Retainage is one of the few industries practices where doing your job correctly doesn't guarantee getting paid in full. For firms running on tight margins, that gap between work performed and cash received isn't a minor inconvenience. It's a structural funding problem that compounds across every billing cycle and every project in your portfolio.

This article is written for construction CFOs, finance managers, and CPAs advising contractors. We'll cover how retainage creates cash flow strain, how it appears on your financial statements, the most common mistakes that worsen the problem, and practical strategies to manage it — including what real-time retainage visibility actually looks like in practice.

Key Takeaways

- Retainage typically withholds 5–10% of each progress payment, creating a widening gap between earned revenue and collected cash

- CFMA's 2025 benchmarks show 6.7% net income before taxes for average contractors, so a 10% retainage clause can exceed a firm's entire expected profit

- Retainage receivable is a Contract Asset under ASC 606; misclassifying it as a standard receivable distorts working capital analysis

- Subcontractors often face retainage of 10–15% and may wait 12–18 months for release after completing their scope

- Negotiation, milestone-based release triggers, and real-time tracking are the three most effective tools for managing retainage exposure

What Is Retainage in Construction?

Retainage (also called retention) is the contractually specified percentage withheld from each progress payment until a project reaches substantial or final completion. The withheld amount protects the project owner against incomplete work, defects, or contractor default.

On a $100,000 invoice at 10% retainage, only $90,000 is paid. On a $5 million project, that's $500,000 locked up for the duration of the build — earning nothing for the contractor while their costs run at full pace.

Standard Rates and Who Sets Them

According to CFMA, retainage typically sits at 5% or 10%, with 10% historically the standard on most commercial and public projects. That's still common, though 5% is increasingly common on larger commercial work.

The applicable rate depends on:

- Negotiated contract terms between the owner and contractor

- State statute — California, Florida, Virginia, New York, and Washington cap public project retainage at 5%; Texas caps it at 10%

- Federal rules under FAR 52.232-5, which permits up to 10% retention on fixed-price contracts when satisfactory progress isn't being made

State Prompt Payment Acts also set deadlines for retainage release and specify interest penalties for owners who miss them. California imposes a 2% per month penalty on wrongfully withheld retention. New York requires release within 30 days of substantial completion. Knowing these statutes — and invoking them — is the difference between collecting on time and waiting months.

How Retainage Directly Impacts Cash Flow

The core problem is asymmetry. Your costs — labor, materials, subcontractor payments, equipment — are 100% immediate. Your revenue is only 90–95% immediate. That gap grows with every billing cycle.

The Margin Squeeze

Here's where retainage gets dangerous for most firms. CFMA's 2025 Financial Benchmarker reports 6.7% net income before taxes for average contractors. A 10% retainage clause means the owner is withholding more than the contractor's entire expected profit margin on the job.

In practical terms: the contractor is financing the owner's project risk with their own capital, interest-free, for the full duration of the build. If the project runs over schedule or disputes emerge at closeout, that financing period extends indefinitely.

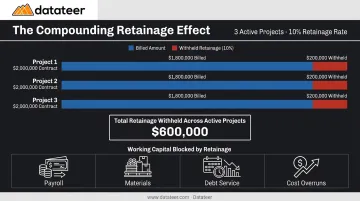

The Multi-Project Compounding Effect

Running three concurrent projects each with 10% retainage doesn't just double or triple the problem — it changes the nature of the problem. A firm with three $2M projects in progress simultaneously has up to $600,000 in withheld funds across its portfolio at any given time. That's working capital that can't be used to:

- Fund payroll during slow billing periods

- Cover material purchases on new project starts

- Service debt or maintain credit line headroom

- Respond to unexpected cost overruns on any one job

The longer the project timelines, the more acute this becomes. On a 24-month project, a contractor is effectively making an interest-free loan to the owner for two years. Full repayment depends on punch-list completion and owner sign-off — neither of which the contractor fully controls.

The Downstream Impact on Subcontractors

The cash strain doesn't stop at the GC level. GCs typically mirror the owner's retainage clause when writing subcontracts, meaning a sub who completes their scope in month 3 of an 18-month project may wait until month 18 or later to collect withheld funds — even though their work was finished and accepted long ago.

The American Subcontractors Association notes that retainage on subcontracts is often 10–15%, sometimes higher than what the GC faces. This cascading withholding across the payment chain creates real operational problems:

- Subs operating on thin margins can't take on new bids while capital is tied up

- GC-sub relationships strain when payment timelines feel arbitrary

- Supply chain stability suffers when key trade contractors hit cash limits

How Retainage Appears in Your Financial Statements

Retainage creates a specific accounting problem: your financial statements can show a healthy business while your cash position tells a very different story. Knowing where retainage lives on each report — and what it actually signals — is how finance teams avoid that trap.

Balance Sheet Classification Under ASC 606

Under FASB ASC 606, a contract asset is a conditional right to consideration — meaning payment is still contingent on something other than the passage of time. A receivable is an unconditional right.

For retainage, CICPAC guidance is clear:

- Active-job retainage → Contract Asset (payment is conditional on project completion or owner approval)

- Completed-job retainage → Contract Receivable (work is done, payment is now an unconditional obligation)

Many firms lump both together or misclassify active retainage as a standard receivable. That overstates liquid working capital and can mislead lenders, bonding companies, and leadership alike.

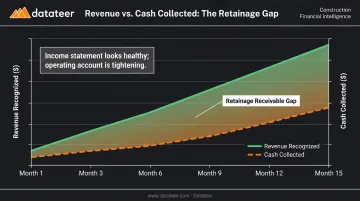

The Revenue vs. Cash Gap

Under percentage-of-completion accounting, revenue is recognized as work is performed — retainage doesn't reduce reported revenue. But it absolutely reduces cash from operations.

A firm can report strong profitability while simultaneously running low on cash, because retainage receivables are growing faster than collections. The income statement looks healthy. Meanwhile, the operating account is tightening — and the gap only widens as more projects go active.

WIP Schedule Implications

That cash gap shows up directly in your WIP schedule. Retainage receivables are a key component of an accurate WIP report, and firms that don't segregate them from regular receivables risk two compounding problems:

- Overstated working capital — the balance sheet looks more liquid than it is

- Flawed project forecasts — cash availability projections built on numbers that won't collect for months

Common Retainage Mistakes That Worsen Cash Flow

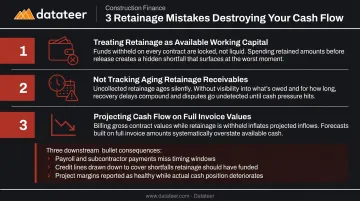

Three mistakes account for the majority of retainage-related cash flow problems:

1. Treating retainage as available working capital. Spending against withheld funds before they're released sets up a liquidity crisis at closeout — the point when expenses have been incurred but the final payment hasn't arrived. This is one of the most common reasons profitable projects produce cash shortfalls.

2. Not tracking aging retainage receivables. Without a systematic process for monitoring which retainage balances are overdue, who needs follow-up, and what the release trigger status is, funds simply sit uncollected. Owners rarely volunteer payment — and when contractors don't follow up promptly, lien rights expire and collection windows close.

3. Projecting cash flow on full invoice values. Firms that forecast based on gross billings — without adjusting downward for withheld retainage — routinely underestimate their funding gaps. The downstream effects compound quickly:

- Overbidding on new work the firm can't actually finance

- Drawing down credit lines that could be preserved for real emergencies

- Getting caught off guard when a major retainage release is delayed

Strategies to Mitigate Retainage's Cash Flow Impact

The best time to manage retainage is before you sign the contract. After that, disciplined collection processes and real-time tracking carry the work.

Negotiate the Rate and Structure Upfront

- Push for 5% instead of 10% — many owners will accept this on projects where the contractor has a track record

- Request a step-down provision: retainage reduces from 10% to 5% after 50% project completion

- For GCs, negotiate line-item release for early-completing trades (sitework, concrete, MEP rough-in) so subs aren't waiting until project closeout for funds they've long since earned

Define the Release Trigger Precisely

Vague language like "owner's satisfaction" or "final completion" gives owners unlimited flexibility to delay. Push for substantial completion as the release trigger and ensure the contract defines it with measurable criteria — not subjective judgment calls.

Build a Retainage Reserve Fund

Set aside a defined percentage of revenue from each project specifically to cover the retainage gap. Most firms target 3–5% of project revenue as a reserve baseline. This reduces dependence on credit lines during collection lag and keeps payroll and material costs funded without borrowing.

Consider Retention Bonds

Contractors with strong financials can offer a surety-backed retention bond in lieu of cash withholding. The owner receives equivalent security; the contractor receives full payment on each invoice. Washington State's RCW 60.30.020 requires owners to accept a retainage bond in lieu of cash withholding for qualifying contractors. Other states have similar provisions.

Build a Proactive Collection Process

Treat retainage receivables like any other aged A/R:

- Set calendar reminders ahead of each project's anticipated release date

- Confirm owner satisfaction proactively before the contractual deadline

- Send formal demand letters when statutory deadlines under the applicable Prompt Payment Act are missed — interest penalties and attorney fees may be recoverable

Tracking Retainage in Real Time: From Spreadsheets to Dashboards

Most construction firms manage retainage through spreadsheets or disconnected ERP exports. Compiling a complete picture takes days or weeks, which means finance leaders are perpetually working with stale data. By the time an overdue retainage balance shows up on a report, it may already be 60–90 days past the release date.

What Real-Time Retainage Tracking Looks Like

A functional retainage dashboard doesn't just show total balances. It surfaces:

- Retainage receivable broken down by project and owner

- Overdue balances with aging visibility

- Release-trigger status for each project

- A/P retainage owed to subcontractors alongside A/R retainage owed to the firm

- Integration with 13-week cash flow forecasting so retainage release timing feeds directly into liquidity projections

That last point matters most. Without that connection to cash flow forecasting, retainage balances are passive data — visible but not actionable. Feed release timing into a live forecast and finance teams can anticipate liquidity gaps weeks before they arrive, not after the fact.

How Datateer Handles This

Datateer's Construction Retainage Tracking & Schedule Analytics module connects directly to 12+ construction ERPs: Procore, Sage (100/300/Intacct), Viewpoint Vista, Viewpoint Spectrum, Acumatica Construction, Foundation Software, CMiC, Jonas Construction, QuickBooks, and NetSuite. It delivers both A/R and A/P retainage visibility in a single dashboard, included in the base flat annual subscription (starting at $10,000/year per data source, unlimited users) with no separate add-on fee.

The retainage dashboard integrates with WIP reporting, over/under-billings, and the 13-week cash flow forecast within the same platform. CFOs and controllers can see retainage exposure alongside billings positions and liquidity projections without toggling between disconnected reports. Implementation takes 2–4 weeks from ERP connection to live dashboards.

For firms that want to assess their current retainage visibility before committing to a platform, Datateer offers a free 15-Minute Workflow Audit — no slides, no sales pitch, just a review of your current process and a look at how automated retainage tracking would work with your specific ERP data.

Frequently Asked Questions

How does retainage affect cash flow?

Retainage withholds 5–10% of each progress payment until project completion, creating a gap between work performed and cash received. This gap accumulates across billing cycles and ties up significant working capital — especially on long-duration or multi-project portfolios where retainage balances can reach hundreds of thousands of dollars simultaneously.

What is the point of retainage in construction?

Retainage gives project owners financial leverage to ensure contractors complete all work to specification and address punch-list items before final payment. It acts as a performance incentive and a reserve against contractor default or defective work — though the practice is widely criticized for burdening contractors and subcontractors who have already delivered quality work.

What is a typical retainage percentage in construction?

5% and 10% are the most common rates. 10% was historically the standard, but 5% is increasingly common on larger commercial projects. Several states cap retainage by statute — California, Florida, Virginia, and New York cap public project retainage at 5%, while Texas caps it at 10% under the Property Code.

How long can retainage be held in construction?

Retainage is typically held until substantial or final completion, but release timelines vary by contract and jurisdiction. Many states have Prompt Payment Acts requiring release within a defined period after substantial completion — for example, New York mandates release within 30 days, with interest penalties for owners who miss that deadline.

Can retainage be negotiated?

Yes — and the contract signing table is the right place to push. Contractors can request a lower percentage, a step-down clause, milestone-based release, or a retention bond in place of cash withholding. Owners typically have more flexibility on structure than on rate, making step-down provisions and line-item releases easier wins than a flat rate cut.

How should retainage be recorded in financial statements?

Retainage receivable on active jobs is recorded as a Contract Asset under ASC 606 (conditional right to payment); once a job reaches completion, it moves to Contract Receivables (unconditional right). Retainage doesn't reduce reported revenue but does reduce operating cash flow — which is why firms relying solely on the income statement can miss significant liquidity gaps hiding in their retainage balances.