The core formula is simple division. Most errors come from using the wrong method, carrying stale cost estimates, or missing inputs like unapproved change orders and stored materials. This guide walks through the exact steps, the three calculation methods, the variables that break accuracy, and how % complete flows into your WIP schedule.

Key Takeaways

- % Complete = Costs Incurred to Date ÷ Total Estimated Project Costs — the cost-to-cost method required under GAAP and IRC Sec. 460

- Three methods apply (cost-to-cost, efforts-expended, units-of-delivery) — whichever you choose must stay consistent throughout the project

- Multiply % complete by the contract price to calculate revenue earned in the current period

- Stored materials, unapproved change orders, and stale cost estimates are the top sources of inaccurate % complete figures

- The % complete figure flows directly into your WIP schedule, where it reveals overbilling or underbilling on every active job

How to Calculate Percentage of Work Completed in Construction

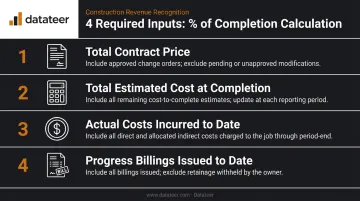

Step 1: Gather Your Four Key Inputs

Before any calculation, confirm these four figures — and make sure every one reflects current data:

- Total contract price — including all approved change orders

- Total estimated cost at completion — your most current forecast, not the original bid

- Actual costs incurred to date — direct and indirect costs only; exclude committed costs, open purchase orders, and stored materials not yet incorporated into the work

- Progress billings issued to date — the cumulative amount invoiced to the owner

Stale inputs produce unreliable outputs. If your total estimated cost hasn't been revised since project kickoff and material prices have moved, your % complete figure is already wrong before you run the formula.

On costs incurred: only count costs for work actually performed. Committed costs, open POs, and stored materials sitting in a staging yard don't qualify — the cost enters the calculation when the work gets done.

Step 2: Apply the Percentage Complete Formula

$$\text{% Complete} = \frac{\text{Costs Incurred to Date}}{\text{Total Estimated Cost at Completion}}$$

Example: A project has $1,000,000 in total estimated costs. You've incurred $600,000 to date.

$$\frac{$600,000}{$1,000,000} = 60% \text{ complete}$$

This percentage feeds directly into your revenue recognition calculation in Step 3.

Step 3: Calculate Revenue Earned to Date

Apply % complete to the contract price:

$$\text{Revenue Earned to Date} = \text{% Complete} \times \text{Contract Price}$$

Using the same example, with a $1,250,000 contract:

$$60% \times $1,250,000 = $750,000 \text{ revenue earned to date}$$

This is the revenue you can recognize in the current reporting period — not what you've billed, not what you've collected.

Step 4: Determine Overbilling or Underbilling

$$\text{Overbilling / Underbilling} = \text{Revenue Earned to Date} - \text{Progress Billings to Date}$$

Continuing the example — if you've billed $800,000 against $750,000 earned:

$$$750,000 - $800,000 = -$50,000 \text{ (overbilling)}$$

- Underbilling (positive result) — Current asset on the balance sheet; you've earned work you haven't yet invoiced.

- Overbilling (negative result) — Current liability; you've invoiced ahead of work performed.

Lenders and sureties look at these balances closely. Large or persistent overbillings can signal cash flow risk; growing underbillings may indicate billing backlogs that will pressure liquidity in future periods.

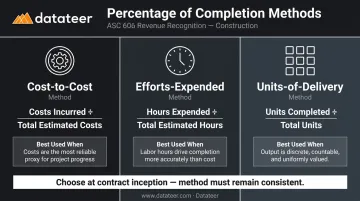

The Three Methods for Calculating Percentage of Completion

The cost-to-cost method is the default under both GAAP (ASC 606) and IRC Sec. 460 for non-exempt long-term contracts. Under ASC 606, progress measures fall into two categories: input methods and output methods. Cost-to-cost and efforts-expended are input methods; units-of-delivery is an output method. The selected method must faithfully depict transfer of control to the customer.

| Method | Formula | Best Used When |

|---|---|---|

| Cost-to-Cost | Costs incurred ÷ Total estimated costs | Most commercial, industrial, and civil contracts; required for tax PCM under Reg. 1.460-4 |

| Efforts-Expended | Hours expended ÷ Total estimated hours | Labor- or machine-intensive specialty work where material costs are minimal or front-loaded |

| Units-of-Delivery | Units completed ÷ Total contracted units | Projects with discrete, countable deliverables of roughly equivalent cost and effort |

Cost-to-Cost Method

Costs incurred divided by total estimated project costs. Most engineering and construction firms use cost-to-cost because project costs are the primary driver of progress on most contracts — and they produce a reliable, auditable proxy. It's also the method IRC Sec. 460 and Reg. 1.460-4 mandate for non-exempt long-term construction contracts, so there's no practical alternative for tax reporting on most commercial work.

Efforts-Expended Method

Labor hours (or machine hours) expended to date divided by total estimated hours. Use this when cost-to-cost would be distorted — for example, a specialty welding or mechanical contract where front-loaded material procurement would inflate early % complete figures if costs were the measure.

Units-of-Delivery Method

Units completed divided by total contracted units. Works for projects with clearly defined, equivalent deliverables — a set number of bridge spans or housing units with consistent scope. It breaks down quickly when unit costs, complexity, or duration vary from one deliverable to the next.

Choose your method at contract inception and hold it. Switching mid-contract distorts % complete and revenue recognition across reporting periods — auditors and your CPA will flag it as a revenue recognition error.

Key Variables That Affect Percentage Calculation Accuracy

The formula is straightforward. The data feeding it often isn't. Four variables cause most of the accuracy problems on live projects.

Accuracy of Total Estimated Costs

The denominator in cost-to-cost is total estimated cost at completion. If that number is understated — or hasn't been revised since the original bid — % complete will be artificially inflated, pulling revenue forward. Firms should reassess total estimated costs at every reporting period and document any revisions, particularly on projects with volatile material prices or scope changes.

Change Orders

Every approved change order affects both the contract price (revenue) and potentially total estimated costs (denominator). Under ASC 606, unapproved change orders where scope is accepted but price isn't are evaluated as variable consideration — include them only to the extent a significant revenue reversal is not probable. Accounting teams often don't find out about approved changes until weeks after the fact. Finance needs a direct, timely communication channel with project managers.

Stored Materials

Materials purchased and on-site but not yet incorporated into the work should not be counted as "costs incurred" for % complete purposes. ASC 606-10-55-21 requires adjustment when costs incurred don't proportionately depict performance, and uninstalled materials are a classic example. Including them inflates % complete and pulls revenue recognition forward.

The fix: segregate stored material costs in the job cost ledger with a distinct cost code, keeping them out of the "incurred" bucket until installation.

Subcontractor and Retention Costs

Sub invoices often lag field progress by weeks. If a subcontractor completed work in March but didn't invoice until April, your March % complete is understated. The further behind sub billing falls, the more distorted your WIP schedule becomes.

Retention withheld from subs also needs consistent treatment. Decide upfront whether retention is included in or excluded from costs incurred, then apply that treatment uniformly across all jobs. Inconsistent treatment makes WIP analysis across the portfolio unreliable.

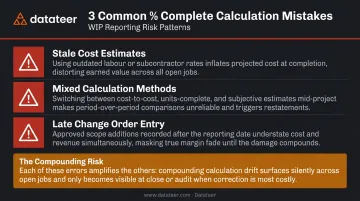

Common Mistakes When Calculating Percentage of Work Completed

Three errors account for most of the % complete problems that surface at project close or audit time:

- Stale cost estimates — Carrying the original project estimate forward without updating for known overruns, price changes, or added scope distorts % complete from the start. The error compounds quietly until a revenue shortfall appears at close that nobody can explain.

- Mixed calculation methods — Applying cost-to-cost on one project and labor hours on another without documentation creates inconsistent WIP analysis. The requirement isn't just to pick a method; it's to document why that method faithfully depicts performance for each contract.

- Late change order entry — A project manager approves a scope addition on March 28. Accounting processes it April 10. The March close shows % complete and revenue both misstated, triggering a correction to management, lenders, or auditors.

That last one isn't a one-off mistake — it's a recurring process gap that continues until the field-to-finance workflow is fixed. Datateer's Change Order Impact & Aging module tracks pending, approved, and stalled change orders with aging by days since submission, giving finance teams visibility into what's outstanding before the close.

Using Percentage Complete to Build Your WIP Schedule

The % complete figure doesn't stand alone. It flows directly into the WIP (Work-in-Progress) schedule — the central financial document for tracking all active jobs. Every set of inputs and outputs (% complete, revenue earned, and overbilling/underbilling) comes together here, and the WIP schedule is what lenders, bonding agents, and auditors actually review.

What the WIP Schedule Reveals

A standard WIP schedule shows, per job:

- Contract value (including approved change orders)

- Total estimated costs at completion

- Costs incurred to date

- % complete

- Revenue earned to date

- Progress billings to date

- Overbilling or underbilling position

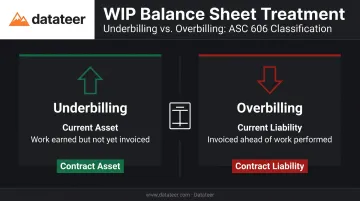

The balance sheet implications matter. Under both legacy construction accounting terminology and ASC 606:

- Underbillings = current asset (costs and estimated earnings in excess of billings / contract asset)

- Overbillings = current liability (billings in excess of costs and estimated earnings / contract liability)

A WIP schedule heavy with underbillings can signal cash flow risk — you've done the work but haven't collected. Significant overbillings can signal front-loading, where a contractor is drawing cash against future work. Sureties and lenders read both patterns carefully.

The Problem With Manual WIP Builds

Most construction firms still build WIP schedules manually in Excel, pulling exports from their ERP at month-end. That process creates a reporting lag that commonly stretches two weeks by the time data is exported and reconciled — time during which decisions get made on numbers that are already outdated.

Double L Management described the shift after implementing Datateer: "That one click replaced two weeks worth of prior work."

Datateer integrates directly with 12+ construction ERPs — including Procore, Sage 100/300/Intacct, Viewpoint Vista, Viewpoint Spectrum, Acumatica Construction, Foundation Software, CMiC, and Jonas — to produce automated WIP reports pulled directly from the source. Finance teams and project managers access the same data simultaneously, cutting the back-and-forth reconciliation cycle and the version-control problems that come with emailing Excel files.

WIP reporting is included in the base subscription at flat annual pricing starting at $10,000/year per data source, with unlimited users.

Frequently Asked Questions

What is the percentage of completion method in construction accounting?

It's the method of recognizing revenue and expenses on long-term contracts in proportion to the work completed each period, rather than waiting until the project is finished. It's required under GAAP (ASC 606, for contracts recognized over time) and under IRC Sec. 460 for most commercial contractors with non-exempt long-term construction contracts.

What is the difference between the cost-to-cost method and the units-of-delivery method?

Cost-to-cost measures progress using actual costs incurred versus total estimated costs and is the default for most contracts and the method required under IRC Sec. 460. Units-of-delivery measures progress using discrete countable outputs (floors, spans, units), and works only when each unit is roughly equivalent in cost and effort.

How does percentage of work completed affect a WIP report?

% complete determines revenue earned to date, which is then compared to progress billings to identify overbilling or underbilling per job. The WIP schedule aggregates this across all active projects, giving CFOs, lenders, and sureties a company-wide view of financial performance and billing position.

What happens if I miscalculate the percentage of completion?

Overstating % complete pulls revenue forward : costs continue but recognized revenue slows, creating a shortfall at project close. Understating it defers revenue and understates profitability. Both distort what you report to lenders, bonding agents, and management and can create material misstatements.

Are contractors required to use the percentage of completion method for taxes?

Under IRC Sec. 460, most contractors with long-term construction contracts must use PCM for federal taxes. Exemptions cover home construction contracts and small contractors: for 2026, the gross receipts threshold under Sec. 448(c) is $32 million (per IRS Rev. Proc. 2025-32), provided the contract is expected to complete within two years.

How often should contractors update their percentage of completion?

At minimum, recalculate % complete at every monthly close and review and revise total estimated costs at the same frequency. More frequent updates reduce the risk of cumulative errors surfacing only at year-end or during an audit.