Introduction

Retainage is often the contractor's entire profit margin sitting in limbo. On a project with a 5% net margin, a 5–10% retainage hold means you've already earned more in withheld funds than you'll clear as profit — yet that money won't arrive for months, sometimes over a year.

The accounting challenge compounds this. Retainage behaves differently from standard accounts receivable. It requires separate balance sheet treatment, specific classification rules under ASC 606, and simultaneous tracking at both the receivable and payable level. Miss any of these, and you're operating with distorted WIP reports, inaccurate cash flow forecasts, and real compliance exposure.

According to CFMA's 2025 Financial Benchmarker, the average pre-tax margin for construction companies in 2024 was 6.7% — which means a standard 10% retainage hold on any given project exceeds that margin entirely. Getting retainage accounting wrong doesn't just create reporting headaches — it distorts every financial decision made while that money is outstanding.

This guide covers how to record retainage journal entries, where it belongs on the balance sheet, the ASC 606 contract asset versus receivable distinction, common accounting pitfalls, and management best practices.

Key Takeaways

- Retainage (typically 5–10% of each progress payment) must be tracked separately from regular AR in both the AR and AP ledgers.

- Under ASC 606, retainage is a receivable only when the right to payment is unconditional; if conditions remain, it's a contract asset.

- Misclassifying retainage distorts working capital ratios, WIP schedules, and bonding capacity.

- State Prompt Payment Laws regulate retainage release timelines and vary significantly by state.

- Automated ERP-integrated retainage tracking eliminates the 10–20 day reconciliation lag that manual spreadsheet processes consistently produce.

Why Retainage Accounting Matters for Construction Finance

The Margin Problem

Retainage is a margin problem before it's a cash problem. On a $2M project at 10% retainage, $200,000 of earned money sits withheld. If that firm operates at CFMA's 2024 industry average pre-tax margin of 6.7%, their expected profit on that job is roughly $134,000 — less than the retainage hold.

That gap has a practical consequence: you can't tell whether a job was actually profitable until retainage comes in. By then, it's too late to course-correct.

The Cash Flow Illusion

Standard accounts receivable accounting doesn't capture retainage accurately. If retainage is lumped into general AR, your balance sheet shows liquidity you can't access. Cash flow forecasts built on that number are optimistic in a way that creates real operational risk — you look solvent on paper while struggling to fund the next mobilization.

The Compliance Dimension

Three compliance frameworks intersect on retainage:

- ASC 606 (Topic 606) — the FASB revenue recognition standard determining whether retainage appears as a receivable or a contract asset on your balance sheet

- State Prompt Payment Laws — statutes in every state specifying when retainage must be released and flow down to subcontractors, with varying timelines and penalty exposure

- Lien and retainage bond statutes — state-specific rules that govern a subcontractor's right to lien for withheld amounts, triggered when upstream parties miss release deadlines

Getting the ASC 606 classification wrong creates audit risk. Getting the Prompt Payment side wrong creates lien exposure.

How to Account for Construction Retainage

The foundational rule: the full earned amount is recognized as revenue, but the cash received and the retainage held back are recorded in separate accounts.

Retainage Receivable (Owner Withholds from GC)

When you submit a progress billing, the journal entry separates the withheld portion immediately:

Example: $50,000 progress billing at 10% retainage

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable | $45,000 | |

| Retainage Receivable | $5,000 | |

| Revenue Earned | $50,000 |

The $5,000 retainage goes to a dedicated Retainage Receivable account — not regular AR. This keeps earned-but-unpaid retainage visible, prevents it from inflating apparent current receivables, and makes it trackable at the project level.

When the owner releases retainage at substantial completion:

| Account | Debit | Credit |

|---|---|---|

| Cash (or AR) | $5,000 | |

| Retainage Receivable | $5,000 |

AP Retainage (GC Withholds from Subcontractors)

The mirror image applies on the payable side. When paying a subcontractor's progress billing, the withheld amount is credited to Retainage Payable — not accounts payable:

| Account | Debit | Credit |

|---|---|---|

| Subcontract Expense | $40,000 | |

| Accounts Payable | $36,000 | |

| Retainage Payable | $4,000 |

One important note: GCs who withhold retainage from subs at a higher rate than the owner withholds from them are creating legal exposure in many states. The flow-down must align.

Contract Asset Treatment Under ASC 606

The FASB Staff Educational Paper published in April 2025 clarifies the distinction that trips up most construction accountants:

| Classification | Right to Payment | Common Trigger |

|---|---|---|

| Retainage Receivable | Unconditional — no further performance conditions remain | Time elapses to payment date |

| Contract Asset | Conditional — future performance still required | Inspection sign-off, punch list completion, milestone reached |

This analysis must be done contract-by-contract. The same project can shift from contract asset to receivable as performance conditions are satisfied. An inspection sign-off that clears the final condition reclassifies that retainage balance from contract asset to receivable — and the journal entry must reflect that shift.

Where Does Retainage Go on the Balance Sheet?

Retainage Receivable: Current vs. Long-Term Asset

Unconditional retainage receivable is presented as a separate line item — not buried in general AR. Classification follows standard current/noncurrent rules:

- Current assets: Retainage expected within 12 months

- Long-term assets: Retainage on multi-year projects expected after one year

FASB's April 2025 guidance requires disclosure of the specific amounts expected after one year and the projected collection timeline. This isn't optional footnote material — it's a required disclosure for construction contractors.

Contract Asset vs. Receivable: The Critical Distinction

When retainage depends on future performance, it belongs within contract balances on the balance sheet, not as a standalone receivable. Per ASC 606, a single contract cannot simultaneously show both a contract asset and a contract liability — they must be netted.

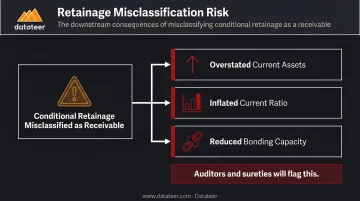

Mislabeling conditional retainage as a receivable:

- Overstates current assets

- Inflates the current ratio

- Misleads lenders, sureties, and bonding agents about actual financial health

Sureties underwrite bonding capacity based on working capital ratios. An inflated current ratio from misclassified retainage directly reduces that capacity — and auditors will catch it.

AP Retainage: Liability Presentation

The liability side deserves the same precision. Retainage payable to subcontractors belongs in current liabilities as a separate line item from accounts payable. Presenting it within general AP:

- Understates payment obligations to subs

- Obscures the symmetry between AR retainage and AP retainage

- Creates a reconciliation problem that auditors and sureties will flag

Disclosure Requirements Under ASC 606

Required disclosures under Topic 606 include:

- Opening and closing balances of receivables and contract assets

- Revenue recognized from prior-period contract liabilities

- Explanation of significant changes in contract balances

FASB also permits voluntary supplemental disclosures — parenthetical notes showing retainage embedded in contract asset balances, or use of terms like "billings in excess" or "revenue in excess of billings" — to improve clarity for financial statement users.

Common Retainage Accounting Challenges

Multi-Project Tracking Complexity

Tracking retainage balances, release conditions, and collection timelines across dozens of concurrent projects in spreadsheets creates compounding problems. Version control failures, reconciliation errors, and reporting lags leave finance teams working from stale data.

The construction industry's data quality problem is well documented: research from Autodesk and FMI found that 30% of respondents said more than half of their project data was inaccurate or inaccessible, with decisions based on bad data accounting for $88.69 billion in rework in a single year.

Retainage is particularly vulnerable to data quality failures because it's a long-tail obligation — balances accumulate across many projects, release conditions vary by contract, and the reconciliation never fully closes until a project reaches substantial completion.

Purpose-built platforms like Datateer address this directly by syncing AR and AP retainage data from construction ERPs (Procore, Sage, Viewpoint, Acumatica, and others) at the project level — giving finance teams a single reconciled view rather than a patchwork of spreadsheet exports.

WIP Schedule Distortion

When retainage isn't properly separated from billed AR, the billings side of the over/under billing calculation becomes inaccurate. The WIP schedule shows distorted overbilling or underbilling positions that don't reflect reality — and those errors don't surface until project closeout, when it's far too late to act on them.

Accurate WIP reporting requires clean retainage separation upstream. The AICPA's guidance on WIP schedules confirms that WIP schedules support revenue recognition by comparing contract costs, recognized revenue, and billings — a comparison that only works correctly when retainage is classified properly.

Subcontractor Retainage Misalignment

GCs face two distinct legal risks on the AP retainage side:

- Withholding from subs at a higher rate than the owner withholds from the GC — permissible in some states, legally risky in others

- Delaying sub retainage release after receiving payment from the owner — violates Prompt Payment Laws in most states

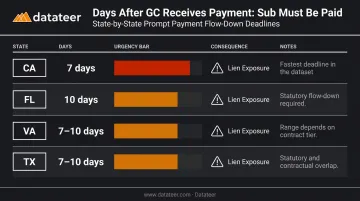

State flow-down timelines are specific and short. California requires subs to receive their retainage share within 7 days of the contractor receiving it. Florida requires payment within 10 days. Virginia and Texas require payment within 7–10 days depending on contract type. These aren't grace periods — they're hard deadlines with lien exposure attached.

Release Trigger Disputes and Lien Risk

Ambiguous "substantial completion" language in contracts creates disputes that can delay retainage release by months. Meanwhile, mechanic's lien deadlines often run from the date of completion or last work performed — not from when retainage is legally due.

A contractor without precise completion documentation faces two compounding risks:

- Closed lien window: The filing deadline passes before the retainage dispute is resolved, eliminating legal recourse

- Unenforceable claims: Without documented milestones, the contractor can't prove substantial completion occurred — leaving the owner in a stronger negotiating position

Treating completion documentation as a legal protection measure — not just an administrative task — is how contractors keep their lien rights intact through disputes.

Best Practices for Construction Retainage Management

Contract Clarity and Legal Foundations

Before work begins, every contract should explicitly define:

- Retainage percentage and applicable caps

- Specific release conditions and milestone criteria

- Definition of "substantial completion" with objective, measurable benchmarks

- Dispute resolution mechanisms for contested completion claims

- State Prompt Payment Law compliance provisions

Two provisions deliver the highest leverage at contract stage: milestone-based retainage reductions (many contracts allow reduction after 50% completion) and explicit Prompt Payment Law compliance language that establishes the release timeline upfront rather than leaving it to negotiation at closeout.

According to ConsensusDocs, retainage rates and release terms vary significantly by state — some states impose caps (California and Florida cap public retainage at 5%), while others allow up to 10% until the 50% completion threshold is reached.

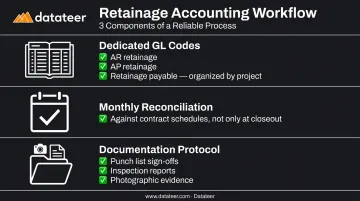

Accounting Workflow and Documentation Standards

A reliable retainage accounting workflow requires:

- Dedicated GL codes — separate accounts for AR retainage, AP retainage, and retainage payable, organized by project

- Monthly reconciliation against contract schedules, not just at closeout

- Documentation protocol — punch list sign-offs, inspection reports, and photographic evidence assembled before any retainage release request is submitted

The documentation protocol matters as much as the accounting setup. An audit-ready paper trail that connects each retainage release to a specific completion milestone eliminates disputes and accelerates payment. Without it, you're negotiating from memory.

Technology Integration for Real-Time Retainage Oversight

Retainage tracking belongs inside your ERP and financial reporting system — not in a spreadsheet that someone owns, updates manually, and emails around. The consequences of spreadsheet-based retainage management show up at month-end close, when finance teams spend days reconciling balances that an integrated system would surface instantly.

That same documentation discipline breaks down fast when retainage data lives across disconnected spreadsheets. Integrated platforms close that gap by automating what manual workflows can't sustain at scale.

Datateer's retainage analytics track AR and AP retainage simultaneously across all projects, monitor release schedules, and feed projected retainage collections directly into 13-week cash flow forecasting. Overdue retainage releases are flagged automatically, surfacing cash flow risks before they reach the close meeting. The platform starts at $10,000/year per data source with unlimited users, and implementation takes 2–4 weeks.

Firms still running retainage in spreadsheets typically find the real cost in three places: delayed releases no one caught, reconciliation hours at month-end, and cash flow forecasts missing the retainage line entirely.

Conclusion

Correct ASC 606 classification, accurate balance sheet presentation, and real-time retainage tracking aren't optional refinements — banks, sureties, and auditors treat them as table stakes for any firm seeking favorable terms or bonding capacity.

Firms that get this right gain a concrete advantage: credible WIP schedules, accurate bonding capacity, healthier subcontractor relationships, and finance leadership that can act strategically rather than reactively. The CFO who can tell a surety exactly how much retainage is outstanding, when it's expected, and what conditions govern release is in a fundamentally different position than one who estimates.

As project scale and complexity increase, the gap between firms using manual retainage processes and those using integrated systems will only widen. Platforms purpose-built for construction — like Datateer's Retainage Tracking module, which surfaces A/R retainage, A/P retainage, and release schedules in a single view — make that shift practical without a months-long implementation. Starting before a dispute forces the issue is almost always cheaper than scrambling after one does.

Frequently Asked Questions

How do you account for construction retainage?

At each progress billing, the withheld amount is debited to a separate "Retainage Receivable" account rather than regular AR. On the payable side, amounts withheld from subcontractors are credited to "Retainage Payable." Revenue is recognized on the full earned amount; only the cash receipt is deferred until release conditions are met.

Where does retainage go on a balance sheet?

Unconditional retainage (where only time separates the contractor from payment) is presented as a separate receivable: current if collectible within 12 months, long-term if beyond. Conditional retainage (still dependent on future performance) belongs within contract asset balances, not as a standalone receivable.

What is the difference between a retainage receivable and a contract asset?

A retainage receivable reflects an unconditional right to payment, meaning nothing remains to perform beyond waiting for time to pass. A contract asset means the right to payment depends on completing remaining performance obligations. The FASB's April 2025 educational paper under ASC 606 clarifies this distinction for construction contractors.

What is the typical retainage percentage in construction?

Retainage most commonly ranges from 5% to 10% of each progress payment. Some states cap public project retainage at 5% (California, Florida), while others allow up to 10% with reductions permitted after 50% completion. Private contracts vary based on negotiated terms.

When does retainage get released in construction?

Retainage is typically released upon substantial completion — when the work is sufficiently complete for the owner to occupy or use the project for its intended purpose, per AIA standards. State Prompt Payment Laws govern release timelines, ranging from 7 days (flow-down to subs) to 60 days (public project release) depending on the state.

How does retainage affect cash flow for subcontractors?

Subcontractors often finish their scope months before overall project completion, yet must wait for the entire project to close before receiving retainage. The result: they fund 100% of costs while collecting only 90–95% of earned revenue for an extended period, a liquidity squeeze that hits smaller specialty subs hardest.