Introduction

Cost to complete (CTC) is the estimated amount still needed to finish a project from a given point in time — covering all remaining labor, materials, subcontractor commitments, and overhead. It sits at the center of every WIP schedule and drives the financial picture construction teams produce each month.

Construction CFOs, finance managers, and project accountants rely on CTC to build WIP schedules, recognize revenue under percentage-of-completion accounting, and flag budget overruns before they compound. When CTC is off, the distortions reach lenders, bonding agents, and ownership — not just the finance team.

This guide explains what CTC means, how to calculate it step by step, which factors compromise its accuracy, and the mistakes that cause it to mislead rather than inform.

Key Takeaways

- CTC is the forward-looking estimate of all remaining costs to reach substantial completion

- Drives WIP reporting and percentage-of-completion revenue recognition under ASC 606

- The formula: CTC = Revised Estimated Cost at Completion (EAC) − Actual Costs Incurred to Date

- Main components: remaining labor, materials, subcontractors, equipment, and contingencies

- Accuracy depends on the quality and timeliness of cost data from the field reaching the accounting system

What Is Cost to Complete in Construction?

CTC represents the projected expenses a contractor still needs to incur to deliver the finished scope of work. It is calculated at a specific point in the project lifecycle and updated on a regular schedule — typically every monthly close cycle.

How CTC Differs from Related Terms

Two terms frequently get confused with CTC:

- Estimate at Completion (EAC) — the total projected project cost, meaning costs incurred to date plus CTC. EAC is the full picture; CTC is only the remaining piece.

- Original contract budget — a fixed baseline that does not change as conditions evolve. CTC and EAC must reflect current reality, not the original estimate.

That requirement to reflect current reality is what makes CTC more than an accounting line item — it's a project health indicator. When CTC rises unexpectedly mid-project, that movement signals scope creep, labor inefficiency, or material cost escalation. A CTC that isn't updated honestly when field conditions are deteriorating doesn't just mislead the team; it delays the response until the damage is done.

Why Cost to Complete Matters to Construction Finance Teams

WIP Reporting and Revenue Recognition

CTC is the single most critical variable in a WIP schedule. It determines percent complete, which drives how much revenue can be recognized in a given period under the percentage-of-completion method.

The cost-to-cost formula from Wegner CPAs makes this direct:

- Percent complete = Costs incurred to date ÷ Total estimated construction cost

- Revenue earned to date = Percent complete × Total contract price

An error in CTC flows immediately into both calculations.

Cash Flow and Profitability Distortions

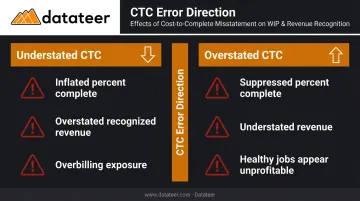

The direction of the error matters:

| CTC Error | Effect on Percent Complete | Effect on Financials |

|---|---|---|

| Understated CTC | Inflates percent complete | Overstates recognized revenue; creates overbilling exposure |

| Overstated CTC | Suppresses percent complete | Understates revenue; makes healthy jobs look unprofitable |

Both outcomes distort the financial statements reviewed by bonding agents, lenders, and ownership. NASBP identifies the WIP schedule as a core component of contractor financial packages covering revenues, billings, costs, gross profit, and over/underbillings — meaning CTC errors have direct consequences for bonding capacity.

Change Orders and IRS/GAAP Compliance

When an owner approves a scope change, the project accountant must update the revised EAC immediately. A change order that sits unrecorded in the WIP schedule produces inaccurate percent-complete figures for the entire reporting period. Dean Dorton notes that incorrectly reporting change orders can cause material swings and job-cost reporting errors.

Compliance amplifies the stakes further. IRC Section 460 generally requires the percentage-of-completion method for long-term contracts. GAAP under ASC 606 requires revenue to be recognized as performance obligations are satisfied — with cost-to-cost as a permitted input method, subject to adjustments for costs that do not depict performance. Under either framework, a stale or estimated CTC isn't just an internal problem; it's a reportable error.

How to Calculate Cost to Complete: Step by Step

The core formula:

CTC = Revised EAC − Actual Costs Incurred to Date

Once you have CTC, percent complete = Actual Costs ÷ Revised EAC, and revenue recognized = Percent Complete × Contract Price.

Worked Example

| Input | Value |

|---|---|

| Contract price | $1,000,000 |

| Revised EAC | $800,000 |

| Actual costs to date | $500,000 |

| CTC | $300,000 |

| Percent complete | 62.5% |

| Revenue recognized to date | $625,000 |

This is the standard cost-to-cost calculation consistent with ASC 606 input-method guidance and Treasury Regulation 1.460-4.

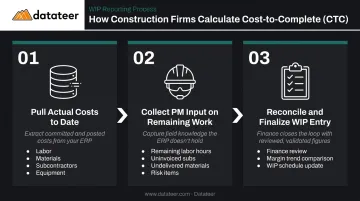

Step 1: Pull Actual Costs to Date

Extract committed and incurred cost data by job from the ERP or accounting system. That means:

- Posted labor charges

- Material invoices

- Subcontractor pay applications

- Equipment charges

Every cost must be coded to the correct cost code before the estimate is built. A single miscoded labor entry skews percent complete and can flip a healthy margin into a paper loss before the PM ever sees the WIP schedule.

Step 2: Collect Project Manager Input on Remaining Work

The PM must estimate the cost of all unfinished scope items:

- Remaining labor hours by trade

- Uninvoiced subcontractor work

- Unordered or undelivered materials

- Known risk items and potential scope additions

This estimate reflects field judgment, not a system calculation. Its accuracy rises or falls with how current and specific the PM's knowledge is at the time of input.

Step 3: Reconcile, Revise, and Finalize the WIP Entry

Finance compares the PM's CTC input against actual cost trends. Any job where the new CTC implies a margin significantly different from prior periods warrants scrutiny — it could indicate scope change, estimate error, or unreported cost events.

After adjustments are resolved, the finalized CTC enters the WIP schedule to compute percent complete and over/underbilling balances.

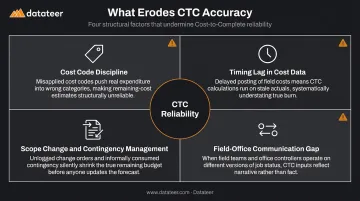

Key Factors That Affect CTC Accuracy

Cost Code Discipline

If field costs land on the wrong cost codes, finance cannot identify which work areas are over or under budget. A bottom-up CTC built from miscoded data is unreliable by definition. Standardized cost code mapping across all projects is a prerequisite for accurate CTC analysis — not a best practice, a requirement. Wiss Construction CPAs notes that accurate tracking at the cost-code level is essential to construction job costing. The consequences can be material: CBIZ uncovered $3 million in misclassified costs in a single construction client's WIP-related analysis.

Timing Lag in Cost Data

When actual costs take 10 to 20 days to flow from the field into the accounting system, the PM and finance team are building a CTC on incomplete information. This lag understates costs incurred while overstating apparent remaining budget — so by the time corrected figures arrive, the WIP report has already gone out the door with flawed numbers baked in.

Scope Change and Contingency Management

Unapproved or untracked change orders distort CTC because the revised EAC denominator has not been updated. Similarly, contingency drawdowns that go unrecorded create the illusion that a project is under budget when it is not. Left unresolved, either issue inflates reported margins on WIP schedules — a problem that surfaces at the worst possible time: during audit or lender review.

The Field-Office Communication Gap

CTC accuracy depends on two-way information flow:

- Finance needs current cost actuals from the field

- PMs need budget-to-actual data before they can make informed remaining-cost estimates

When these teams work from different data sources or different versions of the budget, the CTC reflects that disconnect directly.

Each of these four factors — coding discipline, data timing, scope control, and field-office alignment — erodes CTC reliability on its own. Together, they explain why so many project cost forecasts drift from reality long before the final billing.

Common CTC Mistakes and Best Practices

Mistake 1: Using the Original Budget as a Proxy for CTC

The most damaging misconception in construction finance is treating the original budget estimate as a stand-in for CTC instead of building a fresh forward-looking estimate from actual project conditions. This mistake is especially common mid-project and results in WIP reports that fail to capture margin fade until correction becomes expensive and unavoidable.

Mistake 2: Infrequent Updates

Some contractors update CTC only quarterly or at project milestones. A CTC more than 30 days old provides a false sense of financial control — costs and conditions change continuously. Industry best practice calls for updating CTC every monthly close cycle at a minimum, with mid-month revisions warranted when significant scope changes, change orders, or cost events occur. Surety and CPA sources consistently support this monthly cadence.

Mistake 3: Manual Spreadsheet-Based CTC Processes

The manual CTC refresh cycle typically follows the same painful sequence:

- Export cost data from the ERP manually

- Reformat and distribute Excel templates to PMs

- Wait days for input, then reconcile version conflicts

- Receive data that's already stale by the time it reaches review

Version control failures, broken formulas, and inconsistent cost code mapping compound the problem with every passing month.

Construction firms that connect their ERP directly to an automated reporting platform eliminate this lag. Datateer, for example, syncs with major construction ERPs — including Procore, Sage, Viewpoint Vista, Acumatica, and CMiC — replacing the manual month-end refresh with automated, continuously updated calculations at the job, phase, and cost-code level. Both PMs and finance teams access the same data simultaneously, which removes the information asymmetry that drives field-office conflicts.

Best Practice: Structured Cross-Functional Review

The most accurate CTC processes involve a monthly review where finance presents cost-to-date actuals and PMs provide remaining cost estimates in the same session, using the same live data. This collaborative cadence catches discrepancies before they compound into material misstatements on the WIP schedule. When both teams are looking at the same numbers, disagreements surface as conversations rather than corrections.

Frequently Asked Questions

What does "cost to complete" mean in construction?

CTC is the estimated cost of all remaining work needed to finish a construction project, calculated at a specific point in time. It covers remaining labor, materials, subcontractor commitments, equipment, and overhead, and is updated regularly throughout the project lifecycle.

How do you calculate cost to complete in construction?

CTC equals the Revised Estimated Cost at Completion (EAC) minus Actual Costs Incurred to Date. Percent complete is then calculated as actual costs divided by EAC, which determines how much revenue can be recognized in a given period under the percentage-of-completion method.

What are the 4 types of costs in construction?

The four main cost categories are: direct costs (labor, materials, equipment), subcontractor costs, indirect and overhead costs allocable to the contract, and contingency or allowance costs. Contingency costs are the category most frequently underestimated during mid-project CTC updates.

What is the difference between cost to complete and estimate at completion?

CTC is the remaining cost to finish the project. Estimate at Completion (EAC) is the total projected project cost — actual costs incurred to date plus CTC. EAC tells you where the project lands financially; CTC tells you what it will cost to get there.

How often should cost to complete be updated on a construction project?

Industry best practice calls for updating CTC every monthly close cycle at a minimum. Mid-month revisions are appropriate when significant scope changes, approved change orders, or unexpected cost events occur between scheduled close dates.

What happens if cost to complete is underestimated?

An understated CTC inflates the percent complete figure, which overstates recognized revenue and creates an overbilling position on the WIP schedule. Project margins appear healthier than they are until a correction in a later period compresses recognized revenue — sometimes wiping out an entire quarter's reported profit in a single close cycle.