Overbilling — formally called billings in excess of costs — sits at the center of that strategy. It's a common, recognized accounting practice where invoices temporarily outpace the value of work completed. Done deliberately and tracked carefully, it keeps cash flowing. Left unmonitored, it masks missing costs, distorts financial statements, and can quietly erode margins by the time anyone notices.

This article explains what overbilling is, how to calculate it, what causes it, and how to manage it without letting it become a liability in more ways than one.

Key Takeaways

- Billings in excess of costs arise when invoiced amounts exceed earned revenue based on project completion, recorded as a current liability on the balance sheet

- Overbilling is a legitimate cash flow tool, not inherently fraudulent, but requires disciplined tracking to prevent profit fade and financial misstatement

- The most common causes are advance billing, unrecognized cost savings, unapproved change orders, and missing subcontractor accruals

- Accurate cost-to-complete estimates are the single most important input — outdated estimates corrupt the entire WIP calculation

- Real-time WIP dashboards shift overbilling monitoring from a month-end forensic exercise to active, ongoing financial management

What Is Overbilling in Construction?

Overbilling occurs when the total amount invoiced to a client exceeds the earned revenue based on actual project completion to date. Under the percentage-of-completion method, revenue is recognized in proportion to how much work has been finished — not when invoices are sent. When billing outpaces that progress, the excess sits on the balance sheet as a liability until the underlying work catches up.

This is also called billings in excess of costs, and it's a standard accounting concept in construction. It is not the same as fraudulent overcharging. Legitimate overbilling results from billing timing — advance invoicing, front-loaded schedules of values, or mobilization deposits. Fraud, by contrast, involves deliberately misrepresenting project progress or billing for work never performed.

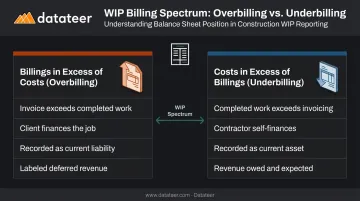

Billings in Excess of Costs vs. Costs in Excess of Billings

These are the two sides of the WIP equation:

- Billings in excess of costs (overbilling): The contractor has invoiced ahead of work completed. The client is effectively financing the job. Recorded as a current liability.

- Costs in excess of billings (underbilling): The contractor has completed more work than invoiced. The contractor is self-financing the job. Recorded as a current asset because the revenue is owed and expected soon.

According to Surety Bond Quarterly, large variances in either direction can signal problems that jeopardize a contractor's bond program. Sureties often prefer some overbilling — it suggests the project is self-financing — but excessive amounts prompt scrutiny. Underbillings raise different concerns: billing delays, cost overruns, or profit fade.

How Overbilling Is Recorded on the Balance Sheet

Under FASB ASC 606, when an entity has an unconditional right to consideration before transferring goods or services, the contract is presented as a contract liability. In construction, this is billings in excess of costs — often labeled "deferred revenue" on the balance sheet.

The contractor has collected (or invoiced) money for work not yet completed — that money isn't recognized income yet, it's an obligation to perform.

Costs in excess of billings sit on the opposite side as a current asset. Misclassifying either line item produces materially inaccurate financial statements that can mislead:

- Bonding companies evaluating contractor capacity

- Lenders assessing creditworthiness

- Other stakeholders relying on those numbers for decisions

How to Calculate Billings in Excess of Costs

The calculation uses the cost-to-cost method to determine percentage of completion, then measures actual billings against earned revenue. Run this for every open project — a company can appear balanced in aggregate while individual jobs are significantly off.

The Four-Step Formula

Step 1: Total cost estimate The total anticipated cost to complete the project, start to finish. This is the number every downstream calculation depends on — get it wrong here and everything else is off.

Step 2: Percent complete

Costs Incurred to Date ÷ Total Cost Estimate = Percent Complete

Step 3: Earned revenue

Percent Complete × Total Contract Amount = Earned Revenue

Step 4: Billings in excess of costs

Total Amount Billed − Earned Revenue = Result

- Positive result = Billings in Excess of Costs (current liability)

- Negative result = Costs in Excess of Billings (current asset)

Worked Example

A contractor is on a $1,000,000 contract. Total cost estimate is $700,000, and $490,000 in costs have been incurred to date.

| Input | Value |

|---|---|

| Total Cost Estimate | $700,000 |

| Costs Incurred to Date | $490,000 |

| Percent Complete | 70% |

| Earned Revenue (70% × $1,000,000) | $700,000 |

| Total Billed | $790,000 |

| Billings in Excess of Costs | $90,000 |

That $90,000 is a current liability — the contractor has collected more than the work completed to date justifies.

Why the Cost Estimate Is the Critical Variable

EisnerAmper notes that accurate estimated costs and contract prices are the two inputs driving the entire WIP schedule. An artificially high or outdated estimate distorts every downstream calculation. A project that looks 60% complete based on a stale estimate might actually be 75% complete — hiding an overbilling problem entirely.

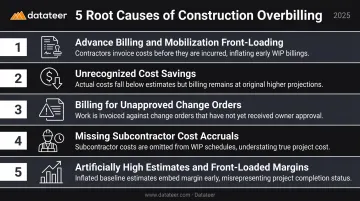

Common Causes of Overbilling in Construction

Most overbilling incidents trace back to one of five root causes — and each one is preventable once you know where to look.

Advance billing and mobilization front-loading. Billing mobilization costs or initial deposits before those costs are incurred is contractually common, but it creates an immediate overbilling position that must be tracked as the project progresses.

Unrecognized cost savings. When actual costs come in below estimate but billing still reflects original rates, the gap becomes an overbilling. If pipe installation was estimated at $75/foot but ran $62/foot, billing at the higher rate creates an unintended discrepancy. Update cost estimates as soon as savings are confirmed — but not prematurely.

Billing for unapproved change orders. EisnerAmper notes that contractors often begin out-of-scope work before a change order is approved to keep projects moving. Billing for that work before authorization creates a gap between what the contract permits and what's been invoiced. Unapproved change orders should be treated as claims, not billable revenue.

Missing subcontractor cost accruals. GCs frequently bill clients for subcontractor work before the sub's invoice has been received and entered. When those costs are absent from the system, the job looks more profitable than it is — a position that corrects itself only when the invoice arrives. Month-end accruals close this gap before it distorts WIP reports.

Artificially high estimates and front-loaded margins. Projects estimated conservatively to buffer against risk — or with high-margin mobilization line items — generate billings that exceed actual costs incurred early in the job. This effect is most pronounced when those line items are billed in the first pay application.

Benefits and Risks of Overbilling in Construction

Benefits: Improved Cash Flow and Working Capital

When a client accepts overbilled invoices, it provides a steady stream of working capital. Labor gets paid, materials get purchased, and subcontractors get funded — without the contractor drawing on credit lines or depleting reserves. The client, in effect, finances the job.

For contractors operating on thin margins, this is a meaningful advantage. CFMA reports that average net profit margins in construction typically range from 3% to 7%. With that little cushion, working capital management isn't optional — it's critical.

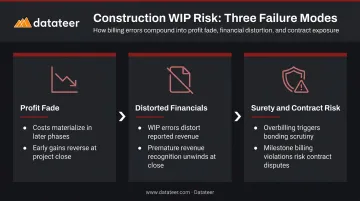

Risks: Profit Fade and Financial Misrepresentation

Overbilling that goes untracked masks missing costs. When those costs materialize in later project phases, the early reported gains reverse — a pattern called profit fade. A project that looked strong at 40% complete can finish at a loss, with little time to course-correct once late-stage costs start hitting.

Two additional failure modes compound the exposure:

- Distorted financials: WIP schedule input errors can distort reported revenue and gross margin across the portfolio

- Premature revenue recognition: Underestimating total costs under percentage-of-completion books revenue too early — an error that unwinds painfully at project close

Risks: Contractual Disputes and Surety Scrutiny

Many contracts tie billing to specific milestones or percentage-complete thresholds. Billing beyond those terms — even accidentally — can trigger disputes or claims of breach. On the bonding side, EisnerAmper confirms that overbilling and underbilling on WIP reports directly affect a construction firm's bonding capacity. Underwriters will want to see that overbilled amounts are held in cash on the balance sheet — not absorbed by unrelated job costs before the work is earned.

Best Practices for Managing Overbilling

Keep Cost Estimates Current

Update the estimated cost to complete on every open job at least monthly. This is non-negotiable. Outdated estimates corrupt the percentage-of-completion calculation and make overbilling invisible until it's too late.

Project managers and finance teams must work together here — PMs see field conditions that drive cost changes before those changes show up anywhere in accounting. A monthly sync between the field and the office isn't bureaucracy; it's the foundation of accurate WIP reporting.

Implement a Monthly WIP and Accrual Review

Review and adjust all accruals at month-end before billing is submitted. Subcontractor costs that haven't been invoiced yet need to be estimated and recorded. WIP schedules should be reconciled against actual job cost reports — not compiled by the accounting team alone and never touched by project management.

The review should happen at the PM and leadership level, with everyone looking at the same numbers.

Standardize Change Order Procedures

No billing should occur for work outside the approved contract scope until a signed change order exists in the system. No exceptions. This eliminates one of the most common and most preventable causes of overbilling discrepancies.

Track every pending change order — by age, dollar amount, and approval status. The longer an unapproved change order sits, the greater the risk that costs have been incurred without any authorization to bill.

Use Real-Time Financial Dashboards to Eliminate Reporting Lag

Manual WIP processes introduce a 10–20 day delay between when conditions change on the job and when finance teams can see the impact. By the time a spreadsheet-based WIP report is complete, the data is stale and overbilling issues may have compounded across multiple jobs.

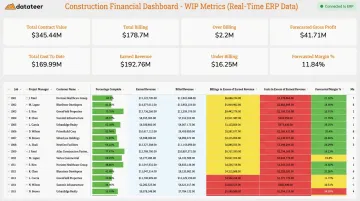

Datateer's construction financial dashboards connect directly to ERPs — including Sage, Viewpoint Vista, Acumatica, Foundation, and CMiC — refreshing WIP data overnight so CFOs and finance managers can see current overbilling positions across all jobs without waiting for month-end close. One client at Double L Management put it plainly: "that one click replaced two weeks' worth of prior work."

The platform automatically surfaces each job's key WIP metrics from source ERP data:

- Percentage complete

- Earned revenue vs. billed revenue

- Billings in excess of costs

- Costs in excess of billings

- Projected margin per job

That turns WIP monitoring from a forensic exercise into active financial management — with margin fade visible in time to act on it.

Frequently Asked Questions

What do 'costs in excess of billings' mean and how are they recorded?

Costs in excess of billings (underbilling) occur when a contractor has completed more work than they've invoiced for. The amount is recorded as a current asset on the balance sheet because the revenue is owed to the contractor and expected to be collected as billing catches up.

Is 'billings in excess of costs' a liability or an asset?

It's a current liability. Billings in excess of costs represents amounts invoiced that haven't been earned through completed work yet. Often labeled "deferred revenue," it must be earned off as project completion progresses. It is not recognized as income until the work is done.

How is billings in excess of costs calculated?

Divide costs incurred to date by total cost estimate to get percent complete. Multiply percent complete by the contract amount to get earned revenue. Subtract earned revenue from total billed — a positive result is billings in excess of costs; a negative result is costs in excess of billings.

What are the most common causes of overbilling in construction?

The top causes are: advance billing for mobilization before costs are incurred, billing at original estimate rates when actual costs come in lower, invoicing for unapproved change orders, and missing subcontractor cost accruals at month-end.

How does overbilling affect surety bond capacity?

Surety underwriters treat excessive overbillings as a potential sign of job borrowing or cash flow stress. They'll verify that overbilled amounts are backed by cash on the balance sheet, and consistently high overbillings relative to current liabilities will require explanation during the bonding process.

What is the difference between overbilling and fraud in construction?

Overbilling is a legitimate practice where invoices temporarily exceed earned revenue. It's disclosed on financial statements as a current liability. Fraud, by contrast, involves deliberately misrepresenting project progress, billing for work never performed, or charging above contractual rates without authorization — and that crosses into criminal territory.