The insidious part: fade rarely hits all at once. A few labor hours over per phase, one material price absorbed without rebidding, a change order performed on a handshake — individually, none of these feel like emergencies. Collectively, they erode the margin you bid before anyone realizes what's happening.

This article examines how margin fade accumulates, what drives it at each stage, and three categories of strategies to stop it: decisions made before work starts, controls applied during execution, and the data systems that determine how fast your finance team can see the problem coming.

Key Takeaways

- Margin fade is the gap between estimated profit at bid and actual profit at close — it builds gradually, not all at once

- Root causes span three layers: decision-time errors, execution-time control failures, and visibility delays

- Catching a variance in week two costs far less than managing an overrun at close-out

- Weekly job cost reviews and real-time WIP visibility are the most direct levers for catching execution fade early

- Process discipline prevents fade — waiting to correct it after close costs far more

How Profit Margin Fade Builds Up

Fade doesn't announce itself. It accumulates as a series of small variances — a few extra labor hours per phase, one untracked scope addition, a material price increase absorbed without rebidding. Each one seems manageable. Compounded across a project's full duration, they're not.

The Visibility Gap

The real problem isn't just that variances occur. It's that they go undetected long enough to multiply.

Most construction firms operate on reporting cycles that lag actual costs by weeks. By the time finance sees the numbers, the crew has moved three phases forward. PlanGrid and FMI's research found that poor project data and miscommunication caused $31.3 billion in US rework annually — nearly half of all US rework volume. That figure reflects what delayed, unreliable data actually costs when compounded across thousands of projects.

The delay between cost incurrence and cost visibility is where manageable variances become entrenched overruns.

A Management Problem, Not an Industry Inevitability

Some fade originates from unpredictable events — weather, supply chain disruption, owner-driven scope shifts. That portion is genuinely hard to prevent.

A substantial share, however, originates from correctable process gaps:

- Estimates built on gut feel rather than historical cost data

- Change orders documented after the fact — or not at all

- Reporting cycles too slow to catch overruns before they compound

That portion is a management outcome. Firms that recognize the difference between uncontrollable events and fixable process failures are the ones that actually close the gap.

Key Drivers of Profit Margin Fade

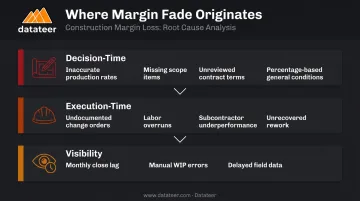

Fade originates at three distinct stages: decision-time errors, execution failures, and visibility gaps. Addressing only one while the others remain intact won't stop the bleed.

Decision-Time Drivers

These are errors made before work starts — problems locked into the estimate:

- Inaccurate production rates built from gut feel rather than actual cost history

- Missing scope items in the estimate that get absorbed as costs during execution

- Contract terms not reviewed before signing — retention percentages, liquidated damages clauses, allowable change order markups, and delay provisions each represent predictable margin leaks that take effect at contract execution

- General conditions calculated as a percentage adder rather than a line-item build-up, which regularly underestimates costs on longer or more complex jobs

Execution-Time Drivers

These emerge during the project, often from weak controls:

- Change orders performed without written documentation or approval

- Labor hours running over budget without triggering a formal review

- Subcontractor underperformance absorbed into the GC's margin rather than addressed contractually

- Rework costs that never get billed back to the responsible party

FMI's 2023 Labor Productivity Study found that US contractors lose roughly $30–$40 billion annually to labor inefficiencies — and that a 6% improvement in labor productivity can produce a 50% average increase in profitability. Labor is where execution fade hits hardest.

Visibility Drivers

These are structural conditions that prevent early detection:

- Monthly close cycles that make last week's variances invisible until next month

- Manually assembled WIP schedules that introduce transcription errors and version conflicts

- Field data that never reaches the finance team in time to act

The CFMA's 2025 Construction Financial Benchmarker shows a typical net income before tax margin of 6.7% for construction firms, with Best in Class reaching 12.0%. At those margins, a variance of even a few percentage points on a mid-size project is material. By the time a monthly close surfaces a problem, the window to correct it has often already closed.

Strategies to Stop Profit Margin Fade

Fade rarely has a single cause, so strategies need to address all three layers where it originates.

Strategies That Change Decisions Before Work Starts

Build estimates from actual company cost history. Industry benchmarks tell you what the average contractor experiences. Your historical data tells you what you experience — your crews, your markets, your typical job types. Establish a post-job review discipline that feeds final labor hours, crew production rates, and materials usage back into a living database. The next bid you build from that data will carry less risk of underbidding than one built from general industry rates.

Review contract terms before signing — every clause. Payment terms, allowable change order markups, retention percentages, delay clauses, and liquidated damages are not boilerplate. Each overlooked clause is a margin leak that begins the moment work starts. This review isn't legal overhead; it's financial due diligence.

Define subcontractor scope at the line-item level. Coverage gaps in subcontractor agreements create costs the GC absorbs by default. Who installs backing for handrails? Who provides and installs off-site utility conduit? Who handles temporary erosion controls if the site conditions change? These aren't edge cases — they're the exact questions that produce surprise costs mid-project when the answer defaults to "the GC."

Build general conditions from a line-item build-up. Actual supervision hours, vehicle costs, temporary facilities, and project duration — priced individually, not applied as a blanket percentage. Percentage adders consistently underestimate GC costs on longer or more complex jobs.

Strategies That Improve Execution Controls

Implement weekly job cost reviews. Waiting for monthly financials allows variances to compound unchecked for four or more weeks. PM accountability for weekly cost-to-complete reviews is the most direct lever for catching execution fade early — before the next phase absorbs the same overrun pattern.

Enforce a formal change order workflow. No additional work starts until it's documented, priced, and approved in writing. This isn't administrative overhead; it's margin protection. Verbal approvals and after-the-fact documentation are where recoverable revenue routinely goes uncollected.

Set crew production goals before mobilization — and track them weekly. Bring the estimator, project manager, and field foreman together before the job starts to confirm budgeted hours by phase. This meeting converts the estimate from an office document into a shared field target. When a foreman knows the budget and owns accountability for it, overruns surface faster.

Monitor cost-to-complete, percent complete, and over/under billing across all active jobs in real time. Datateer's WIP and Job Costing dashboards eliminate the 10–20 day reporting lag by syncing directly to ERP data, giving finance managers live visibility into which jobs are fading while there's still time to adjust crew plans, rebid subcontractors, or accelerate billing.

"That one click replaced two weeks worth of prior work." — Business Analyst, Double L Management

Strategies That Change the Data Environment

Eliminate the ERP-to-reporting lag. Manual Excel-based WIP processes introduce transcription errors, version conflicts, and multi-day delays. These aren't minor inefficiencies. They're the structural reason why close-out surprises keep happening. The root cause of most "surprises" isn't a field problem. It's a data flow problem.

Datateer's direct ERP integration handles automatic reconciliation of Procore project commits to Sage invoices, standardizes cost codes across systems, and catches malformed entries before they reach the dashboard. Reports reflect what's actually happening on the job — not what happened three weeks ago.

Build financial literacy into the project management role. A PM who can read a job cost report, interpret percent complete, and flag over/under billing catches execution issues at the source rather than waiting for finance to surface them weeks later. Datateer's Job Costing & Cost-to-Complete dashboard gives PMs exactly that visibility, showing:

- Actual costs incurred and committed costs

- Pending change orders and projected final cost

- Budget variance at the job, phase, and cost-code level

The PM Scorecard module extends this further, presenting budget variance, margin variance, change order win rate, and earned-value metrics in a format built for project managers, not accountants.

Conduct structured post-job reviews for every completed project. Analyze estimated versus actual costs by category: labor, materials, subcontractors, general conditions. Look for patterns — which job types, clients, or site conditions consistently produce fade? Feed those findings back into future bids. Over time, bid accuracy improves — not because estimators get smarter, but because the data does.

Conclusion

Stopping margin fade requires knowing where it originates — in the decision layer, the execution layer, or the visibility layer — and applying targeted strategies at each point. Generic cost-cutting rarely solves it.

Lasting margin protection combines stronger decisions before projects start, tighter controls during execution, and a data infrastructure that connects field costs to finance fast enough to act. That last piece is where most firms fall short: the data exists inside their ERP, but it's locked in reporting cycles that are weeks too slow to change outcomes. Platforms like Datateer's Margin Protection analytics pull that data out of the ERP automatically, surfacing job-level fade signals while there's still time to act — not after the project closes.

Frequently Asked Questions

What is margin fade?

Margin fade is the negative variance between a project's estimated profit margin at bid and the actual margin realized at completion. It typically accumulates gradually through multiple small cost overruns — untracked labor hours, absorbed scope gaps, uncollected change orders — rather than one large event.

What is an example of margin fade in construction?

A contractor bids a project expecting a 15% gross margin. Rising material costs, a handful of change orders performed on verbal approval, and labor running 8% over budget bring final costs in higher than estimated — leaving a realized margin of 9%. That 6-point gap is margin fade.

What are the most common causes of profit margin fade in construction?

The most common causes include:

- Inaccurate estimates built on outdated production rates

- Change orders performed without written approval

- Labor hours running over budget without triggering a review

- Delayed financial reporting that prevents corrective action

How does delayed financial reporting contribute to margin fade?

When cost data arrives weeks after costs are incurred, small variances compound into larger overruns before anyone sees them. By the time the numbers surface, the window for corrective action has already closed.

Can profit margin fade be prevented entirely?

Some variance is inherent in construction and can't be eliminated. Most margin fade — the kind driven by estimating errors, unmanaged change orders, and reporting lag — is preventable with consistent process discipline and real-time financial visibility.

How often should construction companies review job cost reports?

Weekly at minimum for active projects, with real-time dashboard access between reviews. Monthly reporting cycles are too slow — by the time the numbers arrive, four or more weeks of compounding variance have already occurred.