The consequences compound. Misclassified costs distort job cost reports, corrupt WIP data, and create margin fade that only becomes visible well after the losses are locked in. FMI documented a project bid at a 51% gross margin that finished at 11.2% — a 40-point write-down driven by factors that were present from day one but never surfaced in time.

This guide covers how to define, identify, calculate, and manage both cost types so your bids reflect the true cost of doing the work.

Key Takeaways

- Direct costs are traceable to a specific project: labor, materials, equipment, and subcontractors

- Indirect costs (overhead, G&A, general conditions) support operations across projects and can't be tied to a single activity

- Both belong in every bid; underestimating either leads to structural underpricing

- Indirect costs split into recurring (duration-driven) and non-recurring (one-time) — each estimated differently

- Allocation method consistency matters more than which method you choose

Direct vs Indirect Costs: Quick Comparison

| Attribute | Direct Costs | Indirect Costs |

|---|---|---|

| Definition | Traceable to a specific project activity | Support overall operations; spread across projects |

| Examples | Labor wages, materials, subcontractors, dedicated equipment | Office rent, admin salaries, insurance, shared tools |

| Traceability | High — tied to specific scope items | Low — allocated on a predetermined basis |

| Allocation method | Applied directly to the project | Percentage of cost, labor hours, equipment usage, ABC |

| Impact on profitability | Overruns inflate project cost directly | Omission or undercovery erodes margin across the portfolio |

Miss either category in your estimate and the budget gap shows up late — usually after mobilization, when course correction is costly. Getting both right from the start is what separates accurate bids from money-losing ones.

What Are Direct Costs in Construction?

Direct costs are all expenses that can be directly traced to a specific construction project, task, or activity. Per RSMeans, they are expenses "linked to the physical construction of a project" — the costs needed to complete the build itself.

Examples of Direct Costs in Construction

The core categories:

- Labor wages and burden — craft wages plus FICA, workers' comp, and benefits loaded onto each hour

- Materials and supplies — raw materials, structural components, consumables

- Equipment — owned or rented machinery used exclusively on one project

- Subcontractor payments — specialized trades contracted for project-specific scopes

- Site-specific costs — excavation, temporary structures, project-specific permits, site safety equipment

One classification that trips up many firms: project manager and superintendent salaries count as direct costs when those staff are dedicated to a single project. When someone splits time across jobs, their wages must be allocated proportionally — not assigned wholesale to one project's direct cost column.

How to Calculate Direct Costs

Direct Costs = Labor + Materials + Equipment + Subcontractor Payments + Other Project-Specific Costs

The accuracy of this number depends entirely on how completely each component is identified during estimating — not at project close.

Labor is consistently the highest-risk component. Three data points illustrate why historical rates can't be trusted at face value:

- The AGC's 2024 Workforce Survey found 94% of construction firms had difficulty filling craft positions, pushing wages above budgeted expectations

- FMI's 2024 Construction Index found 51% of civil infrastructure respondents reported labor cost overruns against budget

- The BLS recorded a 2.8% increase in private-industry construction compensation for the 12 months ending September 2024

That 2.8% figure looks modest until it's multiplied across thousands of labor hours on a large project.

What Are Indirect Costs in Construction?

Indirect costs support the overall business and project environment without being part of the physical work itself. They cannot be traced to a single construction activity and are instead allocated across projects on a consistent allocation formula. You'll see them called overhead, G&A, preliminary costs, or general conditions depending on context.

Types of Indirect Costs in Construction

1. General overhead Office rent, utilities, office supplies — the costs of keeping the business running regardless of project activity.

2. G&A (General & Administrative) Administrative salaries, HR, accounting staff, marketing — corporate-level costs not tied to field operations.

3. Project-specific indirect costs (general conditions) On-site supervision staff, temporary site facilities, site utilities, PPE, waste disposal. RSMeans benchmarks general conditions at 5–15% of total project cost including O&P, with 10% as a common midpoint.

4. Shared tools and equipment Machinery that moves across multiple projects rather than being dedicated to one.

5. Insurance and bonding General liability, builder's risk, workers' comp, and performance bonds.

6. Regulatory compliance Permit fees, inspections, and environmental compliance costs not tied to a specific scope item.

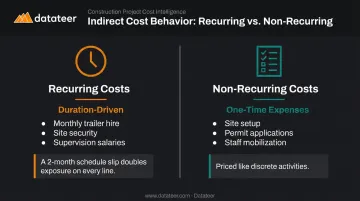

Recurring vs. Non-Recurring Indirect Costs

This distinction is a practical estimating tool that most firms underuse:

- Recurring costs (monthly trailer hire, security, site supervision salaries) are duration-driven. A two-month schedule slip doubles your exposure on every line in this category.

- Non-recurring costs (site setup, permit applications, staff mobilization) are one-time expenses priced like discrete activities.

Understanding which indirect costs are schedule-sensitive and which aren't lets you build a budget that actually flexes when project timelines shift — instead of discovering the gap at project completion.

How to Calculate Indirect Costs

Indirect Cost Rate = Total Indirect Costs ÷ Total Direct Costs

This rate is applied proportionally across projects to ensure overhead is recovered across the portfolio. Most construction firms target a rate between 10–25% of direct costs, though the right number depends on company size, project mix, and how much overhead you carry between jobs.

Unlike direct costs, no drawing or specification prescribes indirect costs. They're driven by team assumptions about duration, scope, and resource needs — which makes them susceptible to omission and schedule-slip risk. A bid priced on a 12-month duration is underpriced if the project runs 16 months.

How to Distinguish Direct from Indirect Costs

The Three-Question Test

When a cost is ambiguous, run it through these questions:

- Can you trace this expense directly to a specific project activity?

- Would this cost disappear if this project didn't exist?

- Is this cost driven by project scope or by business operations?

If questions 1 and 2 are both "yes" — it's a direct cost. If either answer is "no" — it's likely indirect.

The Gray Area Problem

The same cost can land on either side of the line depending on context. Traffic management is a clean example:

- A traffic controller assigned to a specific task (concrete pour access, crane lift) = direct cost

- A traffic controller stationed at the site gate every day regardless of activities = indirect cost

The classification itself matters less than applying it consistently within your firm's cost coding system. A company that always codes site supervision as direct isn't wrong. A company that codes it differently from job to job, though, produces distorted job cost comparisons, unreliable WIP data, and bids that estimators can't compare apples-to-apples.

Fixed vs. Variable Costs Within Each Category

Both direct and indirect costs can be fixed or variable:

| Fixed | Variable | |

|---|---|---|

| Direct | Dedicated PM salary | Material quantities, equipment fuel |

| Indirect | Monthly office rent | Shared equipment usage, site security |

Budgets that account for this distinction let finance teams model how costs respond when scope expands or schedules slip, rather than treating every line as fixed.

Why Misclassification Compounds Over Time

A misclassified indirect cost in a bid doesn't just affect one project. If supervision wages are excluded from overhead recovery calculations, every subsequent bid built on that template carries the same gap. FMI's research attributes $1.84 trillion in construction industry losses in 2020 to poor data management, with 14% of rework caused by bad data — a figure that includes classification errors that compound through estimates, job cost reports, and WIP schedules simultaneously.

How to Manage Direct and Indirect Costs in Construction

Allocation Methods for Indirect Costs

Four methods cover most use cases:

- Percentage of project cost — Simple and common, but ignores actual resource consumption. Works for firms with homogeneous project types.

- Direct labor hours/costs — Appropriate for labor-intensive work where overhead consumption correlates with labor activity.

- Equipment usage — Better fit for machinery-heavy projects where equipment drives overhead exposure.

- Activity-based costing (ABC) — Most precise for complex, multi-phase projects with distinct overhead pools. Higher setup cost, higher accuracy.

No single method is universally correct. The bigger risk is inconsistency — changing methods between bids or projects without adjusting comparisons to account for the change.

Best Practices for Tracking and Controlling Both Cost Types

For direct costs:

- Use detailed upfront estimates with historical unit cost data, not assumptions

- Involve field staff in the estimating process — they catch scope-specific cost drivers that office estimators miss

- Track actuals against budget at the cost-code level in real time, not just at monthly close

- Flag labor slippage early; at 2.8% annual wage escalation, a delayed schedule inflates labor costs beyond what the original burden rate covers

For indirect costs:

- Review allocations against actuals regularly — don't assume the rate you set at project start is still accurate at month six

- Build contingency into overhead budgets specifically for schedule slippage on recurring cost categories

- Update cost drivers based on current market conditions rather than carrying forward historical percentages year over year

Real-Time Visibility Across the Portfolio

For firms managing multiple concurrent projects, the limiting factor is usually visibility speed, not analytical intent. When cost and WIP data lives in spreadsheets, finance teams can't see what's happening on a project until the data is already weeks old.

Those tracking practices above only hold if the underlying data is current — which is where most multi-project firms break down.

Datateer integrates directly with construction ERPs — Procore, Sage 100/300/Intacct, Viewpoint Vista, Viewpoint Spectrum, Acumatica, Foundation Software, CMiC, and others — to deliver real-time job cost and WIP dashboards. The Overhead & Burden Rate Analytics module compares budgeted burden rates to actuals, monitors overhead absorption per project, and flags under-allocated overhead before it erodes end-of-job margin.

Clients like Double L Management have noted that automated reporting replaced two weeks of prior manual work with a single click. The Margin Protection module monitors original estimated margin versus current projected margin per job, surfacing the specific cost codes and phases driving deterioration — so finance teams can intervene while the project is still in progress rather than documenting the loss after close.

Conclusion

Direct and indirect costs are both required inputs in every project's financial equation. The risk isn't misunderstanding their definitions — it's failing to identify, classify, and track them consistently, which causes bids to erode and profitability to erode across the portfolio without anyone catching it in time.

Accurate cost classification is the difference between reactive project accounting and proactive financial management. Get both categories right in your estimates, apply consistent allocation methods, and build reporting systems that surface variances in real time. That's how you protect margins, keep WIP reports clean, and catch cost overruns while there's still time to act — not after the project closes.

Datateer's Job Costing, Cost Variance, and Overhead & Burden Rate dashboards automate exactly this kind of tracking — pulling directly from your ERP so your team sees budget-vs-actual and allocation variances in real time, without the spreadsheet grind.

Frequently Asked Questions

What are examples of direct and indirect costs in construction?

Direct costs include labor wages and burden, raw materials, subcontractor fees, and dedicated equipment. Indirect costs include office rent, administrative salaries, shared equipment maintenance, site supervision under general conditions, and insurance premiums. Both categories must appear in every project budget.

What is the difference between direct and indirect costs in construction?

Direct costs are traceable to a specific project activity and would disappear if that project didn't exist. Indirect costs support overall business operations and are allocated across multiple projects or the entire firm — necessary to execute the work, but not part of the work itself.

How are indirect costs allocated across construction projects?

Common methods include percentage of project cost, direct labor hours, equipment usage, and activity-based costing. Each method suits different project types. Consistency of method across bids and projects matters more than which method you choose.

What is the difference between indirect costs and soft costs in construction?

Soft costs (architectural fees, design fees, land acquisition) are pre- or post-construction expenses for intangible services. Indirect costs are more closely tied to supporting on-site operations during active construction, such as supervision, temporary facilities, and insurance.

How do direct and indirect costs affect construction project profitability?

Underestimating either type creates structural underpricing from the first bid. Untracked indirect costs erode margins through overhead recovery gaps, while poorly managed direct costs (especially labor) produce budget overruns that surface too late to correct.

What happens when indirect costs are misclassified as direct costs?

Misclassification distorts job cost reports and WIP schedules, making projects appear more profitable than they are mid-stream. It also breaks overhead recovery calculations, leaving G&A and field indirect costs unrecovered and driving systematic margin fade across the portfolio.