That's where the WIP report earns its keep. It functions as the financial backbone connecting field activity to financial reality—tracking what's been spent, what's been earned, and where billing stands on every active job. According to KPMG's 2023 Global Construction Survey, 37% of respondents missed budget or schedule targets due to insufficient risk management. Better WIP visibility is one of the clearest fixes available.

This guide covers everything construction finance teams need: WIP definitions, report components, calculation methods, common mistakes, balance sheet treatment, and what modern reporting actually looks like when the manual spreadsheet grind is removed from the equation.

Key Takeaways

- WIP tracks costs incurred, work completed, earned revenue, and billing position across all active jobs

- Percentage of completion drives earned revenue—not how much budget has been spent

- Overbilling is a liability; underbilling is an asset; both must appear on the balance sheet

- Outdated cost estimates skew every WIP calculation downstream

- Automated platforms like Datateer replace weeks of manual spreadsheet work with daily, accurate WIP visibility

What Is Construction Work In Progress (WIP)?

WIP is an accounting concept that captures the financial status of every active construction contract—tracking costs incurred, work completed, and revenue earned for jobs that are underway but not yet finished. As AICPA-CIMA describes it, an effective WIP schedule includes contract price, estimated total project cost, costs to date, and requisitions to date. It is not simply a general ledger entry—it is a management report that sits alongside the financial statements and drives revenue recognition decisions.

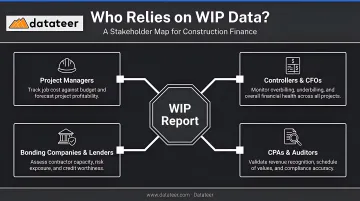

Who Relies on WIP Data

The WIP report serves a broad audience across the business:

- Project managers — monitoring job health and cost performance in real time

- Controllers and CFOs — preparing accurate financial statements and managing revenue recognition entries

- Bonding companies and lenders — sureties evaluate WIP to assess financial condition, underbillings, open change orders, and remaining bonding capacity

- CPAs and auditors: verifying internal controls and confirming financial statement accuracy

Per HBK, sureties, banks, and investors often prioritize WIP schedule analysis over historical income statements because WIP reflects expected future performance—not what already happened.

Why It Matters in Practice

Consider a concrete example: a project is 50% complete by schedule but has consumed 75% of the budget. Without a WIP report, that gap stays invisible until project close. With one, the finance team sees it at the next reporting cycle and still has time to address it—whether through scope negotiation, a change order, or a conversation with the project manager about productivity.

That's the practical difference between reacting to a loss after the fact and catching a margin problem while the project is still running.

Key Components of a Construction WIP Report

Every line item in a WIP report flows from a small set of inputs. Nail these and the rest follows naturally—but weak inputs corrupt every calculation downstream.

Contract Value and Estimated Costs

The starting point is the original contract amount plus all approved change orders. Alongside that sits the revised total estimated cost to complete—and keeping this number current is the single most important discipline in WIP management. Stale estimates corrupt every calculation that follows.

Costs to Date

All direct job costs incurred—labor, materials, subcontractors, equipment, and allocated overhead—accumulate here. Committed costs (purchase orders and subcontract agreements not yet invoiced) must also be tracked. If they're excluded, the percentage complete will be overstated and the WIP report will tell a more optimistic story than the job actually supports.

Percentage Complete and Earned Revenue

These two metrics are linked by a simple relationship:

- % Complete = Costs to Date ÷ Revised Estimated Total Cost

- Earned Revenue = % Complete × Contract Value

Earned revenue reflects what the contractor has actually produced—not what has been invoiced. Conflating the two leads to misstated revenue and unreliable project financials.

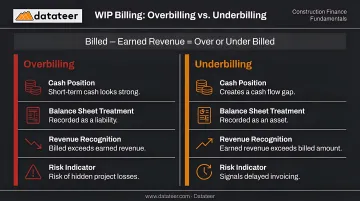

Billed to Date and Over/Underbilling

- Overbilling: Billed amount exceeds earned revenue → a liability

- Underbilling: Earned revenue exceeds billed amount → an asset

Both conditions distort financial statements if left unaddressed. The WIP report makes them visible in real time instead of surfacing them at year-end during an audit.

Projected Profit and Margin Fade

The WIP report should show estimated profit at completion alongside the original budgeted profit. When these diverge as the project progresses, it signals margin fade—often caused by scope creep, change order delays, or inaccurate cost forecasts. As HBK notes, monthly WIP schedules help identify warning signs early enough to course-correct before margin damage becomes permanent.

How to Calculate WIP: Percentage of Completion, Overbilling, and Underbilling

Percentage of Completion Formula

The core formula:

Costs to Date ÷ Revised Estimated Total Cost = % Complete

% Complete × Contract Value = Earned Revenue to Date

Example: A $2M contract has $1.6M in revised estimated costs. The project has incurred $400K in costs to date.

- % Complete = $400K ÷ $1.6M = 25%

- Earned Revenue = 25% × $2M = $500K

If the contractor has billed $600K, they're overbilled by $100K. If they've billed $400K, they're underbilled by $100K.

Identifying Overbilling and Underbilling

Formula: Amount Billed – Earned Revenue = Over or Under Billed

| Overbilling | Underbilling | |

|---|---|---|

| What it means | Billed more than earned revenue to date | Earned revenue exceeds what's been invoiced |

| Balance sheet impact | Liability (obligation to perform future work) | Asset (work completed but not yet billed) |

| Cash flow effect | Cash looks strong short-term | Creates a cash flow gap |

| Risk | Treating it as profit funds operations while creating a hole that surfaces at project close | Signals delayed invoicing or change order backlogs that constrain liquidity even on profitable jobs |

WIP Calculation Methods Beyond Cost-to-Cost

The cost-to-cost method is the most common, but it's not the only option. RSM identifies two categories of progress measurement under ASC 606:

| Method Type | Examples | Best Suited For |

|---|---|---|

| Input methods | Cost-to-cost, labor hours expended | Most construction contracts |

| Output methods | Units delivered, milestones reached, surveys of performance | Repetitive scopes (concrete pours, framing units) |

A third approach—estimated cost-to-finish—has the project manager estimate remaining cost, which is added to cost-to-date to establish a revised budget. This is useful when field conditions have shifted significantly from the original estimate.

One critical rule: ASC 606 requires consistent application of the chosen method across similar performance obligations in similar circumstances. Mixing methods across projects without documentation creates audit exposure.

Common WIP Mistakes That Erode Profit Margins

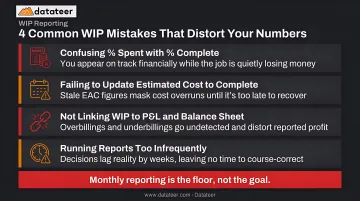

Confusing Percent Spent with Percent Complete

This is the most widespread WIP error. A project can have consumed 60% of its budget while being only 40% complete—meaning the contractor is already heading toward an overrun without knowing it. Using budget consumption as a proxy for physical progress overstates earned revenue, distorts billing, and creates a gap that only becomes visible when it's too late to close.

Failing to Update Estimated Cost to Complete

Outdated cost estimates—particularly when change orders are pending or scope has shifted—corrupt every downstream calculation. The WIP schedule is a living document. It should be revisited at every reporting cycle with direct input from project managers, not reconstructed by accounting from historical data alone.

Assurance Dimensions identifies incomplete or outdated information as one of the most frequent WIP problems found by construction CPAs—alongside exaggerated profit margins and poor field-progress monitoring.

Not Linking WIP Adjustments to the P&L and Balance Sheet

Under ASC 606, three entries are non-negotiable:

- Overbilling → recorded as a contract liability ("billings in excess of costs")

- Underbilling → recorded as a contract asset ("costs in excess of billings")

- Missing journal entries → misstated income statement and balance sheet

Skipping these adjustments creates compliance risk and erodes credibility with bonding companies and lenders—often at the worst possible moment.

Running WIP Reports Too Infrequently

Accurate accounting means nothing if the data arrives too late to act on. A monthly WIP report is already 30 days stale by the time it reaches decision-makers. A quarterly report can leave a struggling project undetected for an entire season.

Monthly reporting aligned with billing cycles is the floor, not the goal. CFMA recommends monitoring KPIs like margin fade and job borrow daily or weekly in volatile conditions—and firms carrying multiple large active contracts should treat that as standard operating procedure, not the exception.

WIP on the Balance Sheet and Revenue Recognition

The Construction in Progress (CIP) Account

While a project is active, all job costs accumulate in the Construction in Progress (CIP) asset account on the balance sheet. When the project completes, these costs transfer to Cost of Goods Sold. This treatment keeps financial reporting consistent for long-duration contracts.

The CIP account is distinct from the WIP schedule—CIP is a ledger account, while the WIP schedule is a management report that drives revenue recognition calculations.

Revenue Recognition: Completed Contract vs. Percentage of Completion

| Method | How It Works | When It Applies |

|---|---|---|

| Completed Contract | Revenue and expenses recognized only at project close | Simple, short-duration contracts |

| Percentage of Completion | Revenue recognized proportionally as work advances | Most long-term construction contracts |

Under GAAP and ASC 606, percentage-of-completion style recognition isn't optional for most contractors—it follows from whether the performance obligation is satisfied over time. Wiss notes that most construction contracts qualify for over-time recognition because the customer controls the asset as it's created, or the contractor has an enforceable right to payment for work performed.

The WIP schedule is the mechanism that documents and supports this recognition on a job-by-job basis. Accurate WIP data is what keeps revenue recognition defensible during audits, bond renewals, and bank reviews.

That defensibility depends on how costs are tracked. Under RSM's ASC 606 guidance, cost-to-cost progress calculations must exclude costs that don't reflect actual performance—such as unexpected wasted materials or labor. Uninstalled materials may require a zero-margin adjustment, and imprecise cost tracking in either area creates direct audit exposure.

From Spreadsheets to Real-Time WIP: The Modern Approach

The Cost of the Monthly WIP Grind

The traditional WIP process looks something like this: finance teams spend 10–20 days pulling data from ERPs, project management systems, and field reports into a master spreadsheet, reconciling cost codes, fixing formula errors, and producing a report that's already outdated by the time it reaches leadership. Double L Management's Business Analyst described it plainly: "that one click replaced two weeks worth of prior work."

This isn't just a time burden. Decisions about staffing, billing, and resource allocation are being made on month-old data. That gap has a real cost—particularly on active jobs where margin is still recoverable if caught in time.

What Automated WIP Reporting Looks Like

That problem is solvable. Platforms like Datateer connect directly to construction ERPs—Procore, Sage, Vista, Acumatica, Foundation, CMiC, and others—to handle the entire data pipeline: extraction, cleaning, and standardization. The system maps cost codes, reconciles Procore project commits to Sage invoices, and populates dashboards without any manual work from the finance team.

Data refreshes overnight as standard, with more frequent updates available for firms that need tighter visibility. The result is a shared dashboard that both field and office teams can trust equally, replacing the Wednesday meeting where everyone stares at numbers that are already three weeks old.

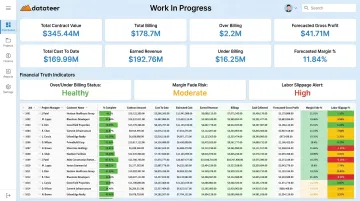

Datateer's WIP & Financial Truth dashboard surfaces:

- Automated over/underbilling calculations — updated without manual reconciliation

- Margin fade alerts — flagged while there's still time to act on active jobs

- Labor slippage — visible mid-week, not three weeks after payroll clears

What to Look for in a WIP Reporting Solution

When evaluating options, construction finance teams should prioritize:

- Direct ERP integration — not manual CSV exports that reintroduce human error

- Automated cost code standardization — mapping that works across multiple projects and systems without manual reconciliation

- Project-level and portfolio-level views — both in one place, accessible to finance, PMs, and executives

- Unlimited users — WIP visibility shouldn't stop at the accounting department; PMs and owners need it too

- Flat-rate pricing — per-seat models that penalize adoption don't serve firms where insight needs to flow across the organization

Datateer starts at $10,000/year per data source with unlimited users included. Data begins flowing during the 2–4 week setup window, before annual fees kick in. For firms running multiple systems, custom integrations are available beyond the standard 12-platform list.

Frequently Asked Questions

What is a WIP report in construction?

A WIP report is a financial document that tracks the status of all active jobs—showing costs incurred, work completed, earned revenue, and billing position for each contract. It gives contractors a view of project profitability before jobs close, rather than discovering problems at the end.

How often should a construction WIP report be updated?

Best practice is monthly at minimum, aligned with billing cycles. Firms managing multiple large contracts benefit from weekly or even daily visibility—CFMA specifically recommends that cadence in challenging market conditions—to catch cost overruns and billing gaps before they compound.

What is the difference between overbilling and underbilling in construction?

Overbilling occurs when invoiced amounts exceed earned revenue, creating a liability for work still owed. Underbilling means earned revenue exceeds what's been billed—a real asset but a cash flow gap. Both must be recorded on the balance sheet as contract liabilities and contract assets under ASC 606.

How is percentage of completion calculated in a WIP report?

Divide actual costs incurred to date by the total revised estimated cost to complete the project. That percentage, multiplied by the contract value, gives earned revenue to date. The method must be applied consistently across similar contracts under ASC 606.

What are the most common WIP report mistakes contractors make?

The top four: using percent of budget spent as a proxy for percent complete, failing to update estimated cost-to-complete when scope changes, not recording overbilling/underbilling adjustments on the balance sheet, and running reports too infrequently to catch problems while they're still fixable.

How does WIP relate to revenue recognition under GAAP?

Under GAAP and ASC 606, contractors with long-term contracts recognize revenue over time using percentage-of-completion logic. Revenue is earned as work progresses, not at project close. The WIP schedule tracks this recognition job by job and serves as the primary support document during audits and bond reviews.