Introduction

Many construction CFOs face a familiar scenario: the auditor arrives, and the next six weeks become a scramble to locate signed change orders, reconcile WIP schedules to the general ledger, and explain cost allocations that made sense at the time but weren't documented.

That scramble is expensive. It strains auditor relationships, delays opinions, and — when findings are qualified — directly damages bonding capacity and lender trust.

The antidote is straightforward: audit-ready financial reports are GAAP-compliant statements supported by organized, cross-referenced documentation that allows an external auditor to verify every number without requiring management to reconstruct data from scratch.

This guide covers what audit-ready reports look like in construction, why they matter for surety and lending relationships, how to build them through consistent monthly habits, and the most costly mistakes to avoid.

Key Takeaways

- Audit readiness is built year-round through monthly WIP reviews, reconciled job costs, and current documentation — not year-end cleanup

- Construction audits center on WIP schedules, ASC 606 percentage-of-completion, and job costing accuracy

- Disorganized records, undocumented change orders, and misallocated overhead are the primary reasons audits run over time and over budget

- GAAP compliance (accrual accounting, ASC 606, ASC 842) is required before surety and lender thresholds — start early

- Direct ERP-integrated reporting tools cut the manual data assembly that stalls audit prep

What Are Audit-Ready Financial Reports for Contractors?

Audit-ready financial reports are a complete, organized set of GAAP-compliant financial statements: income statement, balance sheet, and cash flow statement. They're supported by job-level documentation that lets an auditor trace every figure back to source transactions.

What Makes Construction Different

In most industries, revenue recognition is straightforward. In construction, it isn't. Revenue is recognized over time using the percentage-of-completion method under ASC 606, not when cash changes hands. That means the financials must reflect the real-time status of every active project through accurate WIP schedules, job cost reports, and billing reconciliations.

Per AICPA guidance, the cost-to-cost method — comparing costs incurred to total estimated costs — determines percentage complete and drives both revenue recognition and WIP calculations. If job costs are inaccurate, reported revenue is inaccurate — and that error flows directly into the financial statements your auditor will scrutinize.

Audit-Ready vs. "Closing the Books"

Closing the books means the numbers balance. Audit-ready means the supporting documentation is organized and cross-referenced before the auditor arrives. The difference comes down to what's on file:

- Closing the books: General ledger reconciles, period is locked, financials balance

- Audit-ready: Contracts, change orders, cost codes, and payroll records are mapped to every line item and retrievable on request

The difference shows up in audit duration. Contractors who maintain running audit files move through fieldwork in weeks; those who assemble documentation reactively extend audits by months and generate avoidable findings.

Why Construction Contractors Need Audit-Ready Financial Reports

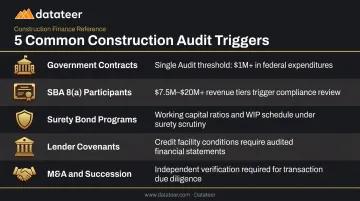

What Triggers a Formal Audit

Several events typically require a construction company to undergo a formal financial audit:

- Government contracts — federal award recipients spending $1 million or more annually must undergo a Single Audit under 2 CFR Part 200 Subpart F

- SBA 8(a) participants with gross annual receipts over $20M must submit audited statements; those between $7.5M and $20M submit reviewed statements

- Surety bond programs — while no universal dollar trigger exists, Windham Brannon notes that reviewed or audited statements carry significantly more weight with sureties, who scrutinize working capital, debt-to-equity, and WIP schedules

- Lender covenants — loan agreements often require audited statements as a condition of credit

- M&A and succession events — buyers and investors require independent verification of financial position

Old Republic Surety estimates a construction audit takes 6–9 weeks to complete. Waiting until a bond or credit event forces the issue leaves no runway to address deficiencies.

The Cost of a Qualified Opinion

A qualified audit opinion signals to lenders and sureties that GAAP reporting standards weren't fully followed. The downstream effects are concrete:

- Reduced bonding capacity — sureties view qualification as evidence of weak financial controls

- Higher borrowing costs — clean audited statements can reduce interest rates by more than 0.5%, according to Doeren Mayhew

- Lost contract bids — government and large GC contracts often require unqualified opinions as a condition of award

Audit Readiness as Competitive Advantage

Contractors who consistently produce clean audits access larger bonds, better credit terms, and more contract opportunities than those who scramble annually. EisnerAmper notes that bonding companies view the WIP schedule as the "holy grail" of contractor financial statements — it's the first thing a surety reviews when evaluating bonding capacity.

That makes accurate, timely WIP reporting one of the highest-leverage things a contractor can do to strengthen their financial position — and it starts with having clean, consistently structured data before the auditor walks in the door.

How to Build Audit-Ready Financial Reports: A Step-by-Step Guide

Audit readiness comes from consistent monthly habits across four areas: accounting systems, job-level documentation, financial reporting, and internal controls.

Step 1: Transition to GAAP-Compliant Accrual Accounting

Cash-basis accounting records revenue when received and expenses when paid. That approach distorts profitability on long-term contracts and tells lenders and sureties very little about a contractor's actual financial position.

GAAP accrual accounting requires:

- Recognizing revenue as work progresses under ASC 606 (cost-to-cost percentage-of-completion)

- Recording expenses when incurred, not when paid

- Reporting operating and finance leases on the balance sheet under ASC 842 (effective for private companies for fiscal years beginning after December 15, 2021)

- Classifying over-billings and under-billings correctly on the balance sheet

Auditors verify consistent application of these methods and look for disclosed accounting policies for revenue recognition and capitalization thresholds. Inconsistent application is one of the most common triggers for audit adjustments.

Step 2: Establish Rigorous Job Costing Processes

Accurate job costing is a prerequisite for reliable GAAP revenue recognition. If costs are misallocated, the percentage-of-completion calculation is wrong, and reported revenue is misstated.

A strong job costing system requires:

- Standardized cost codes applied consistently across all projects

- Clear allocation rules for indirect costs — labor burden, insurance, fuel, equipment

- Real-time field updates so costs are captured when incurred, not weeks later

- Monthly reconciliation of actual costs against budget at the cost-code level

Boyum Barenscheer identifies misallocated overhead costs in job costing as one of the five most common construction audit issues. Consistent process applied before auditors arrive is the only reliable fix.

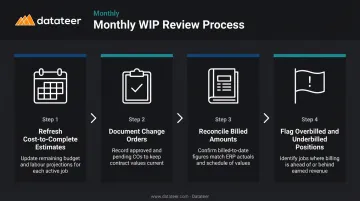

Step 3: Implement Monthly WIP Reporting

Because job costing accuracy feeds directly into WIP calculations, the two disciplines are inseparable. The WIP schedule — which reconciles contract value, costs incurred, billings to date, and estimated costs to complete for every active project — is the most scrutinized document in a construction audit. Any inconsistency signals revenue manipulation or weak controls.

A monthly WIP review process looks like this:

- Refresh cost-to-complete estimates before month-end close — project manager inputs must reflect current field conditions

- Document change orders as they are approved, not retroactively

- Reconcile billed amounts against the general ledger

- Flag overbilled and underbilled positions early so adjustments can be made while projects are still active

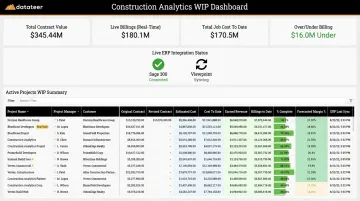

The challenge most contractors face is timing. Traditional WIP reports involve CSV exports, VLOOKUP reconciliation between Procore and Sage, and a 10–20 day lag before the schedule is usable. By the time it's ready, the data is already stale.

Datateer's WIP dashboard eliminates that lag. The platform syncs directly with 12 major construction ERPs — including Procore, Sage, Viewpoint Vista, Acumatica Construction, CMiC, Foundation Software, and Jonas Construction — and refreshes WIP data in under two minutes. Double L Management's business analyst put it plainly: "That one click replaced two weeks' worth of prior work." That kind of real-time visibility means WIP can be reviewed, adjusted, and handed to auditors without a last-minute scramble.

Step 4: Organize Documentation and Prepare Supporting Schedules

Auditors work from a standard request list. Having these organized before fieldwork begins is the difference between a 6-week audit and a 10-week audit.

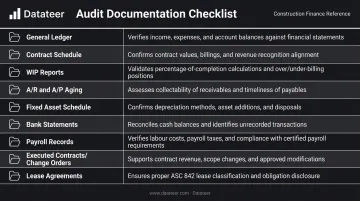

Core documentation auditors request:

| Document | Purpose |

|---|---|

| General ledger (full audit period) | Foundation for all testing |

| Contract schedule reconciled to trial balance | Verifies revenue completeness |

| WIP reports | Revenue recognition support |

| A/R and A/P aging schedules | Receivables and payables verification |

| Fixed asset and depreciation schedules | Balance sheet verification |

| Bank statements | Cash reconciliation |

| Payroll records | Labor cost verification |

| Executed contracts and approved change orders | Revenue authorization |

| Lease agreements (ASC 842) | Balance sheet completeness |

Records prepared at the time of transaction are more defensible than reconstructions — auditors can tell the difference. Maintaining a running audit file throughout the year means fieldwork starts from a position of strength, not a last-minute document pull.

Key Construction-Specific Factors That Affect Audit Readiness

Job Costing Complexity

Unlike most industries, construction revenue depends on cost-to-complete estimates that require judgment. Auditors test the reasonableness of those estimates directly with project managers. Finance and operations must be aligned — if a PM's cost-to-complete assumptions don't match the accounting records, auditors will ask why.

Change Order Management

Undocumented or unsigned change orders are a top audit risk. They inflate contract values without supporting authorization, create overbilling positions, and raise questions about revenue reliability. EisnerAmper notes that construction companies entering long-term contracts need careful change order tracking under ASC 606. The fix is a documented workflow requiring approval before work proceeds, not after the invoice is submitted.

Chart of Accounts Structure

A poorly structured chart of accounts forces auditors to manually untangle GAAP adjustments from operational metrics. A clean, purpose-built chart that separates over/under billings, capitalized interest, and retainage from internal job tracking codes reduces audit fieldwork time measurably.

Technology and ERP Integration

Manual spreadsheet reporting introduces transcription errors, formula breaks, and version control problems that auditors flag as internal control weaknesses. Construction firms using automated reporting with direct ERP data feeds eliminate these risks.

Datateer's construction analytics platform integrates with 12+ construction ERPs and project management systems, including:

- Procore, Sage, Viewpoint Vista and Spectrum

- Acumatica Construction, CMiC, and Foundation Software

It maintains a single, auditable data source across WIP, job costing, ASC 606 revenue recognition, and change order tracking. Automated data extraction standardizes cost codes across systems and reconciles Procore project commits to Sage invoices automatically, eliminating the manual reconciliation that typically generates internal control findings.

Internal Controls and Segregation of Duties

Smaller construction firms often have one person handling AP, AR, and payroll. That concentration is a red flag for auditors. Document compensating controls — owner review of bank statements, independent payroll verification — and plan to strengthen segregation as your firm grows.

Common Audit Preparation Mistakes Contractors Make

Treating Audit Prep as a Year-End Activity

This is the most expensive mistake in construction finance. Year-end scrambling leads to retroactive data reconstruction, discovered errors that trigger adjustments, and extended fieldwork that strains both the team and the auditor relationship. Monthly WIP reviews and running documentation files prevent all three problems before fieldwork starts.

Documentation Gaps That Generate Findings

Several specific mistakes consistently derail construction audits:

- Omitting revised cost-to-complete estimates from the WIP schedule — estimates that don't reflect current field conditions produce revenue restatements

- Failing to reconcile the contract schedule to the trial balance before fieldwork begins — discrepancies become audit findings that an internal review would have caught

- Missing approved change orders in the WIP schedule — KatzAbosch notes that approved contract changes as of the balance sheet date must be reflected in WIP

Confusing a Clean Close with Audit Readiness

A contractor can have correct totals and still face a difficult audit. Auditors require supporting evidence for every material balance — not just accurate numbers. A revenue figure unsupported by a signed contract or approved change order triggers follow-up requests that can extend fieldwork by two to three weeks.

The distinction: a clean close means the books balance. Audit readiness means every material balance has documentation behind it.

Frequently Asked Questions

What are the 5 C's of audit findings?

The five audit finding attributes are: Criteria (the standard expected), Condition (what was found), Cause (why the gap exists), Consequence (the impact), and Corrective Action (what will be done to fix it). Knowing each attribute helps contractors respond precisely and avoid repeat findings in subsequent audits.

What are the 4 types of financial audits?

The four main types are: external audits (CPA firm examination of financial statements), internal audits (company-conducted assessment of controls and processes), government/regulatory audits (required for federal contracts or funding), and forensic audits (investigative, typically triggered by suspected fraud or litigation).

When does a construction contractor typically need a financial audit?

Common triggers include federal award expenditures over $1M (Single Audit requirement), SBA 8(a) program participation above certain revenue thresholds, surety programs requiring audited statements, and M&A or ownership transitions. Preparation should start well before any of these thresholds are reached.

What is a WIP schedule and why do auditors focus on it so heavily?

A WIP schedule reconciles each active project's contract value, costs incurred, billings to date, and estimated costs to complete. Auditors scrutinize it because revenue recognition under GAAP flows directly through it — errors in cost estimates or billing records misstate reported revenue across the entire portfolio.

What is the difference between cash-basis and GAAP accounting for contractors?

Cash-basis records revenue when payment is received and expenses when paid — simple, but distorting for long-term contracts. GAAP accrual accounting under ASC 606 recognizes revenue as work progresses using percentage-of-completion, giving lenders, sureties, and auditors an accurate view of actual financial performance at any point in time.

How long does a construction audit typically take, and what slows it down?

Construction audits typically run 6–9 weeks, but stretch longer when WIP schedules aren't reconciled to the general ledger, documentation is scattered, or auditors wait on management to locate records. Maintaining current WIP schedules, running documentation files, and reconciled job costs year-round is what keeps that timeline in check.