That definition sounds straightforward. The execution is anything but.

For general contractors, specialty contractors, construction CFOs, and finance managers, job costing is the financial operating layer that separates firms that protect their margins from those that discover problems at closeout. Unlike manufacturing, no two construction projects share the same scope, location, subcontractor mix, or cost structure—which makes project-specific cost tracking not just useful, but essential.

This guide covers what job costing is, the five core cost categories, how the process works step by step, the most common challenges firms face, and what separates reactive reporting from a genuinely proactive job costing practice.

Key Takeaways

- Job costing tracks all project-level costs against the original estimate so contractors can spot overruns before they erode margin.

- The five core cost categories—labor, materials, equipment, subcontractors, and overhead—each require a distinct tracking methodology.

- Accurate job costing depends on timely data entry, standardized cost codes, and real-time visibility across field and office.

- WIP reporting is the financial output of job costing and the primary tool for assessing per-project profitability.

- Most job costing failures trace back to data that reaches decision-makers too late to act on.

What Is Job Costing in Construction?

Job costing is a project-specific accounting method that breaks down all expenditures into defined categories for a single job, creating an ongoing financial picture that is completely separate from company-wide financial reporting.

The Construction Financial Management Association (CFMA) describes job costing as a contractor's report card—for both completed and active contracts—and as a guidepost for future work. That distinction matters: a report card implies accountability at the job level, not just the company level.

Job Costing vs. the General Ledger

A general ledger captures every company transaction but cannot isolate the profit or loss of an individual project. Job costing adds a project-level layer on top of that, enabling per-job profitability analysis. Without it, a contractor can be profitable on paper while quietly losing money on three of their five active projects.

At the job level, that means tracking three things the GL cannot show you:

- Which projects are generating profit vs. quietly burning it

- Where cost overruns are occurring (labor, materials, subcontractors, or overhead)

- Whether your current backlog is actually healthy or just looks that way on paper

Job Costing vs. Process Costing

According to OpenStax's managerial accounting framework, job order costing traces individual costs directly to a specific job or service, while process costing assigns costs by process or department across continuous, uniform production runs.

Construction firms use job costing almost exclusively because no two projects are identical. Each has its own scope, site conditions, crew composition, and subcontractor structure — making the standardized averages of process costing functionally useless at the project level.

The Key Components of Construction Job Costing

Every job cost system must capture five primary cost categories. Each one behaves differently and requires its own tracking logic.

Labor Costs

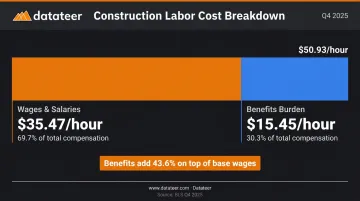

Labor is typically the largest and most variable cost on any project. Tracking it correctly means capturing more than hourly wages—it requires including the full payroll burden.

According to the U.S. Bureau of Labor Statistics (Q4 2025), private construction compensation runs $50.93 per hour, broken down as:

- $35.47/hour in wages and salaries (69.7% of total compensation)

- $15.45/hour in benefits (30.3% of total compensation)

That means benefits add roughly 43.6% on top of base wages. A contractor who only tracks wage cost is undercounting their true labor expense by nearly half.

Every time entry must be coded to the correct job, phase, and cost code at the moment it's recorded—not reconstructed from memory a week later. CFMA states explicitly that job-cost data should be captured using mobile technology to record labor and equipment hours directly from the field.

Materials Costs

Materials must be tracked as they are received or consumed, tied to specific cost codes, and cross-referenced against purchase orders. One often-overlooked category: committed costs—open purchase orders that have been issued but not yet invoiced. If those POs aren't included in the cost picture, a project can appear under budget right up until the invoices arrive.

Per CFMA, materials are a direct job-cost component and should be assigned with the same rigor as labor. When that discipline breaks down—a delivery receipt miscoded or left unmatched—costs bleed into the wrong job or disappear into overhead, quietly distorting every project's profitability picture.

Equipment Costs

Equipment costs present a different tracking challenge from materials. Owned equipment is where costs get understated most often: if a piece of equipment is deployed at no internal charge, the project looks more profitable than it actually is—until depreciation, maintenance, fuel, and insurance show up elsewhere in the financials. The standard approach is to establish an internal charge rate based on expected rental value, with time-based allocation as the most accurate method since repairs and maintenance track closely with hours on-site.

Rented equipment is simpler: allocate the invoice directly to the job.

Subcontractor and Overhead Costs

Subcontractor costs must be tracked against contracted amounts and any approved change orders. When scope creep occurs and subcontractors complete work before a change order is formally approved, the contractor absorbs costs with no corresponding budget or billing adjustment.

Overhead requires a different approach. Costs like insurance, office rent, and administrative salaries don't tie to a single job—they must be allocated proportionally across all active projects using a consistent method (typically a percentage of direct labor or total direct costs). CFMA's 2024 Construction Financial Benchmarker reports SG&A expenses of 11.8% of revenue for typical firms and 10.8% for best-in-class performers—useful context when setting overhead allocation rates.

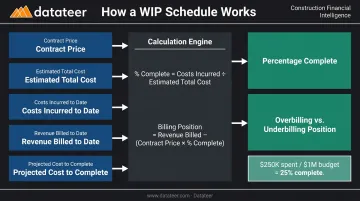

Work in Progress (WIP) Reporting

WIP reporting is the financial output that connects job costing to revenue recognition. According to AICPA-CIMA, an effective WIP schedule requires:

- Contract price

- Estimated total project cost

- Costs incurred to date

- Revenue billed to date

- Projected cost to complete

From those inputs, the WIP schedule calculates percentage complete, earned revenue, and whether each job is in an overbilling or underbilling position. AICPA-CIMA's example: if $250,000 has been spent against a $1,000,000 budget, the project is 25% complete—and only 25% of revenue and gross profit should be recognized. One critical caution from CFMA: overbillings should be treated as cash reserved to fund remaining work, not recognized as immediate profit.

The stakes extend beyond internal reporting. Sureties use WIP reports to assess financial health, backlog, and capacity across a contractor's entire portfolio—which means WIP quality directly affects bonding capacity.

How Job Costing Works: A Step-by-Step Process

Job costing spans the full project lifecycle — from the moment a contract is awarded through final closeout, when estimated costs get measured against what was actually spent.

Step 1: Establish the Project Budget and Cost Code Structure

Before any work begins, the estimating team's cost breakdown must be translated into a formal job budget organized by standardized cost codes. Done poorly, it undermines every cost comparison that follows.

If the estimating team uses different cost codes than the accounting team, comparing estimated vs. actual costs becomes guesswork. CSI's MasterFormat is the most widely used industry standard, though many firms layer firm-specific codes on top of it. The structure must support budget, actual, and estimate-at-completion analysis simultaneously — not just one of those three.

Step 2: Capture and Allocate Costs as Work Progresses

Every labor hour, material receipt, equipment usage entry, and subcontractor invoice must be coded to the correct job and cost code at the time of occurrence—not retroactively.

Key principles for this step:

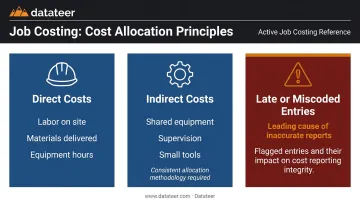

- Direct costs (labor on site, materials delivered, equipment hours) are allocated to the specific job and cost code they belong to.

- Indirect costs (shared equipment, supervision time, small tools) are allocated using a documented methodology applied consistently across jobs.

- Late or miscoded entries are the single most common cause of inaccurate job cost reports—not missing data, but data entered late or in the wrong place.

Step 3: Monitor, Compare, and Forecast

Active financial management means running continuous comparisons across three figures: budget vs. committed vs. actual.

Weekly reviews by operations and finance teams should cover:

- Which cost codes are trending over budget, and by how much

- Whether labor forecasts need to be adjusted based on current productivity

- Whether pending change orders have been formally logged and are awaiting approval

- What the revised cost-at-completion looks like compared to the original estimate

The purpose of this review cadence is early warning: catching cost overruns while the project team still has time to respond, before margin erodes past the point of recovery.

Common Job Costing Challenges (and How to Solve Them)

Delayed and Incomplete Data

When field teams enter time, material receipts, or equipment usage days after the fact, the job cost report reflects a past financial state rather than the current one. A project can appear on budget right up until a large closeout surprise. CFMA's standard is clear: job-cost information should be as close to real time as possible.

Solution: Invest in mobile-first field data entry tools and establish clear daily or weekly submission standards by role—not suggestions, but defined requirements.

Misallocated Costs

Expenses coded to the wrong job or cost code distort profitability at every level. This happens when field staff lack visibility into the budget structure, or when cost code lists differ between estimating and accounting systems. CFMA notes that omitting or misallocating indirect costs leads to inaccurate conclusions and ineffective strategies.

Solution: Standardize cost codes across both estimating and accounting, train all stakeholders on coding expectations, and run weekly exception reports to catch miscoded transactions before they compound.

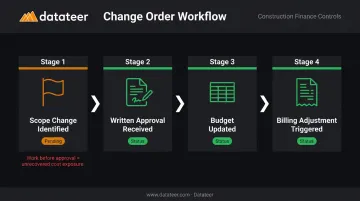

Failing to Account for Change Orders

Scope changes performed before formal approval mean contractors absorb out-of-scope labor and materials with no corresponding budget or billing adjustment. FMI identifies this as a primary driver of gross margin fade. AGC defines a change order as a formal, written agreement. Anything short of that creates financial exposure.

Banks and sureties scrutinize unapproved change orders closely. Removing them from contract value damages working capital, equity, and credit credibility — a point CFMA flags as a direct threat to bonding capacity.

The fix: Implement a formal change order workflow that logs potential changes as "pending" before work begins, updates the budget only upon written approval, and triggers a billing adjustment automatically.

Real-Time Visibility Gaps

Many firms still rely on monthly close cycles to produce WIP reports, meaning decision-makers are working with data that is 10–20 days old. By the time a budget overrun appears in a report, the opportunity to act may have passed.

This is the challenge Datateer's construction finance dashboards are built to solve. By syncing directly with a firm's ERP overnight (with more frequent refresh available when needed), the platform eliminates the manual WIP process entirely. Double L Management's business analyst put it plainly: "that one click replaced two weeks worth of prior work." Finance teams move from forensic accounting to active oversight of what's happening right now.

Best Practices for Accurate and Proactive Job Costing

Three practices separate firms with functional job costing from those with genuinely proactive systems:

1. Align cost codes between estimating and accounting. Variance analysis is only meaningful when the two sides of the comparison speak the same language. This isn't a one-time setup task—it requires ongoing upkeep as projects evolve and code structures change.

2. Establish a weekly operations-finance review cadence. Project managers and accounting teams should review cost code performance together weekly, agree on updated forecasts, and flag codes trending the wrong way. Datateer's PM Scorecards support this cadence directly—tracking budget variance, margin variance, change order win rate, and earned value per project manager, turning uncomfortable conversations into data-backed reviews.

3. Allocate all indirect costs using a documented, consistent methodology. Every project should reflect its true cost burden. If overhead allocation varies by project or isn't applied at all, the profitability comparisons between jobs are meaningless.

Connecting Job Costing to Company-Wide Financial Intelligence

Job costing should not operate in isolation. When project-level actuals feed directly into company-wide cash flow forecasts, WIP schedules, and bonding reports, finance managers shift from reactive reporting to strategic advising.

For firms managing multiple concurrent projects, manual aggregation creates both lag and error risk. Datateer's platform automates the full data pipeline—from ERP to executive dashboards—replacing days of manual formatting with overnight-refreshed financial intelligence. Key areas covered include:

- Job costing and cost-to-complete

- WIP reporting and over/under-billings

- Margin protection and change order tracking

- Overhead and burden rate analytics

All of this runs under flat annual pricing with unlimited users and no per-seat fees.

Historical Actuals as a Competitive Advantage

Accurate job costing creates a proprietary database of historical performance data. Estimators who can review actual labor hours, material costs, and subcontractor performance by crew type and project category will validate assumptions faster, explain past variances with confidence, and submit sharper bids. The CFMA frames job costing as a "guidepost for future work"—which is precisely what it delivers when the underlying data is clean and consistently organized.

Conclusion

Job costing is the financial layer that lets contractors see not just where money was spent, but whether each project will be profitable before it's too late to change the outcome.

The process — budgeting, coding, capturing, comparing — is well understood. The firms that execute it best aren't running a more complicated system. They're getting cost data in front of decision-makers faster, while projects can still be steered.

Moving from monthly forensic reporting to real-time job cost monitoring gives project teams and finance managers the ability to protect margins, manage cash flow, and win better work. That shift requires clean, automated data flowing directly from the ERP — which is exactly what platforms like Datateer are built to deliver. When historical job cost data is accurate and accessible, it stops being a compliance exercise and starts driving smarter bids, tighter scopes, and stronger margins on the next project.

Frequently Asked Questions

What is job costing in construction accounting?

Construction job costing assigns all project costs—labor, materials, equipment, subcontractors, and overhead—to individual jobs so contractors can track profitability in real time. Unlike general ledger reporting, it isolates the financial performance of each project rather than consolidating everything at the company level.

What are the 7 steps in job costing?

The seven core steps are:

- Establish the project budget and cost codes

- Capture direct costs (labor, materials, equipment)

- Allocate indirect and overhead costs

- Track committed costs

- Monitor actuals vs. budget by cost code

- Manage change orders formally

- Compare final actuals to the original estimate to improve future bids

What are the 4 types of cost accounting?

The four main methods are job costing, process costing, activity-based costing, and standard costing. Construction firms use job costing almost exclusively because each project has a unique scope, site, and cost structure that makes averaging costs across jobs meaningless.

What is the difference between job costing and process costing?

Job costing tracks costs for individual, unique projects—standard in construction. Process costing averages costs across large volumes of identical units, which is common in manufacturing. Since no two construction projects share the same scope or conditions, process costing doesn't apply.

What is a construction cost accountant's role in job costing?

A construction cost accountant sets up the job cost structure and ensures every transaction is coded correctly. Core responsibilities include producing WIP reports, reconciling committed vs. actual costs, and delivering accurate financial performance data to project managers and executives from start to finish.

How does WIP reporting relate to job costing?

WIP reporting is the primary financial output of job costing. It uses cost-to-date, estimated cost at completion, contract value, and billings to calculate over- or under-billing status and forecast final margin. That makes it essential for monthly close, bonding capacity, and margin management.