For construction CFOs, controllers, and finance managers, this isn't just a procurement headache. It's a direct threat to project margins, bid accuracy, and cash flow forecasting. Bids locked in months ago are now executing in a materially different cost environment.

This article breaks down which materials are rising fastest, what's driving the current escalation cycle, how margin compression happens in practice, and what firms can do to stay ahead of it.

Key Takeaways

- Construction input prices are up 43.3% since February 2020, with pace re-accelerating in 2025–2026

- Aluminum mill shapes surged 26%+ year-over-year; copper wire and cable climbed more than 22% in 2025

- New Section 232 tariffs on steel, aluminum, and copper are the primary near-term driver of price escalation

- Two in five contractors have already raised bid prices in response to tariff-driven material cost increases

- Real-time cost monitoring is the critical capability for protecting margins — monthly close cycles are too slow

Which Construction Materials Are Seeing the Biggest Price Increases

Material price inflation is not uniform. Some categories are surging while others have partially stabilized. Here's where the sharpest pressure is concentrated right now.

Steel and Metals

Steel mill products rose 12.4% year-over-year through September 2025, reaching 20.7% year-over-year by January 2026, according to AGC. The primary driver: Section 232 tariffs on steel and aluminum were raised from 25% to 50% effective June 4, 2025, compressing import supply and giving domestic producers room to push prices higher.

Aluminum mill shapes tell an even sharper story: up 26.0% year-over-year through September 2025 and 33.0% year-over-year by January 2026. AGC economist Ken Simonson noted directly that steep tariffs on imported metals are enabling domestic sellers to raise costs on construction materials and equipment.

Copper and Electrical Components

Copper wire and cable climbed more than 22% year-over-year in 2025, with a notable 4.6% spike in December alone, per ABC. Two forces are compounding: a new 50% Section 232 tariff on copper products effective August 1, 2025, and surging demand from data center construction and the energy transition.

The demand side is real. North American data center capacity under construction reached 5,994.4 MW at year-end 2025, according to CBRE. S&P Global projects AI-related data center copper demand will represent 58% of total copper data center demand by 2030. For electrical contractors and MEP subcontractors, this pressure extends well beyond current project cycles.

Lumber and Wood Products

Lumber presents a more mixed picture. Lumber and plywood is up 24.0% since February 2020, but year-over-year growth has moderated to +1.4% through September 2025. Monthly volatility remains, with a 2.0% month-over-month decline in September partially offsetting earlier gains.

Canadian softwood lumber tariffs add another layer of risk. Current tariff layers include:

- Antidumping margins: 9.65% to 35.53% depending on producer

- Countervailing duty rates: an additional 12–17% on top

- Proposed additional tariff: 25%, which NAHB flagged in early 2025 would stack on an already-effective 14.5% duty

Lumber hasn't spiked like metals. It also hasn't come close to returning to pre-pandemic pricing.

Energy Inputs and Concrete

Diesel fuel is up 8.2% year-over-year and 61.8% since February 2020, while natural gas posted a sharp 34.8% month-over-month jump in December 2025. These aren't isolated line items. Energy is a cost input for manufacturing nearly every construction material, and a transportation cost for delivering all of them.

The downstream effect on concrete is visible in the data:

- Cement: +2.2% YoY, +40.8% since February 2020

- Concrete products: +2.0% YoY, +42.0% since February 2020

- Precast concrete products: +5.5% YoY, +47.1% since February 2020

Precast concrete — used heavily in infrastructure, parking, and industrial construction — now carries one of the steeper cumulative increases across the entire materials basket, nearly 47% above pre-pandemic levels.

What's Driving Construction Material Price Increases

Four distinct forces are pushing construction material costs higher at the same time — tariffs, energy volatility, post-pandemic supply chain fragility, and sustained demand. That combination is harder to navigate than a single-cause disruption, because there's no single lever to pull.

Tariffs and Trade Policy

Tariffs are the most significant near-term driver. The key rate changes in 2025:

- Steel and aluminum Section 232: increased from 25% to 50% (effective June 4, 2025)

- Copper Section 232: 50% on semi-finished copper and derivative products (effective August 1, 2025)

- Canada IEEPA tariff: 25% on most Canadian products, 10% on energy (effective February 2025)

- Mexico IEEPA tariff: 25% on Mexican products (effective February 2025)

- Reciprocal tariff: 10% additional on all imports from all trading partners (effective April 2025)

The cost pressure is already showing up in bids. Per AGC's September 2025 survey data, two in five contractors have raised their own prices in response to tariffs on key construction materials. Tariff costs don't stop at the port — they pass through every tier of the supply chain before landing in your project budget.

Energy Price Volatility

Energy prices function as a cost multiplier across the materials supply chain. Natural gas drives cement kiln and manufacturing costs. Diesel drives delivery costs for every material category. When both spike simultaneously — as they did in late 2025 — the effect moves through nearly every line item in a construction budget.

Post-Pandemic Supply Chain Residue

The 2020–2022 supply chain crisis didn't just create temporary shortages. It durably re-priced some inputs and reduced the redundancy of supplier networks. The industry emerged from that period with thinner procurement buffers and less flexibility to absorb cost shocks from geopolitical or trade disruptions. That structural change is still a factor today.

Supply-side fragility becomes especially costly when demand stays strong — which is exactly what's happening now.

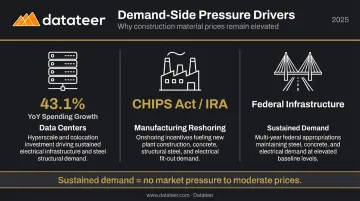

Demand-Side Pressure

Strong construction activity is preventing the market corrections that might otherwise moderate prices. Key demand drivers keeping pressure elevated:

- Data centers: U.S. data center construction spending rose 43.1% year-over-year through November 2024

- Manufacturing reshoring: CHIPS Act and IRA incentives are sustaining a wave of industrial construction starts

- Infrastructure programs: Federal infrastructure spending continues to absorb steel, concrete, and electrical materials in large quantities

With buyers competing for the same materials across multiple high-volume sectors, suppliers face no pressure to discount — which means elevated prices are likely to persist through the near term.

How Rising Material Costs Are Squeezing Construction Firm Margins

Price increases at the input level don't just raise project costs in isolation. They compress margins, distort cash flow projections, and can turn a correctly-bid project into a loss before the first foundation pour.

Project Budget and Bid Accuracy

The timing gap is the core problem. A bid prepared four to six months before project start is priced against the market conditions at bid date. If steel rises 12% and aluminum rises 26% between bid and mobilization, the project's material budget is already underwater before any work begins.

This isn't a theoretical risk. With nonresidential construction input prices up 3.2% in 2025 alone and metals surging far faster than that, the gap between estimated and actual material costs is one of the most direct mechanisms of margin fade on active jobs.

Project Cancellations and Owner Hesitancy

The owner side is reacting too. According to a ConstructConnect summary of the AGC's 2025 Construction Outlook survey (1,109 respondents), two-thirds of surveyed contractors reported that projects had been postponed or canceled. When owners hit their budget limits, they pause—and that has direct consequences for contractor revenue pipelines and backlog.

The firms most exposed are those carrying significant work-in-progress on projects bid before the current tariff cycle began.

Insurance and Indirect Cost Escalation

Higher material values don't just affect direct project costs. They increase the insured replacement value of projects under construction, which drives up property and casualty premiums. P&C premiums rose 7.7% on average in Q1 2024, according to data cited in construction-industry insurance analysis from Morris & Garritano—and that was before the additional tariff-driven material cost escalation of 2025.

The Financial Monitoring Gap

Material cost volatility demands faster financial visibility. The problem: most construction firms still rely on monthly close cycles and manually assembled WIP reports. By the time margin erosion appears in a standard monthly report, the project has already moved—and the window for intervention has narrowed or closed entirely.

That's the gap Datateer is built to close. The Material Price Tracking & Escalation Analytics module gives finance teams a live view of exposure across active jobs:

- Tracks actual purchased cost per unit for steel, copper, lumber, concrete, and fuel

- Trends unit costs over time and compares them against bid-estimate prices

- Benchmarks against external indices including the PPI and ENR Material Cost Index

- Rolls escalation impact up to project margin so at-risk jobs are visible before they become a quarterly surprise

Combined with Datateer's Cost Variance and Job Costing & Cost-to-Complete modules, the platform replaces the traditional 10–20 day WIP reporting lag with automated overnight data syncs pulling from ERPs including Sage, Viewpoint Vista, Procore, Acumatica, and others. Double L Management put it plainly: "That one click replaced two weeks worth of prior work."

How Construction Firms Can Respond to Material Price Volatility

There's no single fix for a volatile materials market, but three operational levers reduce exposure:

Contractual Price Protection

- Include material cost escalation clauses that allow price adjustments if key material indices move beyond a defined threshold

- Use material cost allowances for highly volatile line items rather than lump-sum pricing

- Specify which market indices (PPI, ENR) trigger adjustment rights and document them clearly in the contract

Procurement Timing and Diversification

- Accelerate early purchasing for tariff-exposed materials where storage is practical — two in five contractors are already doing this

- Expand vendor relationships to include domestic alternatives for import-dependent categories like aluminum and steel

- Lock in supplier pricing through forward purchase agreements where volume justifies it

Real-Time Financial Monitoring

- Model multiple cost scenarios (base, moderate, elevated) into project budgets rather than single-point estimates

- Track actual purchased material costs against bid estimates continuously, not just at month-end

- Use platforms with dedicated material escalation and margin protection analytics — like Datateer's Material Price Escalation and Margin Protection dashboards — to identify which jobs are margin-vulnerable before costs compound

Firms that rely on procurement alone to manage material risk — without the financial monitoring infrastructure to catch cost variance early — typically discover margin damage at month-end, when the window to course-correct has already closed.

Future Signals: What to Watch in Construction Material Prices

Tariff policy resolution is the single most consequential variable in the near-term outlook. As long as Section 232 duties on steel, aluminum, and copper remain at 50%, and broad IEEPA tariffs on Canada and Mexico stay in place, domestic producers will continue to benefit from reduced import competition. Any negotiated trade resolution—particularly with Canada, which is a major supplier of both lumber and aluminum—could provide meaningful relief. Escalation would push prices higher through the remainder of 2025 and into 2026.

Beyond tariffs, the signals worth watching:

- Energy prices: Oil and natural gas movements translate almost directly into manufacturing and transport costs across all material categories

- Copper demand: AI data center buildout is a durable demand driver for copper—not a short-term spike

- Construction activity levels: If strong commercial and industrial demand continues, there's limited market pressure to moderate prices

Construction material prices are not returning to pre-2020 norms in any near-term scenario. The cumulative 43.3% increase since February 2020 represents a structural repricing of the input cost base — and firms should plan accordingly.

The firms best positioned to protect margins are pairing strategic procurement with financial systems that surface cost exposure in real time, so decisions get made before the monthly close rather than in reaction to it.

Frequently Asked Questions

Are construction materials going up in price?

Yes. Construction input prices rose 2.8% in 2025 and remain 43.3% above February 2020 levels. After a period of moderation in 2023–2024, tariffs on steel, aluminum, and copper have re-accelerated price growth, particularly in metals and electrical components.

How much have construction materials increased since 2020?

Overall construction inputs have risen 43.3% since February 2020, per AGC's BLS PPI tracking. Specific categories have climbed even more—copper and brass mill shapes are up 69.8% over the same period, and precast concrete is up 47.1%.

Is it normal for contractors to upcharge materials?

Yes—contractors typically pass material cost increases through via bid pricing or contractual escalation clauses. With tariffs and energy costs pushing key materials up sharply, upcharges have become more frequent and larger. Two in five contractors surveyed by AGC-NCCER have already raised prices specifically in response to tariffs.

What construction materials will be affected by tariffs?

Steel, aluminum, copper, and lumber face the most direct tariff exposure. Section 232 duties of 50% now apply to steel, aluminum, and copper imports. Broad IEEPA tariffs on Canada and Mexico affect lumber and dozens of other material categories, putting virtually every materials budget line at risk.

How do material price increases affect construction project budgets?

Price increases between bid date and construction start can turn a profitable bid into a loss-making project. With materials rising several percent over a matter of months, the gap between estimated and actual costs is a primary driver of margin fade. Catching that gap requires continuous budget monitoring—not just end-of-month reporting.

How can construction companies protect their margins when material costs rise?

Three approaches consistently protect margins in a rising-cost environment:

- Contract escalation clauses that allow price adjustments tied to PPI or ENR index movements

- Early material procurement to lock in prices before further increases

- Real-time cost tracking to catch overruns before they compound

Platforms like Datateer's Material Price Escalation and Cost Variance modules deliver the continuous visibility that monthly close cycles miss when prices are moving fast.