Budget Management Uniquely Complex

Multiple jobs, one P&L — and the gap between them

Construction firms don't manage one budget. They manage a portfolio — often 15 to 40 concurrent projects, each with its own cost structure, subcontractor mix, and completion timeline. The company-level income statement averages across all of them, which means a few strong jobs can obscure a deteriorating one until it's too late to course-correct.

Job-level budget control is the only layer where margin is actually made or lost. That's an accounting reality, not a platitude. McKinsey's analysis of 532 large global projects found average cost overruns of at least 79% versus initial budget estimates. Even accounting for the megaproject sample, the implication is hard to dismiss.

Percentage-of-completion creates a financial reporting risk, not just an ops issue

Under percentage-of-completion accounting, revenue recognized in a period is tied directly to costs incurred versus total estimated costs. If the cost-to-complete estimate is wrong — whether through optimism, incomplete field data, or untracked change orders — reported revenue is wrong too.

This isn't a project management problem that finance can observe from a distance. Inaccurate CTC estimates produce misstated financials.

The RSM 2025 construction revenue recognition guidance confirms that under ASC 606, pending and unpriced change orders are treated as variable consideration — included in the transaction price only when it's probable that a significant revenue reversal won't occur. Firms that include pending change orders in contract value before that threshold is met are overstating revenue, not just being optimistic.

The field-to-office gap and its downstream consequences

Field costs — labor hours, materials consumed, subcontractor work completed — take days or weeks to surface in financial systems. Finance teams end up making decisions on data that's already stale. A WIP schedule is only as accurate as the data feeding it, and delayed percent-complete updates make revenue recognition unreliable.

Those effects accumulate fast:

- Cash flow strain from billing timing mismatches and unresolved change orders

- Damaged bonding capacity — sureties evaluate WIP schedules closely, and inconsistency raises flags

- Lender hesitation when reported job margins shift sharply at period-end

- Reduced bidding capacity when working capital is tied up in deteriorating jobs

Key Components of a Construction Budget

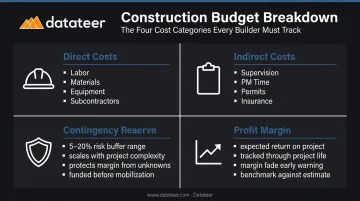

Every construction budget, regardless of project type or size, contains four core cost categories:

| Category | What It Includes |

|---|---|

| Direct costs | Labor (including burden), materials, equipment, subcontractors |

| Indirect costs | Supervision, PM time, permits, insurance, temporary facilities |

| Contingency reserve | Risk buffer, typically 5–20% depending on project complexity |

| Profit margin | The contractor's expected return, tracked throughout the project life |

Project budget vs. company annual budget

These are distinct tools that serve different purposes:

- The project budget is a job-level control document: it defines scope, allocates cost by category, and becomes the baseline against which actuals are measured

- The company annual budget is a portfolio-level planning tool: it aggregates expected revenue, overhead, and profit across all projected work

The project budget is where margin is protected. The annual budget is where leadership assesses capacity, overhead recovery, and growth trajectory. Both require precision, but the project budget is the active control mechanism.

Why cost codes matter more than most firms realize

Cost codes organize budget lines by phase, task, or resource type. Without consistent cost code discipline, job costing comparisons break down, variance analysis becomes guesswork, and historical data stops being a reliable benchmark.

That manual reconciliation burden — matching Procore project commits against Sage invoices before every close — is one of the most common time sinks in construction finance. Datateer's automated data extraction handles cost code standardization across ERP and project management systems, so finance teams get clean, normalized data without the manual cleanup.

How to Create a Construction Budget Step by Step

Step 1: Define scope using a Work Breakdown Structure

A WBS breaks the project into discrete phases and deliverables (foundation, structural, MEP rough-in, finishes, closeout). This structure becomes the scaffolding for every downstream cost estimate and makes budget-vs.-actual tracking possible at the task level, not just the job level. Without it, variance analysis tells you a job is over budget — but not where or why.

Step 2: Estimate direct and indirect costs — fully burdened

Labor is where most estimates go wrong. BLS data from March 2025 shows that total employer compensation in private construction averaged $48.58 per hour — with wages at $33.79 and benefits at $14.79, or roughly 30% on top of wages. Firms that price labor using wage rates alone are underestimating by nearly a third before the first shovel hits the ground.

Estimate each cost category explicitly:

- Labor: Wage rates plus burden (FICA, workers' comp, benefits, fringes)

- Subcontractors: Hard bids where possible; allowances flagged clearly as assumptions

- Materials: Quantity takeoffs with current unit prices, not last year's pricing

- Equipment: Ownership costs or rental rates, utilization assumptions

- Indirect costs: PM and superintendent time allocated to the job, permits, insurance, temporary facilities

Step 3: Set contingency based on actual project risk

Contingency isn't a flat rule. The appropriate reserve depends on how well-defined the project scope is and how much execution risk the contractor is absorbing.

- 5–10%: Well-defined scope, familiar project type, stable subcontractor market, fixed-price contract

- 10–15%: Some design uncertainty, fast-track schedule, competitive subcontractor bids

- 15–20%+: Design-build delivery, complex site conditions, early-phase estimates, significant material price exposure

Distinguish between owner contingency (scope additions, design changes) and contractor contingency (labor inefficiency, execution variability). They serve different purposes and shouldn't be pooled.

Step 4: Establish a change order protocol before work begins

Two failure modes destroy change order discipline:

- Verbal approvals that never get formally processed, creating scope delivered but not contracted

- Pending change orders included in contract value before they meet the ASC 606 revenue recognition threshold

Both produce budget distortion that compounds over the project life. Before mobilization, define in writing: who can authorize scope changes, what documentation is required, and how approved, pending, and unsubmitted changes are handled in accounting.

Step 5: Define the variance analysis cadence

A budget that isn't reviewed regularly is a historical record, not a control tool. Establish monthly joint reviews (bi-weekly on larger jobs) between project managers and finance that include:

- Costs incurred to date (from accounting)

- Costs committed but not yet invoiced (POs, subcontracts)

- PM's updated cost-to-complete estimate, broken down by cost category

- Resulting projected final cost and margin

The PM's CTC estimate is required, not optional. Accounting actuals alone show what's already happened; without a forward-looking cost estimate, there's no basis for corrective action.

Common Causes of Budget Overruns — and How to Catch Them Early

Change order erosion

Budget drift most often starts not from catastrophic events but from approved-but-unprocessed scope changes. A single untracked change order creates cascading problems: understated CTC, billing disputes, and potential revenue misstatement under percentage-of-completion.

The remedy is a tiered tracking system with clear accounting rules for each stage:

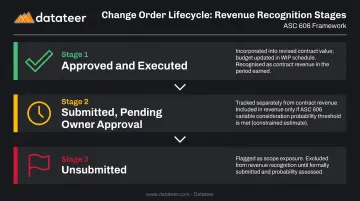

- Approved and executed: Incorporated into revised contract value; budget updated

- Submitted, pending owner approval: Tracked separately; included in revenue only if ASC 606 probability threshold is met

- Unsubmitted: Flagged as scope exposure; not included in revenue

Datateer's Change Order Impact & Aging module tracks change orders across the full lifecycle — pending, approved, denied, and executed — with aging by days since submission and revenue and margin impact by cost code and phase.

Indirect cost misallocation

When PM, superintendent, and estimator time isn't documented to specific jobs, those costs default to G&A. Individual jobs then look more profitable than they are, and company-level operating margin gets compressed. Under percentage-of-completion, misallocated indirect costs also suppress revenue recognition on the jobs that consumed them.

FMI notes that variable overhead runs 1–3% of revenue for most contractors. At scale, that's meaningful — and systematically understated when indirect labor isn't tracked to jobs.

Cost-to-complete optimism

The CTC trend problem is subtle but predictable: project managers who consistently revise their remaining cost estimates downward as jobs progress tend to produce negative gain/fade at completion. Finance teams need to track CTC estimates over time — not just the current snapshot — and challenge estimates that shrink without corresponding work completed.

Those unsupported reductions tend to cluster in the 60–85% completion range. The job looks close to done, so the PM reduces the CTC to match — but the margin that appeared on paper never materializes because the remaining scope was understated.

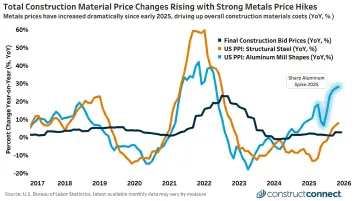

Material price volatility

Current market conditions have made material price risk sharper than it's been in years. Budgets set with prior-year unit prices can develop significant exposure before the first delivery hits the site.

AGC's September 2025 PPI release puts the scale in perspective:

- Aluminum mill shapes up 22.8% year-over-year

- Steel mill products up 13.1% over the same period

- 65% of firms experienced project delays from supply-chain challenges (AGC 2023 workforce survey)

Those delays carry their own cost implications through extended general conditions and labor inefficiency — compounding the direct material hit.

Construction Budget Management Best Practices

Start early and use a WBS from day one

The estimating process should begin before mobilization, with the WBS structure defined first. Building the budget line by line against a WBS — rather than as a lump-sum with rough categories — produces a document that can actually be tracked and challenged as the project progresses.

That WBS is only as reliable as the cost data behind it. Historical actuals from comparable completed projects are the most trustworthy input for labor, material, and subcontractor unit costs — firms estimating from memory, without a structured database of job actuals, compound that gap at the bid stage and carry it through execution.

Joint PM-and-finance reviews, not parallel reporting

Effective budget management requires both finance and project managers to review the same numbers at the same cadence. Separate reporting streams — the PM's field tracker and the accounting system's cost report — create conflicting versions of the truth and give each side cover to avoid accountability.

Monthly joint reviews that bring three data streams into a single conversation create shared ownership over where the job is headed:

- Accounting actuals (what's been invoiced and posted)

- Committed costs (open POs, executed subcontracts)

- PM-entered CTC by cost category

Datateer's Job Costing and Cost-to-Complete dashboards and PM Scorecards are built for exactly this workflow, presenting actuals and PM estimates side by side so the review stays focused on the job rather than resolving which number is correct.

Communicate proactively with owners, lenders, and leadership

Owners, lenders, and internal leadership should hear about budget status before problems force the conversation. Regular updates — ideally through dashboards that non-financial stakeholders can actually read — keep everyone aligned and reduce the likelihood of disputes escalating. When a change order issue does arise, it's far easier to resolve with a current documentation trail already in place.

How Real-Time Financial Visibility Strengthens Budget Control

The 10–20 day lag that closes the intervention window

In firms still relying on manual WIP processes and spreadsheet-based reporting, budget data is typically two to three weeks old by the time it reaches leadership. At that point, a deteriorating job is often 70%+ complete. The window to adjust field operations, accelerate billing, renegotiate scope, or protect margin has closed.

The JBKnowledge ConTech survey found 62% of construction firms still used spreadsheets for estimating and 44% used spreadsheets as their primary data-transfer method. This is a control problem as much as an efficiency problem. Manual processes introduce version errors, broken formulas, and the weekly data-gathering cycle that consumes finance team hours without producing current numbers.

Double L Management described the shift after implementing Datateer: "The very first time we accessed our data through a Datateer analytics dashboard, that one click replaced two weeks worth of prior work." The real value is timing: decisions made with current data can still change outcomes. Decisions made with three-week-old data are largely post-mortems.

What modern financial infrastructure enables

Datateer syncs directly with construction ERPs — including Procore, Sage, Viewpoint Vista, Viewpoint Spectrum, Acumatica, Foundation, CMiC, Jonas, QuickBooks, and NetSuite — to deliver automated WIP reports, job cost dashboards, and margin tracking without manual extraction or reconstruction.

Specific capabilities directly relevant to budget control:

- Job Costing & Cost-to-Complete: Actual costs incurred, committed costs, pending change orders, and projected final cost at job, phase, and cost-code level — updated automatically, not rebuilt monthly

- Margin Protection: Monitors original estimated margin vs. current projected margin per job; flags negative variance drivers (labor overrun, material escalation, subcontractor cost increases) so intervention happens during the project, not after closeout

- Change Order Impact & Aging: Tracks the full change order lifecycle — pending, approved, denied, executed — with aging by days since submission and revenue/margin impact tied to specific cost codes

- WIP Reporting: Automates percentage-complete, earned revenue, over/under-billings calculations — replacing the VLOOKUP marathon with a real-time schedule pulled directly from the ERP

What strong reporting signals to lenders and sureties

Contractors who can produce current, accurate WIP schedules with supportable CTC estimates and consistent gain/fade patterns present a materially lower risk profile. Sureties evaluate financial condition directly — inconsistent or perpetually restated WIP schedules are a red flag that disciplined financial controls aren't in place.

Finance teams using real-time data change the conversation with bonding agents, lenders, and ownership. The topic shifts from reconciling last month's numbers to managing this month's margin — a materially different position for everyone at the table.

Frequently Asked Questions

How do you budget as a contractor?

Define scope via a Work Breakdown Structure, then estimate all direct costs (labor with burden, materials, subcontractors, equipment) and indirect costs (PM time, permits, insurance, overhead). Add a contingency reserve of 5–20%, establish a formal change order process, and track actuals against budget throughout the job.

What are common budgeting allocation guidelines for contractors?

Personal finance rules like 50/30/20 don't translate to construction. Contractors typically target labor, overhead, and profit at defined percentages of revenue, but the right ratios depend on project type, delivery method, firm size, and market conditions. Establish those targets before bidding and track actuals job by job, not company-wide.

What are the 3 P's of budgeting for contractors?

Planning (build the budget before mobilization with accurate scope and cost estimates), Performance (track actuals against the budget throughout execution), and Projections (update the cost-to-complete estimate regularly so the finish-line margin is never a surprise). Gaps in any one of these will undermine the other two and erode margin before you see it coming.

What is a good contingency percentage for a construction budget?

Contingency typically ranges from 5% to 20% of total project cost. Well-defined, familiar-scope projects sit at the lower end; high-risk, fast-track, or design-build projects warrant reserves at the upper end or above. The percentage should reflect actual project risk, not a company-wide default.

What causes construction projects to go over budget?

The most common causes: inaccurate initial estimates, unmanaged scope creep, verbally approved but unprocessed change orders, indirect costs defaulting to G&A instead of specific jobs, and cost-to-complete estimates that stay optimistic past the project midpoint. These failure modes rarely appear in isolation.

How often should a construction budget be reviewed?

At minimum, monthly — with bi-weekly reviews recommended on larger or higher-risk jobs. Reviews must include updated cost-to-complete estimates from the project manager, not just accounting actuals. A budget review using only posted costs tells you where the job has been, not where it's going.