Overhead allocation is the process of distributing indirect costs across construction projects so every job carries its fair share of the expenses required to run the business. Without it, job costing is incomplete and financial statements mislead more than they inform.

This guide covers:

- What construction overhead is and how to distinguish indirect costs from G&A

- Why allocation accuracy directly affects bidding, bonding, and profitability

- The main allocation methods and how to choose between them

- A five-step process for applying overhead to jobs

- Common mistakes and how technology closes the gap

Key Takeaways

- Overhead allocation distributes indirect costs — equipment, insurance, admin salaries — so every project reflects its true cost

- Construction firms use several methods (direct labor hours, direct costs, revenue-based, ABC); the best choice depends on cost structure and project mix

- A predetermined overhead rate lets firms apply estimated overhead to jobs in real time, before the period-end close

- Misallocating overhead distorts job costing, drives underbidding, and masks margin fade until it's too late

- Technology that syncs ERP data overnight lets finance teams monitor allocated vs. actual overhead across every active job, in real time

What Is Overhead in Construction?

Overhead is any cost that can't be traced directly to a single project but is still essential for running the business. It's the counterpart to direct costs — materials purchased for a specific job, direct labor tied to that site, subcontractors under a project-specific contract.

Construction makes this especially complex. Firms run many jobs simultaneously, each consuming shared resources at different rates. A dozer working across three active sites shouldn't have its full operating cost charged to any one of them. That's where systematic allocation becomes necessary.

Indirect Costs

Indirect costs are tied to job activity but shared across multiple projects. They fluctuate with business volume — the more jobs running, the higher these costs tend to climb.

Common indirect cost categories in construction:

- Equipment depreciation, fuel, and maintenance

- Vehicles and fleet operating costs

- Labor burden (health benefits, workers' comp, payroll taxes) for field staff

- Indirect labor — project managers, superintendents, safety officers

- Insurance premiums (general liability, builder's risk, workers' comp)

- Job-site tools, supplies, and temporary facilities

General & Administrative (G&A) Costs

G&A costs support the overall operation of the business regardless of how many jobs are active. These would exist even with zero projects on the books.

Typical G&A expenses include:

- Office rent and utilities

- Administrative and executive salaries

- Legal, accounting, and audit fees

- Software subscriptions and licenses

- Marketing and business development

The practical distinction matters for allocation: indirect costs vary with job volume and connect more logically to project consumption, while G&A is relatively fixed regardless of how busy the firm is. Both types can be allocated across jobs, but the rationale and method often differ — and that difference directly affects bid accuracy and reported job margins. A construction CPA can help determine which costs belong in each bucket and which allocation method best reflects actual consumption.

Why Overhead Allocation Matters for Construction Firms

The Job Costing Problem

If overhead is excluded or underallocated, a job that looks profitable on a direct-cost basis may be a money-loser once indirect expenses are factored in. That false picture compounds over time — especially when it feeds future estimates.

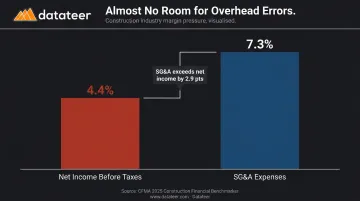

According to CFMA's 2025 Construction Financial Benchmarker, net income before taxes for Industrial and Nonresidential contractors averaged just 4.4% of revenue, with SG&A expenses consuming 7.3% of revenue. There's almost no margin for error in overhead recovery. Firms that consistently underallocate overhead end up subsidizing unprofitable work — and their own job reports tell them everything is fine.

The Bidding Consequence

Firms that don't properly fold overhead into bid pricing win jobs at margins too thin to survive. The SFAA identifies bids that are priced too low as a direct sign of poor estimating and job cost reporting — and a documented early warning sign of contractor financial distress.

Historical overhead rates should flow directly into the estimating process. When they don't, bids are built on incomplete cost models.

Financial Reporting and Bonding Exposure

Underpriced bids are only the first casualty. Overhead misallocation also distorts the financial data that lenders, sureties, and auditors depend on:

- Skewed WIP schedules — over/underbillings become unreliable when job costs are wrong

- Inaccurate percentage-of-completion — revenue recognition on long-term contracts depends on accurate cost data

- Surety and lending risk — NASBP has documented cases where underbilling errors inflated a contractor's working capital by nearly $3M, creating serious misrepresentation with bonding companies

Surety underwriters, lenders, and investors rely on job cost data. Overhead allocation errors create exposure that goes far beyond day-to-day operations.

Common Overhead Allocation Methods in Construction

The right allocation method depends on what actually drives overhead consumption at your firm. A labor-intensive MEP subcontractor has a fundamentally different cost structure than a civil contractor running heavy equipment on large earthwork contracts — and the method that fits one will distort results for the other.

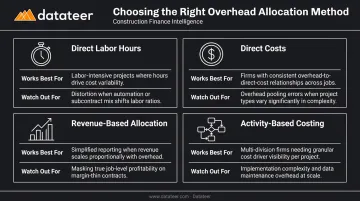

Direct Labor Hours

Overhead is distributed based on labor hours charged to each job. If Job A logged 1,500 hours out of 3,500 total company hours, it absorbs 43% of the overhead pool.

Works best for: Labor-intensive firms where field activity closely tracks overhead consumption. Watch out for: Equipment-heavy projects, where high machine hours may drive more overhead than labor hours suggest.

Direct Costs

Overhead is allocated in proportion to each job's total direct costs (materials + labor + subcontractors). A larger, more resource-intensive project absorbs proportionally more overhead.

Works well for firms with relatively consistent project types, though a materials-heavy job can absorb significant overhead even when the actual management intensity is low.

Revenue-Based Allocation

Overhead is distributed proportionally based on each project's revenue contribution. This aligns overhead recovery with financial performance and works well when project size and complexity track with revenue. Works best for firms where larger contracts genuinely demand more G&A support, but can skew results if a high-revenue job runs lean on internal resources.

Predetermined Overhead Rate

Rather than waiting for period-end actuals, firms estimate total annual overhead and divide by the estimated total of the chosen allocation base.

Formula: Overhead Rate = Estimated Total Overhead ÷ Estimated Total Allocation Base

Example: $300,000 estimated overhead ÷ 10,000 estimated direct labor hours = $30 per direct labor hour

As each job logs hours, the rate is applied immediately — giving project managers and finance teams current cost visibility rather than a month-end surprise.

Activity-Based Costing (ABC)

ABC allocates overhead based on specific cost-driving activities — number of change orders, permit processing steps, equipment setups — rather than a single company-wide rate. It provides the most granular accuracy but requires more upfront setup. Best suited for firms with diverse project types and complex overhead structures where a blended rate would distort results significantly.

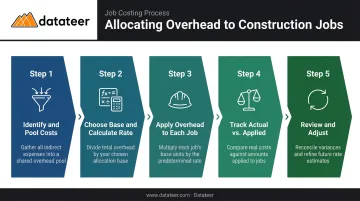

How to Allocate Overhead to a Construction Job: Step-by-Step

Step 1: Identify and Pool Overhead Costs

Group indirect and G&A costs into defined cost pools — for example:

- Equipment pool (depreciation, fuel, maintenance)

- Labor burden pool (benefits, workers' comp, payroll taxes)

- General overhead pool (office, admin salaries, insurance)

Separating pools matters because an equipment-intensive job should absorb more from the equipment pool than from the administrative pool. Blending everything into one pool obscures those differences.

Step 2: Choose an Allocation Base and Calculate the Rate

Select the base that best reflects cost consumption for each pool. Apply the formula:

Overhead Rate = Estimated Total Overhead ÷ Estimated Total Allocation Base

Worked example — two concurrent jobs:

| Job A (Residential) | Job B (Commercial) | |

|---|---|---|

| Direct Labor Hours | 1,200 | 2,800 |

| Total Direct Costs | $180,000 | $620,000 |

| Labor Burden Pool ($40,000 ÷ 4,000 hrs = $10/hr) | $12,000 | $28,000 |

| G&A Pool ($60,000 ÷ $800,000 direct costs = 7.5%) | $13,500 | $46,500 |

Job B is larger and absorbs more from both pools — but the proportions differ depending on which base you use, which is why pool separation matters.

Step 3: Apply Overhead to Each Job

Multiply the overhead rate by the actual allocation base activity recorded for that job. The journal entry:

- Debit: Work-in-Process (WIP) — the job's cost account increases

- Credit: Construction Overhead clearing account — the overhead pool decreases

This transfers overhead costs from the shared pool into the specific job's cost record.

Step 4: Track Actual Overhead and Compare to Applied

At period-end, compare what was actually incurred against what was applied to jobs.

- Underapplied overhead: Actual costs exceeded applied — jobs were undercharged. The firm absorbed less overhead than it actually spent.

- Overapplied overhead: Applied overhead exceeded actual costs — jobs were overcharged.

The variance is closed to Cost of Goods Sold if immaterial. If material, it should be allocated across WIP, Finished Goods, and COGS proportionally.

Step 5: Review and Adjust

Overhead rates should be reviewed at least quarterly. Several factors can shift your overhead drivers between reviews:

- Project mix changes (more equipment-heavy work vs. labor-heavy)

- Headcount fluctuations affecting labor burden pools

- Equipment fleet additions or disposals

- Significant swings in business volume

When any of these shift materially, recalculate your rates before they quietly inflate job costs or erode margin on new bids.

Common Overhead Allocation Mistakes to Avoid

Misclassifying Direct and Indirect Costs

Treating shared equipment depreciation as a direct cost — charging a dozer's full depreciation to whichever job it happens to be on this week — inflates that job's direct costs and understates overhead. Every other job then absorbs too little.

The reverse error cuts the other way: treating a direct cost as overhead inflates the overhead pool and causes systematic overburdening across all jobs.

Failing to Connect Allocation Back to Bids

Many firms develop their allocation method for financial reporting and never feed it into the estimating process. Bids get built on incomplete cost models. The fix: historical overhead rates should be a standing input in every bid template, reviewed before each project estimate is finalized.

Relying on Spreadsheets

JBKnowledge's Construction Technology Report found that 62% of construction firms relied on spreadsheets for estimating and 49% manually transferred data between non-integrated applications.

For overhead allocation, spreadsheet dependence creates compounding problems:

- Formula errors that silently corrupt allocation rates

- Version control failures when multiple team members maintain separate files

- Data living outside the accounting system with no audit trail

- Reporting lag that leaves finance teams reacting to problems that embedded weeks earlier

Each of these mistakes shares a root cause: overhead allocation treated as a periodic cleanup task rather than a live, integrated process. The firms that get it right build allocation into their systems — not their to-do lists.

How Technology Transforms Overhead Allocation in Construction

The traditional overhead allocation workflow has a structural flaw: by the time month-end close produces reliable numbers, the decisions those numbers should have informed are already made. For large jobs, a 10–20 day reporting lag means margin fade can take hold well before anyone sees it.

Modern platforms change the dynamic. Datateer's Overhead, G&A & Burden Rate Analytics module — bundled into its flat-rate subscription — syncs directly with construction ERPs on an overnight cycle, pulling actual job cost data and surfacing overhead absorption per project without manual intervention. More frequent refresh is available when needed.

What to Look for in a Technology Solution

- Pulls data directly from source ERPs — no manual re-entry, no CSV exports. Datateer connects with 12 construction ERP systems including Sage 100/300/Intacct, Viewpoint Vista, Viewpoint Spectrum, Procore, Acumatica Construction, Foundation Software, CMiC, Jonas Construction, QuickBooks, and NetSuite

- Standardizes overhead categorization across projects through automated cost code mapping, even when underlying ERP structures differ

- Shows allocated vs. actual overhead side-by-side at the job level, with drill-down to the source transaction

- Tracks burden rate variance — budgeted vs. actual fully-burdened labor rates by craft, department, and division

Datateer's implementation runs 2–4 weeks, and the annual subscription (starting at $10,000/year per data source, unlimited users) begins only after data is flowing.

From Forensic Accounting to Strategic Visibility

When overhead data is current and reliable, construction CFOs stop reformatting spreadsheets and start identifying which project types produce the best overhead recovery, which crews consistently run over on labor burden, and where indirect costs are trending upward before they compress margins on otherwise profitable jobs. Accurate, automated overhead allocation is what makes that shift from reactive reporting to forward-looking decisions possible.

Frequently Asked Questions

How is overhead allocated to a job?

Overhead is allocated by first calculating a predetermined overhead rate (estimated total overhead ÷ estimated allocation base activity), then multiplying that rate by the actual allocation base recorded for each job as work progresses. The result is applied to the job's cost record throughout the period rather than waiting for period-end actuals.

When overhead is allocated to a job, which account increases?

When overhead is applied to a job, the Work-in-Process (WIP) account increases through a debit entry, while the Construction Overhead clearing account is credited — transferring indirect costs from the shared pool into that specific job's cost record.

What does allocated overhead mean?

Allocated overhead is the portion of indirect costs — equipment, insurance, admin salaries — assigned to a specific job using a predetermined rate and allocation base. It represents that job's fair share of business-wide expenses that can't be traced directly to a single project.

What is the difference between direct costs and overhead costs in construction?

Direct costs (materials, direct labor, subcontractors) are traceable to a single specific project. Overhead costs are indirect expenses shared across multiple jobs that must be distributed using a systematic allocation method rather than direct assignment.

What is a predetermined overhead rate and why is it used?

A predetermined overhead rate is calculated at the start of the period (estimated overhead ÷ estimated allocation base) and applied throughout the year so job costs can be tracked in real time — without waiting for period-end actuals. This enables current job cost visibility and timely bidding decisions.

What is underapplied vs. overapplied overhead in construction?

Underapplied overhead means actual costs exceeded what was applied — the firm undercharged jobs. Overapplied means applied overhead exceeded actual costs — the firm overcharged jobs. Immaterial variances are closed to Cost of Goods Sold at period-end; material amounts are prorated across WIP, finished goods, and COGS.