Introduction

A contractor can win the bid, hit every margin target on paper, and still miss payroll. Not because the project failed—because the cash never arrived when the costs did.

This is the working capital problem that's unique to construction. Revenue is earned continuously, but cash arrives in fits and starts — months after the work is done, minus whatever retainage the owner is holding. Meanwhile, labor, materials, and subcontractors don't wait.

According to CFMA's 2025 Construction Financial Benchmarker—covering fiscal 2024 data from 1,558 companies—the all-company current ratio sits at 1.7, with DSO averaging 55.2 days. That's not a cushion. That's a tightrope.

Here's what this guide covers:

- How working capital is defined and measured in construction

- Why the cash gap hits harder here than in other industries

- The four drains that trap the most capital

- The metrics that signal trouble early

- The strategies CFOs use to stay ahead of the crunch

Key Takeaways

- Working capital measures current assets minus current liabilities — in construction, that number moves project by project and month by month, rarely reflecting a stable baseline

- Retainage, billing delays, unapproved change orders, and subcontractor timing are the four biggest working capital constraints

- Track DSO, retainage outstanding, billing-to-collection lag, and underbilling balances—not just your bank balance

- Billing discipline and proactive retainage collection free up more capital than increasing your credit line

- Live ERP-connected dashboards replace stale month-end snapshots with daily working capital signals your team can act on

What Is Working Capital Management in Construction?

Working capital is current assets minus current liabilities. In practice: cash, receivables, and contract assets on one side; payables, accrued costs, and short-term debt on the other.

NASBP's working capital analysis defines current assets for contractors to include underbillings alongside cash, A/R, and inventories—and current liabilities to include overbillings alongside payables and accrued expenses. Construction working capital, in other words, is a function of your billing position, not just your bank balance.

Why Construction Is Different

In most product-based businesses, working capital stays relatively stable month to month. In construction, it fluctuates constantly because:

- Every project has its own billing schedule, retainage terms, and collection timeline

- Multiple projects run simultaneously, each in a different stage of the cash cycle

- The finance team must manage liquidity at the job level, not just company-wide

Managing working capital in construction means balancing inflows and outflows across a portfolio of projects — each with its own owner, contract terms, and completion horizon. A company-level cash balance tells you almost nothing about whether the next payroll is covered.

What "Healthy" Looks Like

CFMA's 2025 benchmarker reports an all-company current ratio of 1.7 for construction. Compare that to NYU Stern's cross-sector data, which shows engineering and construction non-cash working capital at 19.38% of sales versus 9.30% for the total market—roughly twice the capital intensity of the broader market.

Sureties use their own lens: NASBP notes they typically want to see roughly 10% of the requested bonding program in working capital, evaluated alongside WIP, liquidity, and bank credit.

The Construction Cash Gap: Why Working Capital Is Uniquely Challenging

Most businesses collect payment before or shortly after delivering something. Construction collects last — after mobilizing, spending, and waiting.

A contractor mobilizes, hires crews, orders materials, and pays subcontractors—all before submitting a payment application. Then the owner reviews it. Requests information. Requires lien waivers. Processes through their own accounting. The contractor waits another 30–60 days before cash arrives. Meanwhile, costs haven't paused.

The Multi-Project Compounding Effect

Run three projects simultaneously, each in mid-cycle, and each one has its own cash gap. The total capital required to fund operations can exceed what a cash balance snapshot shows. A company that appears adequately funded at the firm level can be cash-starved at the project level.

Retainage: The Built-In Delay

Retainage compounds the problem. Typically 5–10% is withheld from each progress payment until project completion — which, as CFMA notes, can take months or years. Every dollar of retainage is earned revenue that's been locked away, unavailable to fund the next project's startup costs or cover a payroll gap.

The more active long-duration projects you carry, the more capital is frozen in retainage at any given time. It's not a receivable you can accelerate. It waits on the project timeline.

Why Generic Financial Advice Doesn't Apply

A manufacturing company collects payment within net-30 terms on goods already produced. A services firm often invoices monthly against delivered work. Neither faces the combination of:

- Extended cost periods before first billing

- Owner review and approval cycles outside their control

- Mandatory retainage holdbacks

- Subcontractor payment obligations that arrive before owner payments do

Generic advice to "improve cash flow" misses the point. The gap between spending and collecting isn't a process failure — it's a structural feature of how construction contracts work. Managing working capital in construction means managing that gap deliberately, not assuming it will shrink on its own.

The Four Biggest Working Capital Drains in Construction

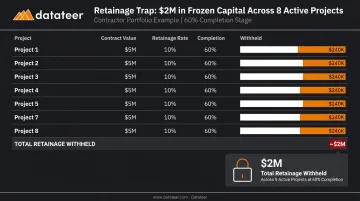

Retainage: Trapped Earned Revenue

Retainage is often the single largest working capital drain that doesn't show up as a problem until it's compounded.

Consider a contractor with eight active projects averaging $5M in contract value, each carrying 10% retainage. If each project is 60% complete, roughly $240,000 per project in earned revenue has been billed and withheld. Across the portfolio, that's nearly $2 million in earned revenue sitting in retainage—rivaling or exceeding the available credit line.

Contractors who don't track retainage systematically by project often discover this number only when they're already borrowing to cover costs.

FASB's guidance (Topic 910) requires contractors to disclose billed-but-unpaid retainage and amounts expected after one year. Compliance is different from proactive management.

Billing Cycle Delays: The Avoidable Drain

Every day a payment application is submitted late is a day added to the collection timeline. Every correction request resets that clock.

FMI recommends that project teams reach out to subcontractors by the 20th of the month so accurate billing is ready, and follow up when invoices are two or three days late. CFMA's cash management guidance similarly emphasizes insisting on timely, accurate invoicing and implementing collection standards.

This is a direct capital management lever. A contractor that submits applications consistently on day one of the allowable window collects weeks faster over a full year. Billing discipline compounds — teams that treat submission timing as a priority outpace those who don't across every project in the portfolio.

Unbilled and Pending Change Orders: The Invisible Float

Work performed under unapproved or unbilled change orders represents capital already deployed with no collection date in sight.

Research cited by Clearstory from Dodge Construction Network, covering nearly 200 contractors, found:

- 48% of GCs report increased change-order frequency

- 42% of specialty contractors report cash-flow problems from untimely change-order processing

- 83% still track change-order exposure in spreadsheets

Every month a change order sits unbilled, the contractor is providing interest-free financing to the owner while drawing on their credit line to cover the associated costs. The exposure is a working capital problem, not just a project management one.

Subcontractor Payment Timing: The Squeeze in the Middle

GCs sit between the owner's payment cycle and their subs' payment expectations. When owner payments run 45–60 days out, but subcontractors expect payment within 30, the GC absorbs the difference.

Two contract mechanisms govern this tension:

- Pay-when-paid: Ties the timing of sub payment to owner receipt, but doesn't eliminate the obligation

- Pay-if-paid: Makes owner payment a condition precedent to the GC's obligation to pay—but these clauses are void or unenforceable in several states including California, New York, North Carolina, South Carolina, and Wisconsin

The practical reality: subcontractor relationships and pricing depend on predictable payment. GCs who manage this timing proactively—rather than defaulting to whatever terms are in the contract—protect both their capital position and their access to the subs they need.

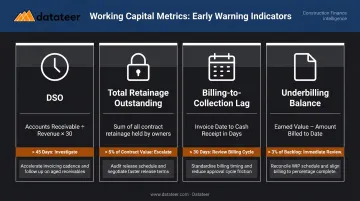

Key Working Capital Metrics Every Construction Finance Team Should Track

Tracking working capital in construction requires looking beyond the bank balance. Here are the four metrics that matter most:

| Metric | How It's Calculated | Warning Threshold | Action to Take |

|---|---|---|---|

| Days Sales Outstanding (DSO) | A/R ÷ Credit Sales × Days in Period | Above 60 days (CFMA benchmark: 55.2) | Audit billing cycle; tighten collections process |

| Total Retainage Outstanding | Sum of billed but withheld retainage by project | Growing relative to revenue without matching completions | Identify projects approaching substantial completion; initiate release process |

| Billing-to-Collection Lag | Average days from application submission to cash received | Trending upward quarter over quarter | Review owner payment practices; escalate slow payers |

| Underbilling Balance (WIP) | Costs in excess of billings, per project | Significant balance on multiple active projects | Prioritize billing catch-up; review billing procedures with PMs |

The WIP Schedule as a Working Capital Tool

The WIP schedule does something a balance sheet can't: it shows whether you're funding work you haven't billed yet, or drawing on future revenue you've already collected.

An underbilling position means the company has spent more than it has billed — it's effectively financing the gap out of its own pocket. Overbilling, by contrast, temporarily boosts liquidity but represents future work still owed to the owner.

CFMA benchmarks show underbillings to equity at 8.1% across the industry. Behind that figure is real cash already out the door: costs incurred and labor deployed, with no corresponding payment yet received.

The problem with most WIP reporting: it's produced once a month, after a close process that can take two or more weeks. By the time the underbilling position is visible, the cash has already been spent.

Strategies to Improve Working Capital Management in Construction

Billing Discipline as Foundational Strategy

Submit payment applications on the earliest contractually allowed date, every cycle, complete and correct. No exceptions.

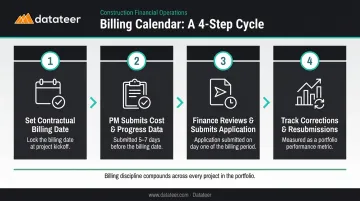

A systematic billing calendar looks like this:

- Set the contractual billing date for each active project at project kickoff

- Assign PM accountability for providing cost and progress data by a fixed internal deadline (typically 5–7 days before the billing date)

- Finance reviews and submits the application on day one of the window

- Track corrections and resubmissions as a performance metric

The CFO's role is to make the system non-negotiable and hold each project accountable to it.

Retainage Collection as a Dedicated Process

Retainage should be managed with the same rigor as active receivables. For each project:

- Track the contractual retainage release trigger (substantial completion, final acceptance, specific milestones)

- Identify required documentation 60–90 days in advance

- Assign ownership of the release process to a specific person

- Treat uncollected retainage on complete or substantially complete projects as an overdue receivable

NASBP's contractor guidance notes that not closing completed projects formally is one of the most common ways retainage gets held past its release date. On a substantially complete project, the money is already earned — the only remaining task is executing the paperwork to release it.

Project Mix Management as a Strategic Lever

Before signing a large lump-sum contract, a CFO should ask: what does this do to our working capital position for the next 18 months?

Considerations when evaluating new work:

- What are the billing cycle terms and retainage percentage?

- How long before the project generates net positive cash flow?

- What is the estimated peak underbilling exposure during construction?

- Does adding this project alongside current backlog create a capital crunch at mid-cycle?

Balancing the portfolio with shorter-duration projects or time-and-materials work can smooth the cash cycle while the company carries larger long-duration contracts.

Line of Credit: Timing Tool, Not a Crutch

A credit line used to bridge the timing gap between paying costs and collecting revenue is appropriate. CFMA advises negotiating an adequate working-capital line before each bid season, sized to projected usage rather than collateral value alone.

A line of credit that stays consistently maxed out signals something different:

- Debt funding day-to-day operations instead of bridging timing gaps

- Poor collections absorbing cash that should be self-sustaining

- Growth outpacing the firm's internal financing capacity

That pattern requires a collections and billing fix, not a larger credit line.

How Real-Time Dashboards Eliminate the Working Capital Blind Spot

The biggest enemy of working capital management isn't retainage or slow owners. It's data lag.

When AR aging reports, WIP positions, and retainage balances are only available after a 10–20 day close process, finance teams are always looking backward. They're doing forensic accounting—figuring out what happened—rather than intervening while there's still time to act.

FMI's research on engineering and construction firms found that only 8% have real-time, full project management information systems supporting dashboard reporting. Meanwhile, 49% manually transfer data between applications and teams spend roughly 13% of their work hours searching for project data.

The gap isn't a technology problem—it's a management visibility problem that compounds with every day of delay.

What Changes With Real-Time Data

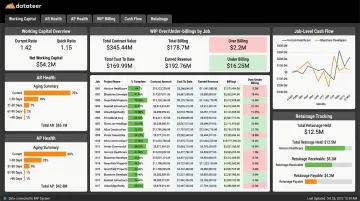

Datateer connects directly to 20+ construction ERPs—Procore, Sage, Viewpoint Vista, Acumatica, Foundation, CMiC, Jonas, and others—to deliver working capital dashboards that update overnight from live ERP data. The Cash Operations Dashboard suite includes:

- AR & AP Health: Receivables aging and payables status pulled directly from the ERP—not estimated from a spreadsheet export

- WIP & Over/Under-Billings: Underbilling and overbilling positions by job, calculated automatically—no manual month-end WIP marathon

- Job-Level Cash Flow: Flags which projects are generating cash versus consuming it, with 13-week forecasting built from actual burn rates and retainage schedules

- Retainage Tracking: A/R and A/P retainage by project and owner, with alerts for overdue releases that are holding up working capital

Double L Management's team reported that "the very first time we accessed our data through a Datateer analytics dashboard, that one click replaced two weeks worth of prior work."

From Reactive to Strategic

The shift isn't just speed—it's the nature of the work. When a CFO spends two weeks assembling a WIP report, there's no time left to act on what it reveals. When that same report refreshes automatically and surfaces an underbilled project at mid-month, there's time to accelerate billing, flag the project manager, and recover the cash position before month-end.

Finance teams that get there first—before month-end, before the damage compounds—are the ones protecting margins and keeping projects cash-positive.

Frequently Asked Questions

What is a common tool used for working capital management in construction?

The most common tools are construction ERP systems for job-level AR/AP tracking, WIP schedules for identifying underbilling and overbilling positions, and real-time dashboards that monitor working capital metrics continuously. Platforms like Datateer pull live data from ERPs like Procore, Sage, and Vista into pre-built working capital dashboards automatically.

What is a good working capital ratio for a construction company?

CFMA's 2025 Financial Benchmarker reports an all-company current ratio of 1.7 for FY 2024 construction firms. The right target varies based on project size, retainage volume, and billing cycle length—a company with heavy retainage exposure or longer billing cycles needs a higher buffer than the benchmark suggests.

How does retainage affect working capital in construction?

Retainage locks earned revenue in a receivable that can't be collected until project completion—sometimes months or years away. The more long-duration projects a contractor carries simultaneously, the more capital is frozen in retainage, sometimes rivaling the available credit line.

What is the difference between working capital and cash flow in construction?

Working capital is a balance sheet measure—current assets minus current liabilities—reflecting your short-term financial position at a point in time. Cash flow tracks money moving in and out over a period. They answer different questions: working capital shows whether you're solvent; cash flow shows whether you're liquid.

How does the WIP schedule relate to working capital management?

The WIP schedule reveals whether a contractor is underbilled (funded more work than billed, consuming working capital) or overbilled (billed ahead of costs, temporarily boosting liquidity). It's essential for understanding true working capital position beyond the balance sheet—stale WIP data makes it impossible to act before the problem compounds.

How can a construction company improve working capital without increasing its line of credit?

The highest-leverage actions: tighten billing discipline (submit applications on the earliest allowed date without exception), pursue retainage release proactively on projects approaching completion, eliminate change order billing delays, and align subcontractor payment terms with the collection cycle. These free trapped capital without adding debt.