Key Takeaways

- The construction CCC measures the gap between cash going out (labor, materials, subs) and cash coming in (owner payments) — often 60–90+ days

- DSO is the dominant CCC driver in construction, with CFMA reporting 55.2 days in accounts receivable for fiscal year 2024

- Retainage, billing approval lags, and underbilling positions are the three key factors that extend the CCC beyond what billing terms alone would suggest

- Front-loading schedules of values, accelerating pay application submission, and negotiating retainage terms are the highest-leverage levers for shortening the CCC

- Real-time WIP visibility is what separates firms that manage cash proactively from those that react to crises

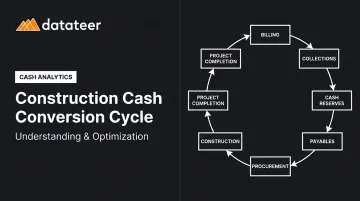

What Is the Cash Conversion Cycle in Construction?

The cash conversion cycle (CCC) measures the number of days between when cash leaves your business and when it returns via owner payments. For a construction firm, that means the time from cutting payroll and paying suppliers through to depositing the owner's check.

In theory, CCC uses three components:

- Days Inventory Outstanding (DIO) — days of materials and work-in-progress on hand before billing

- Days Sales Outstanding (DSO) — days from billing submission to cash receipt

- Days Payable Outstanding (DPO) — days from receiving a supplier or subcontractor invoice to paying it

Formula: CCC = DIO + DSO – DPO

While all three components matter, in construction DSO dominates. A retailer invoices and collects within days. A contractor submits a pay application, waits for owner and architect review, waits for the contractual payment window, and even after payment clears, has retainage withheld until closeout. Cash flows out continuously; it flows back in as delayed, partial installments.

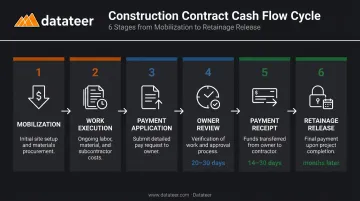

The Typical Cash Flow Sequence on a Construction Contract

- Mobilization — equipment, insurance, bonding costs hit the bank before a single bill goes out

- Ongoing spend — payroll runs every two weeks; material and sub invoices arrive daily

- Progress billing — submitted monthly (or per milestone), triggering the approval clock

- Owner/architect review — typically 20–30 days before approval

- Payment receipt — another 14–30 days post-approval

- Retainage release — held until substantial or final completion, often months later

This sequence means a contractor can be fully booked, billing on time, and still face a genuine cash crunch — not because the business is failing, but because the structure of construction payment cycles creates a persistent gap between work performed and cash received.

According to EisnerAmper, bonding capacity is often calculated at roughly 10 times working capital — meaning $5M in working capital can support $50M in additional bonding capacity. Every day shaved off the CCC is working capital freed up, translating directly into bid capacity and reduced dependence on lines of credit.

How to Calculate the Construction Cash Conversion Cycle

Calculating DSO in Construction

DSO measures the average days from billing submission to cash received:

DSO = (Accounts Receivable ÷ Revenue) × 365

One critical detail: construction AR typically contains two distinct buckets that should never be collapsed into one number:

- Billed-but-unpaid AR — invoiced amounts still within the payment window or past due

- Retainage AR — amounts earned but contractually withheld until project milestones

Combining them overstates collectible receivables and masks the true cash timing problem. A firm with $2M in AR might have $800K of that in retainage that won't arrive for 6–12 months, a very different liquidity picture than $2M of normal trade receivables.

Calculating DPO in Construction

DPO = (Accounts Payable ÷ Cost of Revenue) × 365

Pay-when-paid clauses complicate DPO calculations. When a general contractor can legally defer subcontractor payment until the owner pays, DPO inflates, which makes the CCC look better on paper. That's not improved liquidity; it's transferred risk. A CCC that appears short because of pay-when-paid deferral may be masking genuine collection problems upstream.

Watch for this: A shrinking CCC driven by pay-when-paid deferral is a warning sign, not a performance improvement.

The Net Cash Outlay Approach

For project-level cash management, the net cash outlay method is more actionable than a company-wide CCC average:

Net Cash Position = Cumulative Contract Cash Inflows – Cumulative Contract Cash Outflows

Consider a straightforward example: a contractor mobilizes on Day 1, covering immediate labor and material costs. The first pay application goes out at month-end. The owner takes 30 days to approve it, then the contract allows 20 days to pay.

The contractor is now at Day 80 before the first dollar arrives, while payroll has run four times. That 60–80 day gap is the real cash at risk — built directly into the contract terms.

Multiplied across a portfolio of 15–20 active projects at different stages, the aggregate net cash position becomes the firm's true working capital exposure. Datateer's Job-Level Cash Flow dashboard maps this exposure project by project, showing which jobs are generating cash and which are drawing it down — so finance teams can act before a liquidity gap becomes a cash crisis.

Construction-Specific Factors That Extend the CCC

Retainage

Retainage is the single biggest structural CCC extender. Owners typically withhold 5–10% of each progress payment until substantial or final completion. Under federal construction contracts, FAR 32.103 caps retainage at 10% of the approved estimated amount — and that ceiling reflects common private-contract practice as well.

On a $10M contract at 10% retainage, the contractor funds $1M of work without receiving a dollar for it until closeout. Depending on project duration, that cash could be tied up for 12–24 months.

Several states have enacted retainage reform laws. New York's 2023 legislation capped retainage at 5% on qualifying private projects, and California implemented a similar 5% cap for private contracts in 2026. The AGC maintains a Prompt Payment State-by-State Map to track current rules by jurisdiction.

Billing Approval Lags

Commercial and public contracts typically require owner or architect review of each pay application before payment releases. This approval period runs 20–30 days on top of the contractual payment window, entirely outside the contractor's control.

Federal contracts set a useful benchmark: FAR 52.232-27 requires payment within 14 days of receiving a proper request on federal construction work, a standard most private contracts don't meet.

The American Express/PYMNTS 2025 report found that by end of 2023, 71% of subcontractors reported delayed payments from general contractors, with the average payment cycle reaching 57 days for completed work.

Pay-When-Paid and Pay-If-Paid Clauses

These two clauses are legally distinct:

- Pay-when-paid — a timing mechanism; the GC must pay the sub within a reasonable time after receiving owner payment

- Pay-if-paid — a condition precedent; if the owner never pays, the sub absorbs that risk entirely

Both create cascading delays: a single disputed owner payment ripples through every subcontractor on the job. For CCC analysis, these clauses mean DPO doesn't always reflect genuine payment management. Sometimes it reflects contractual risk transfer with nothing to do with the firm's actual cash velocity.

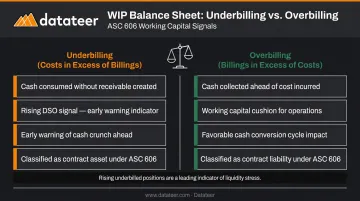

Underbilling and Overbilling (WIP Positions)

WIP schedule positions are direct CCC signals:

- Underbilling (costs in excess of billings) — the firm has spent money it hasn't billed yet; cash is actively being consumed without a corresponding receivable

- Overbilling (billings in excess of costs) — the firm has collected ahead of cost incurrence; a cash flow cushion exists

Under ASC 606, underbillings are contract assets on the balance sheet — economic value, but not yet cash. A portfolio with rising underbilled positions across multiple projects is burning working capital faster than billings are creating receivables. That imbalance registers in the CCC as rising DSO, often weeks before it surfaces as a cash problem.

What Does a Good Construction CCC Look Like?

There is no single target number. A lump-sum commercial contractor, a cost-plus industrial firm, and a specialty trade subcontractor will have structurally different CCCs — driven by contract type, owner mix, and payment terms.

The most reliable public benchmark: CFMA's 2025 Construction Financial Benchmarker reports 55.2 days in accounts receivable for fiscal year 2024 across all responding construction companies. CFMA also reports a current ratio of 1.7, quick ratio of 1.4, and 27.0 days of cash — useful liquidity markers alongside the DSO figure.

Trend analysis matters more than any single reading. A CCC shortening over consecutive quarters means faster billing cycles and healthier owner payment behavior. A CCC lengthening while revenue grows is a warning: the firm is funding that growth with working capital it doesn't yet have.

What drives those differences between firms? A few structural factors shape where your CCC will naturally land:

- Contract type — lump-sum contracts carry more billing risk than cost-plus

- Owner mix — public agency owners typically pay slower than private commercial owners

- Payment terms — net-30 vs. net-60 subcontracts move DPO in opposite directions

- Retainage rates — higher retainage artificially extends DSO until project closeout

What is a good CCC ratio?

In construction, a "good" CCC is measured against sector peers — commercial, heavy civil, and specialty trades each have different norms. Target a CCC that trends shorter over time rather than chasing a fixed number; construction will always run longer than retail or manufacturing .

What is a good cash ratio for a construction company?

The cash ratio (cash ÷ current liabilities) measures immediate liquidity, not operational efficiency. CFMA's public summary doesn't break out a standalone cash ratio benchmark, but CFMA's reported 27.0 days of cash and 1.7 current ratio provide more meaningful context. Construction firms should maintain enough cash or credit availability to cover the typical 60–90+ day lag between spending and receipt on active contracts.

Knowing where your CCC stands against these benchmarks is the starting point — the next step is identifying which lever (DSO, DIO, or DPO) offers the fastest path to improvement.

Proven Strategies to Optimize Your Construction CCC

Accelerate Billing and Reduce DSO

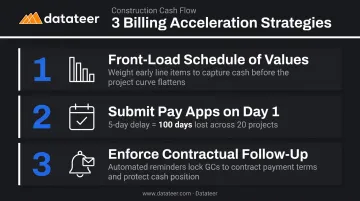

Three billing practices move the needle most:

Front-load the schedule of values. Assign higher values to early work items — mobilization, site prep, foundations — so initial payments offset cash outflow during the project's most capital-intensive phase. Legal, standard, and one of the most effective cash flow tools available at contract inception.

Submit pay applications on Day 1 of the billing window. Waiting even 5 days pushes the entire approval-to-payment cycle back by 5 days. Across a 20-project portfolio billing monthly, that's 100 days of avoidable payment delay — just from late submissions. Assign ownership to a named role with a hard submission date each month.

Enforce contractual follow-up procedures. Send reminders to owners and architects before and after approval deadlines. Most billing delays are administrative — not disputes — and a follow-up email resolves them faster than waiting out the payment cycle.

Reduce Retainage Exposure

Push for retainage reduction at contract negotiation, not after the fact:

- Request step-down from 10% to 5% after reaching 50% completion with satisfactory performance

- Negotiate milestone-based retainage releases (e.g., release foundation retainage at structure topping out)

- Ensure subcontract retainage mirrors owner retainage terms — don't hold 10% from subs if the owner is holding only 5% from you

State prompt payment laws increasingly support these positions. Contractors working in New York, California, and other states with retainage reform legislation have statutory leverage to enforce lower caps or earlier releases.

Extend and Manage DPO Strategically

Negotiate net-30 or net-45 terms with key material suppliers where volume warrants it. Use pay-when-paid provisions with subcontractors to align outflows with inflows — but don't weaponize them. Paying subcontractors 90 days late because you can doesn't improve your CCC at all — it drives your best subs to competitors and inflates material costs through lost early-pay discounts.

The goal is DPO that mirrors your own payment receipt timing, not DPO maximized for its own sake.

Monitor WIP and Billing Health Weekly

A rising underbilled position across multiple projects is a cash crunch in slow motion. By the time it appears on a month-end WIP report, the firm is already 3–4 weeks into funding work it hasn't billed for. Finance teams that review WIP weekly — or in near-real-time — catch these positions while projects still have billing opportunities ahead.

Datateer's WIP Reporting module automates costs in excess of billings, billings in excess of costs, and projected margin per job — pulled directly from the ERP each morning. Finance managers get the visibility to act on underbilling positions before they become liquidity events, without waiting two weeks for a manual report to close.

How Real-Time Data Transforms CCC Management

Most construction finance teams produce WIP reports manually: export CSVs from the ERP, run VLOOKUP reconciliations between Procore and Sage, reformat into the reporting template, review for errors. That process typically takes 10–20 days after month-end. By the time leadership sees it, the billing delays and underbilling positions it reveals are already 3 weeks old.

Automated financial dashboards that sync directly with construction ERPs eliminate that lag. Datateer pulls data overnight from Procore, Sage 100/300/Intacct, Viewpoint Vista, Viewpoint Spectrum, Acumatica Construction, Foundation Software, CMiC, Jonas Construction, QuickBooks, NetSuite, and others.

Finance managers see current WIP positions, AR aging, and billing status each morning — no manual work required.

One Double L Management business analyst described the result plainly: "That one click replaced two weeks worth of prior work." That's the difference between forensic accounting and proactive cash management.

Real-time CCC visibility also creates a shared single source of truth across the organization. When project managers and finance teams see the same WIP and billing data simultaneously, field decisions get made with awareness of the firm's actual cash position:

- Change order timing — pursue or defer based on current liquidity, not last month's report

- Cost approvals — validate against live budget-to-actual before committing

- Subcontractor mobilization — sequence draws against real cash availability

Datateer's Cash Conversion & Velocity dashboard surfaces exactly where cash is getting stuck, from unbilled work to slow-paying owners. The Retainage Tracking module separately tracks A/R retainage (withheld by owners) and A/P retainage (withheld from subs), with aging schedules per project that feed directly into 13-week cash flow forecasting. All of it starts at $10,000/year per data source, with unlimited users and a 2–4 week implementation.

Frequently Asked Questions

How do you calculate the cash conversion cycle for a construction company?

Use CCC = DIO + DSO – DPO, where DSO (billing submission to cash receipt) is typically the most impactful component. For project-level monitoring, the net cash outlay method — cumulative contract inflows minus cumulative outflows — is often more actionable than a company-wide average.

How does retainage affect the construction cash conversion cycle?

Retainage withholds 5–10% of each progress payment until project closeout, meaning contractors fund that portion of their work without receiving cash for months or years. This materially extends the effective CCC beyond what billing cycle timing alone reflects.

What is a good CCC ratio?

Most construction firms operate with a CCC between 60 and 120 days, though this varies by project type, contract structure, and retainage terms. Benchmark against sector peers rather than cross-industry averages. The most important signal is direction: a CCC trending shorter over successive quarters indicates improving cash management, regardless of the absolute number.

What is a good cash ratio for a construction company?

The cash ratio measures immediate liquidity while the CCC measures operational efficiency. Most construction firms target a cash ratio of 0.5 or higher, with enough cash or credit availability to cover the typical 60–90+ day lag between outlay and receipt across active contracts.

What is the biggest driver of a long CCC in construction?

DSO is the primary driver, specifically the billing approval process and retainage holdbacks. Payroll and material costs are incurred continuously, while owner payments arrive in delayed, partial installments with a portion withheld entirely until project closeout.

How often should construction firms review their cash conversion cycle?

At minimum, monthly, tied to the WIP report cycle. Firms managing multiple concurrent projects or rapid growth should add weekly AR aging reviews and near-real-time WIP monitoring, since billing discipline slipping across even two or three jobs simultaneously can create compounding cash shortfalls.