Most contractors track margin closely. Fewer treat working capital management with the same discipline — and that gap has consequences. It shows up as constrained bonding capacity, reactive borrowing, and in the worst cases, insolvency on what looked like a healthy income statement.

This article covers three specific, measurable advantages of active working capital management in construction — and what gets lost when management is reactive or running on stale data.

Key Takeaways

- Working capital (current assets minus current liabilities) measures short-term financial cushion — construction's payment cycles make that cushion uniquely hard to maintain

- CFMA's 2025 Construction Financial Benchmarker reports an industry-average DSO of 55.2 days — firms routinely wait nearly two months to collect what they've already spent

- Surety bonding capacity is calculated as a direct multiple of working capital — meaning balance sheet strength determines which projects you're eligible to bid

- A firm can be profitable on paper and still become insolvent; working capital management is the early-warning system that prevents that outcome

- WIP reports that are 10–20 days old show where the business was, not where it stands today — making data lag a direct working capital risk

What Is Working Capital Management in Construction?

Working capital is straightforward to define: current assets (cash, accounts receivable, prepaid items) minus current liabilities (accounts payable, short-term debt, accrued expenses). The result is the net short-term cushion available to run the business day to day.

What makes construction different is how project-level variables distort that cushion in real time.

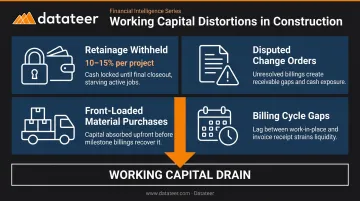

Four distortions show up on nearly every project:

- Retainage withheld by owners (typically 10–15% per project, per ASA guidance) sits on the balance sheet as a receivable but isn't accessible until project completion — sometimes months after closeout

- Disputed change orders tie up cash that's already been spent performing the work

- Front-loaded material purchases hit accounts payable before a single invoice goes out to the owner

- Billing cycle gaps mean cash doesn't flow when work is performed; it flows when paperwork clears

Working capital management in construction isn't bookkeeping. It's the ongoing discipline of monitoring, protecting, and optimizing the firm's liquidity position across all active projects — so leadership can make informed decisions about which contracts to pursue, what credit to carry, and how to allocate resources.

Key Advantages of Working Capital Management in Construction

These three advantages directly affect profitability, bonding capacity, and whether a firm catches financial problems before they become irreversible.

Cash Flow Stability Across the Project Lifecycle

Construction projects create a predictable cash flow mismatch. Mobilization costs, material purchases, subcontractor draws, and early-phase labor all hit the books before milestone billing kicks in. Owner payments then lag by weeks or months — sometimes tied to inspections, lien waiver processing, or retainage release schedules that extend well past substantial completion.

Active working capital management closes this gap — accounts receivable needs to function as an operational metric that finance teams track in real time:

- Invoice on schedule — billing delays directly extend DSO and widen the cash gap

- Monitor DSO weekly — the industry average per CFMA is 55.2 days; knowing where your firm sits relative to that number matters

- Track retainage balances by project — retainage release timing is one of the most predictable cash flow variables, and most firms don't model it forward

- Watch the cash conversion cycle — from work performed to cash collected, this cycle reveals how efficiently the firm converts its work into liquidity

The practical advantage: firms with real-time cash flow visibility can anticipate gaps weeks in advance and make deliberate financing decisions. Firms without it borrow reactively — drawing on credit lines to cover payroll when cash runs dry, at whatever rate the market offers. With the Federal Reserve's bank prime loan rate sitting at 6.75% as of June 2026, unplanned borrowing carries a real cost.

When this matters most: Large multi-phase projects with front-loaded costs; rapid growth periods when multiple projects create simultaneous cash float; owner payment terms of 60+ days.

KPIs to track: Days Sales Outstanding (DSO), cash conversion cycle, current ratio, net cash flow by project, retainage balance outstanding.

Bonding Capacity and Bid Competitiveness

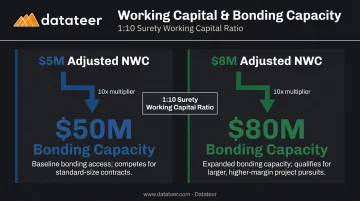

Surety underwriters don't just review revenue. They look at working capital first — because bonding capacity is calculated as a direct multiple of it. NASBP guidance indicates sureties typically require working capital equal to roughly 10% of the requested bonding program — meaning approximately $1 of working capital supports $10 of bonding capacity.

The second factor matters just as much: sureties adjust working capital downward during underwriting. Receivables aged beyond 90 days, prepaid expenses, and disputed balances may be excluded or discounted. A firm's "real" bondable working capital is often substantially lower than what appears on the balance sheet — and only disciplined working capital management produces the clean position sureties want to see.

Two practical consequences follow from this:

Firms that actively build working capital can target specific bonding thresholds. Moving from a $5M adjusted net working capital position to $8M isn't just a balance sheet improvement — it's the difference between being eligible for $50M single projects versus $80M, unlocking contract sizes competitors with weaker balance sheets cannot pursue.

Over-leveraged firms price themselves out of competitive bids. A highly leveraged firm carries short-term debt servicing costs in its overhead rate, making bids structurally more expensive than a well-capitalized competitor bidding on identical work. In margin-compressed markets, that difference often exceeds the margin itself.

When this matters most: Growth phases where firms are moving into larger contract sizes; competitive bidding environments with thin margins; periods of rising interest rates when the penalty for over-leverage grows.

KPIs to track: Adjusted working capital, current ratio, debt-to-equity ratio, bonding capacity headroom, bid-to-win ratio on larger projects.

Early Detection of Project-Level Liquidity Risk

The income statement shows profit. The backlog looks strong. The firm is technically insolvent. This happens when retainage is tied up, receivables are aging, disputed extras drain reserves, and no one tracks the aggregate working capital position across projects.

The problem doesn't announce itself on the income statement. It surfaces as working capital erosion — first at the project level, then in aggregate.

Active WCM creates an early-warning system by treating WIP schedules as a liquidity tool, not just an accounting requirement:

- Underbilling (costs incurred ahead of billing) reduces current assets and is a direct working capital drain — CFMA notes this may also indicate payment issues or inaccurate completion estimates

- Retainage aging by project shows which balances are approaching release versus which are stalled — a distinction that changes the liquidity picture materially

- WIP gain/fade analysis performed at least monthly, as both CMAA and NASBP guidance recommend, catches margin deterioration while the project is still correctable

Manual WIP reporting makes this worse. When reports take 10–20 days to produce, leadership is always working from an outdated financial picture. Double L Management, a Datateer customer, noted that the first time they accessed their data through automated dashboards, "that one click replaced two weeks worth of prior work." That two-week lag — compressed to overnight — represents the difference between catching a problem and discovering the damage.

When this matters most: Firms running multiple concurrent projects; rapid growth phases where project volume outpaces financial oversight; cost-volatile markets where material and labor inflation creates unexpected overruns.

KPIs to track: WIP overbilling/underbilling balance, retainage aging, gross margin by project versus budget, net working capital trend over rolling 90 days.

What Happens When Working Capital Management Is Ignored

The consequences build quietly before they become obvious.

On their own, none of these look alarming:

- A slow billing cycle extends DSO by a week

- A disputed change order sits unresolved for 60 days

- Retainage on three completed projects hasn't been chased

- One project runs over budget without triggering a formal review

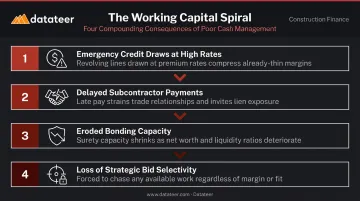

Together, they produce a working capital position that no longer supports the firm's operational needs. The downstream effects compound quickly:

- Cash shortfalls force emergency credit draws at unfavorable rates

- Delayed subcontractor payments damage relationships and slow project execution

- Bonding capacity erodes just as the firm is trying to bid larger work

- Leadership loses the ability to make selective bidding decisions — every contract starts to look necessary rather than strategic

The long-term BLS data on construction establishment survival is sobering: of establishments born in March 1994, only 10.3% remained operating by March 2025. Early-stage attrition is steep — survival rates fall below 51% by the fourth year. Working capital discipline won't prevent every bad project or downturn — but without it, firms have no buffer when one inevitably arrives.

How to Get the Most Value from Working Capital Management

Working capital management is most valuable as an ongoing discipline, not a quarterly review. That means:

- Billing cycles tight and consistent: invoice on schedule, every project, every period

- AR aging reviewed weekly — not monthly, not at quarter-end

- Retainage balances tracked by project, with expected release dates modeled into cash flow forecasts

- Current ratio monitored monthly against industry benchmarks; CFMA's 2025 data shows the industry average at 1.7, with a healthy range typically considered between 1.2 and 2.0

The quality of that discipline depends entirely on data quality. Firms producing WIP reports and working capital summaries through manual spreadsheet processes are working with a structural lag — decisions get made on where the business was, not where it is.

Datateer's construction finance dashboards address this directly. The platform syncs overnight from 12+ construction ERPs — Sage, Viewpoint Vista, Procore, Acumatica, and others — and surfaces WIP schedules, AR and AP aging, retainage tracking, DSO, cash conversion cycle, and 13-week liquidity forecasting without manual assembly.

Three dashboards do the core work:

- AR & AP Health tracks DSO against live receivables data

- Cash Conversion & Velocity identifies exactly where cash is stalling

- Job-Level Cash Flow shows which projects are generating liquidity and which ones are consuming it

Implementation runs 2–4 weeks, with data flowing before annual fees begin.

The goal isn't just visibility — it's using that visibility to make forward-looking decisions: which projects to bid, when to draw on credit, when to pass on a contract the firm doesn't have the capital to float.

Conclusion

Working capital management in construction determines bonding capacity, cash flow resilience, bid competitiveness, and a firm's ability to absorb project setbacks without becoming insolvent. It's an active discipline with compounding returns. Firms that manage working capital consistently build the balance sheet strength to pursue larger work, borrow on better terms, and grow from a position of financial clarity rather than uncertainty.

The firms most vulnerable to working capital surprises aren't necessarily the ones with the worst margins. They're the ones making decisions on stale data. That's the problem worth solving first — and it's a solvable one. Platforms like Datateer automate the data flow from construction ERPs into real-time working capital dashboards, so finance teams are always working from current numbers rather than last month's spreadsheet.

Frequently Asked Questions

What are the key elements of working capital management in the construction industry?

The core elements are accounts receivable management (billing speed and collections), retainage tracking by project, accounts payable discipline, WIP schedule monitoring, and short-term debt management — all measured against cash flow projections at both the project level and in aggregate.

In the construction industry, is it better to have high or low net working capital?

Higher NWC is generally better — it increases bonding capacity, reduces reliance on expensive short-term credit, and buffers against project losses or delayed payments. That said, the goal is sufficient, well-managed liquidity: excess idle capital can signal underdeployment of available resources.

What is net working capital (NWC) and how does it differ from working capital (WC)?

Working capital typically refers to the ratio (current assets ÷ current liabilities), while net working capital is the dollar difference (current assets minus current liabilities). In construction, NWC is particularly significant because sureties and lenders use adjusted NWC — excluding hard-to-liquidate assets — as the basis for bonding and credit decisions.

What is a good working capital ratio for a construction company?

A current ratio of 1.2 to 2.0 is the accepted healthy range, with CFMA's 2025 benchmark at 1.7. The right target depends on project complexity, revenue scale, and growth stage — sureties need a ratio and NWC position that supports the firm's desired bonding capacity at the standard ~10x multiple.

How does WIP affect working capital in construction?

WIP overbilling (billing ahead of costs incurred) temporarily inflates working capital; underbilling (costs incurred ahead of billing) reduces it. An inaccurate or delayed WIP schedule can make a firm's working capital look healthier or weaker than it actually is, distorting both internal decisions and external reviews by lenders or sureties.

What are the most common causes of working capital shortages in construction?

The primary culprits: slow owner payments extending DSO, retainage withheld for extended periods, disputed change orders tying up receivables, project cost overruns consuming more cash than budgeted, and excessive project load outpacing the available capital to float combined upfront costs.